The U.S. Dollar Index (DXY) has rebounded over the last month following its worst first half since its inception in 1973. Progress on trade negotiations, a patient higher-for-longer Federal Reserve (Fed), better-than-expected economic data (up until last Friday’s employment report), and rotational pressure back into U.S. equities have been key catalysts behind the recovery. Technically, oversold conditions, contrarian levels of bearish sentiment and positioning, and major uptrend support for the DXY have also been supportive of the greenback.

Of course, with currencies, it’s all relative to the other side of the pair. For the DXY, that means what happens in the Eurozone can significantly influence the trajectory of the dollar, as the euro holds the largest weight (58%) in the basket of currencies against which the dollar is compared. A quick review of European economic conditions and monetary policy reveals a weaker growth profile and a relatively more dovish central bank.

While the European Central Bank (ECB) pushed the pause button during its monetary policy meeting last month, policymakers have cut their target rate from 4% to 2% over the last year, including four 0.25% cuts in 2025, while another 0.25% reduction is expected by December. This compares to the Fed’s current upper-bound target rate of 4.5%, with zero rate cuts so far this year and maybe two or three 0.25% cuts by year-end. ECB President Christine Lagarde has also continued to stress that risks to Eurozone economic growth remain “tilted to the downside.” This is a much different tone than Fed Chair Jerome Powell’s comments last week, stating, “Despite elevated uncertainty, the economy is in a solid position.”

The dismal U.S. payrolls print last Friday and an open seat to fill outgoing Fed Governor Adriana Kugler’s seat, after she resigned last week, will likely introduce a more dovish tone from the Fed; however, we don’t expect a material deviation away from the market’s expectation of rate cuts starting again in September.

Zooming out to a longer-term perspective reveals a dollar holding above a secular uptrend that began back in 2008. The current 12% decline from the January high is also commensurate with other drawdowns since the dollar broke out above the 2009–2010 highs. Speculator short positioning among institutional/hedge fund investors has also reached contrarian levels that overlapped with previous inflection points. The next big test for the greenback will be holding above the 50-day moving average (dma) near 98.25 and recapturing the lower end of its prior range at 100.75.

The Dollar Finds Support Off a Secular Uptrend

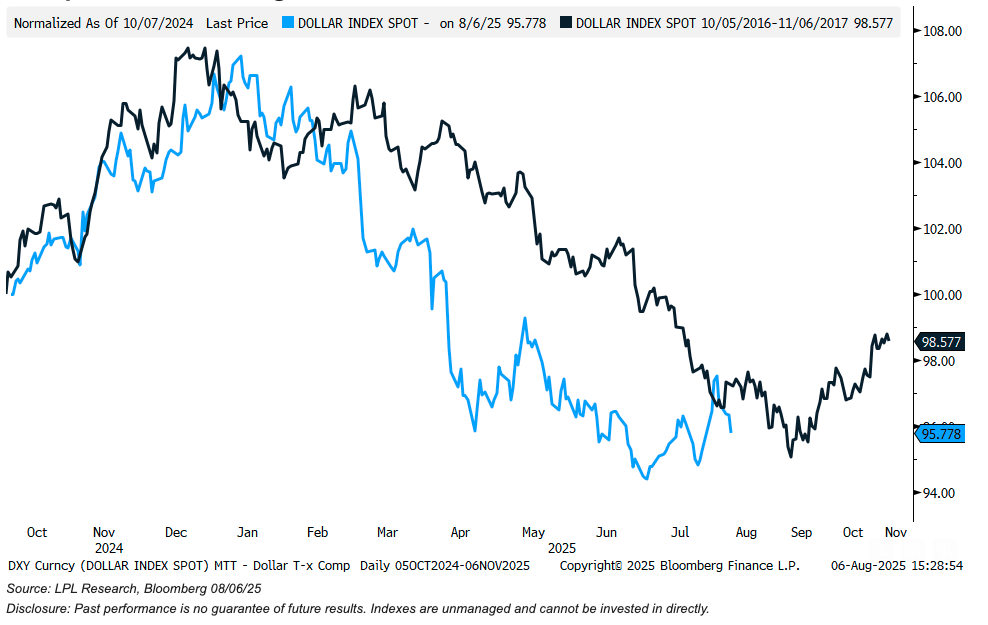

While “this time is different” seems like an appropriate disclaimer when comparing President Trump’s first term to his second term, price action in the dollar has been relatively consistent across both periods. Following President Trump’s November 2015 election victory, the dollar surged around 8% before peaking in January. From that peak, the dollar suffered a sizable 12% drawdown before bottoming in September. Fast forward to Election Day in 2024 and Trump 2.0, the dollar staged a comparable rally into January before peaking ahead of the current 12% drawdown into July. Of course, context is key, and we acknowledge the 2016 macro backdrop was much different than today; however, we remain receptive to the adage that history may not repeat, but it often rhymes.

Trump 1.0 vs. 2.0 Analog

Summary

The dollar is trading near an inflection point. At a minimum, the recent relief rally could have more room to run despite potential headwinds from the Fed shifting to a more dovish tone. On a relative basis, the U.S. economy is holding up well and should avoid a recession, with less downside risk than Europe. Furthermore, American exceptionalism has arguably been revived in the wake of U.S. technology stock leadership since the April lows. Further outperformance in this space could continue to attract foreign investors back to the U.S., boosting dollar demand and potentially counterbalancing the negative impact of reduced global trade.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities. Investors may be well served by bracing for occasional bouts of volatility given how much optimism is currently reflected in stock prices. LPL Research advises against increasing portfolio risk beyond benchmark targets currently and continues to monitor tariff negotiations, economic data, earnings, the bond market, and various technical indicators to identify a potentially more attractive entry point to add equities on weakness. The Committee’s regional preferences across the U.S, developed international, and emerging markets (EM) are aligned with benchmarks. The Committee still favors growth over value, large caps over small caps, and the communication services and financials sectors.

Within fixed income, the STAAC holds a neutral weight in core bonds, with a slight preference for mortgage-backed securities (MBS) over investment-grade corporates. The Committee believes the risk-reward for core bond sectors (U.S. Treasury, agency MBS, investment-grade corporates) is more attractive than plus sectors. The Committee does not believe adding duration (interest rate sensitivity) at current levels is attractive and remains neutral relative to benchmarks. The Committee would get more interested in adding long-term bonds if the U.S. 10-Year Treasury yield got closer to 5%.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by LPL Financial