The Federal Reserve (Fed) delivered a highly anticipated 0.25% interest rate cut during its September 16-17 Federal Open Market Committee (FOMC) meeting. Fed Chair Powell said the move should be viewed as a “risk-management cut” in response to signs of a weakening labor market. Powell attributed most of the slowdown in payroll growth to lower immigration and lower labor force participation, but further added, “Labor demand has softened, and the recent pace of job creation appears to be running below the ‘breakeven’ rate needed to hold the unemployment rate constant.” Policymakers also penciled in two additional 0.25% interest rate reductions for 2025, and an additional 0.25% cut by year-end 2026. Within the Fed’s Summary of Economic Projections (SEP), forecasts for real gross domestic product (GDP) growth were revised higher for 2025 and 2026, while the unemployment rate was forecasted 0.1% lower for both 2025 and 2026. Inflation forecasts for 2026 rose to 2.6% from 2.4%. While newly appointed Fed Governor Steven Miran was the only dissent at the meeting (who voted for a 0.50% cut), there was little unanimity on the dot plot for future cuts. Even Chair Powell mentioned during his press conference that “if you ask any of the forecasters whether they have great confidence in their forecast right now. I think they'll honestly say, no.”

While the FOMC meeting delivered a little bit of everything for both hawks and doves last week, it also delivered on what the market wanted to hear — the rate-cutting campaign is back in gear. Stocks have responded with a series of record highs. With this major risk-clearing event in the rearview mirror, investors are now asking what happens next. The Fed has a challenging job ahead, balancing near-term risks to inflation and downside risks to the labor market, leaving “no risk-free path” with future monetary policy decisions.

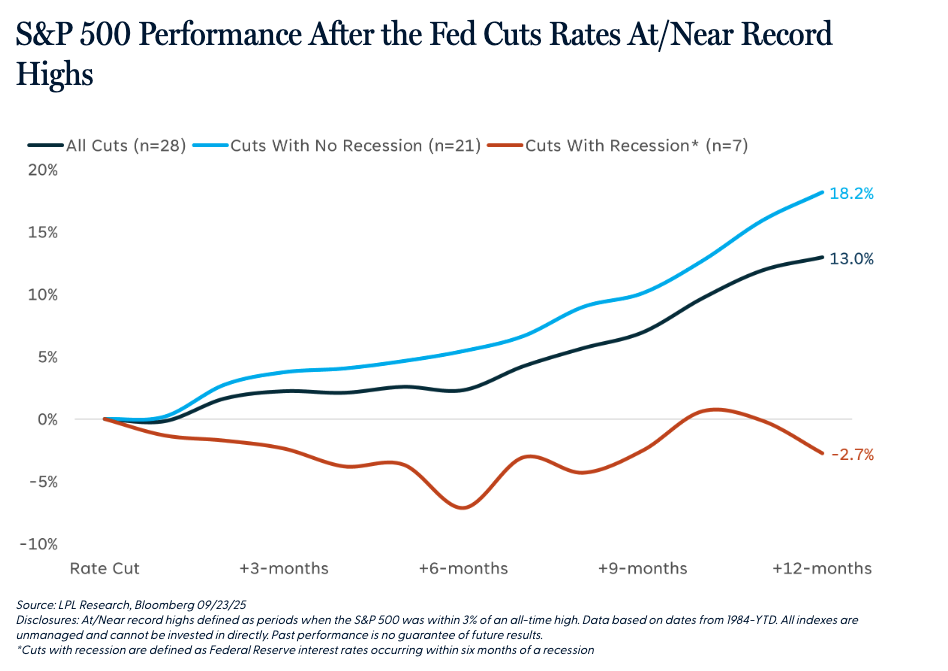

For stocks, history suggests that the path ahead is likely higher, based on previous instances when the Fed cut rates when stocks were trading near or at record highs, although past performance is no guarantee of future results. Since 1984, the Fed has cut rates 28 different times when the S&P 500 was within 3% of an all-time high. After the cut, the broader market traded higher by an average of 13.0% 12 months later, with 93% of periods producing positive returns. When there was no recession near or during the rate cut (we filtered for cuts occurring at least six months prior to a recession), the average 12-month return for the S&P 500 increased to 18%, with 21 out of 21 periods producing positive results. When a recession overlapped near or during a rate cut, the market posted an average loss of 2.7% in the 12 months after the Fed reduced rates, with only 25% of periods generating a gain.

Factoring in Labor Market Conditions

Absent a recession, the history lesson from comparable rate cuts to the current market environment leans bullish. However, it’s important to consider the underlying conditions that prompted the Fed to ease policy last week. Economic growth has moderated, and the labor market is showing signs of fatigue. As highlighted in LPL Research’s latest Weekly Market Commentary (“No Risk-Free Path”), the Bureau of Labor Statistics revised job growth downward by 818,000 for the 12 months ending March 2024 — roughly 68,000 fewer jobs per month than previously reported. This followed a weak August Employment Report, which showed three-month average payroll gains of just 29,000 and included the first negative monthly print in over four years (June was revised to -13,000).

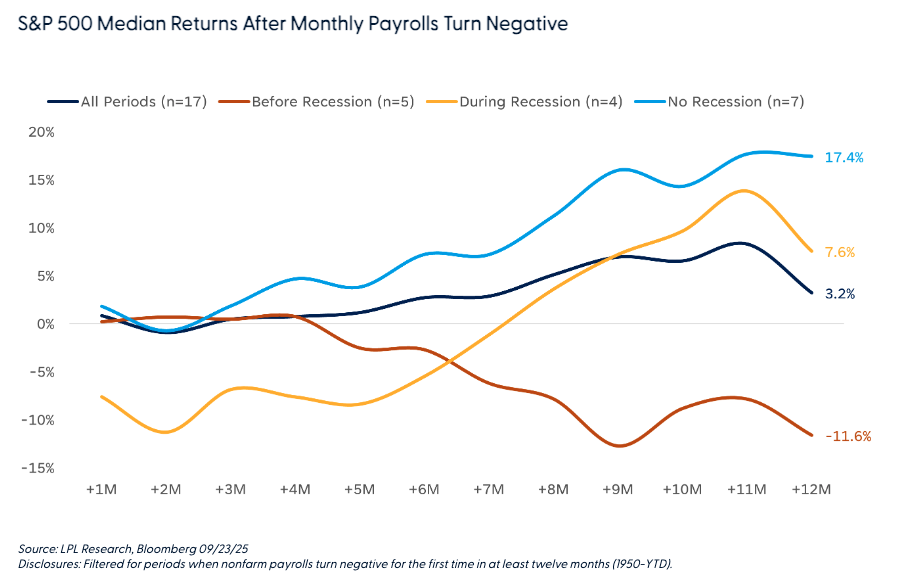

The end of consecutive positive monthly payrolls serves as another important history lesson for markets, as negative payrolls prints have often overlapped with recessions and/or subpar equity market performance. Since 1950, when nonfarm payrolls turn negative for the first time in at least a year, the S&P 500 has delivered a median 12-month return of just 3.2%, with positive outcomes in about 65% of cases. However, the path forward diverges sharply depending on whether a recession follows. In the five instances that preceded a recession, the median return was -11.6%. In contrast, when a downturn was avoided (seven occurrences), the median return surged to 17.4%. While LPL Research’s base case is that the U.S. economy will avoid recession, another weak month or two of employment data could quickly introduce upside risk of recession.

Summary:

The restart of the Fed’s rate-cutting cycle — especially with equities trading near record highs — has historically been a constructive signal for markets. Still, the recent deterioration in labor market data raises concerns. The end of a long streak of positive monthly payroll prints serves as a cautionary marker, particularly if recession risks begin to build.

At this stage, LPL Research views near-term recession risk as relatively low. Our base case calls for an economy that continues to muddle through, with potential upside to GDP growth supported by a lower fed funds rate, stimulative measures from the One Big Beautiful Bill Act (OBBA), and productivity gains amid easing cost pressures.

From a technical perspective, it is hard to argue with a bull market that is making new highs and powered by cyclical leadership. However, building overbought conditions paired with diverging market breadth suggest this melt-up could be due for some cooling off — something we would consider as a potential tactical opportunity to buy the dip.

Adam Turnquist oversees the management and development of technical research at LPL Financial. His investment career spans over 15 years.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #801342

Read more commentaries by LPL Financial