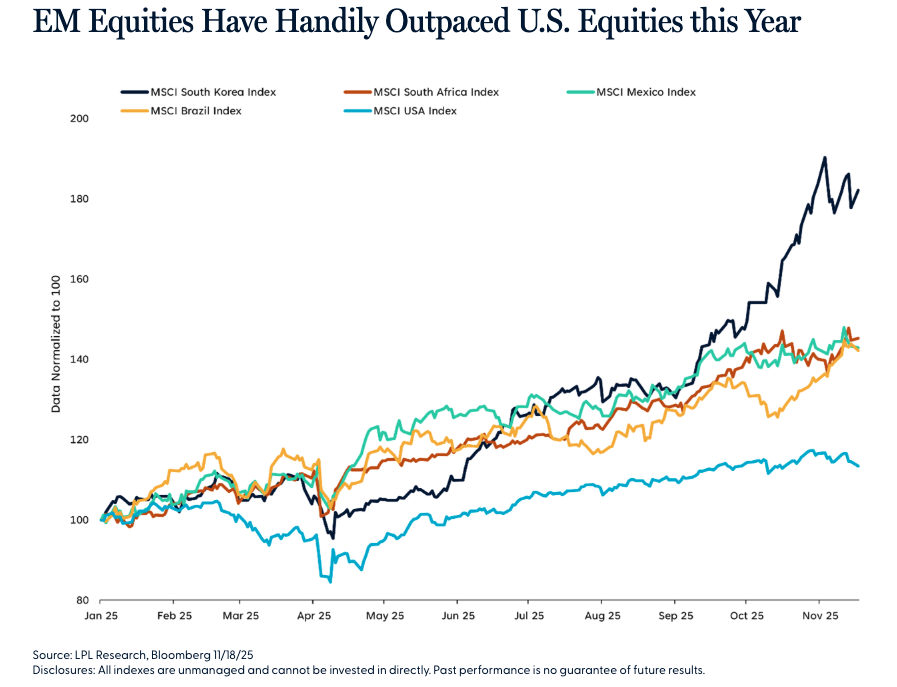

2025 has been an exceptional year for emerging market (EM) equities. South Korea has surged almost 80%, while South Africa, Brazil, and Mexico have each posted gains of more than 40% year to date. Within the MSCI country universe, six of the top 10 performers this year are emerging markets. This level of outperformance relative to the U.S. at the broad asset class level has been rare and, barring a strong late-year rotation, this will mark only the third time in the past 15 years that emerging markets have outperformed U.S. equities.

Can this trend persist or is it merely a one-year aberration? Much of the answer likely depends on the U.S. dollar, as the dollar’s trajectory has historically been the single most important driver of international equity performance compared to the U.S. When the dollar weakens, it encourages capital to search outside the U.S. for investment opportunities; when it strengthens, capital gravitates back to the U.S. in search of returns. These dynamics often reinforce themselves, as we’ve seen over the past decade where dollar strength fueled U.S. equity outperformance, which in turn supported further dollar strength.

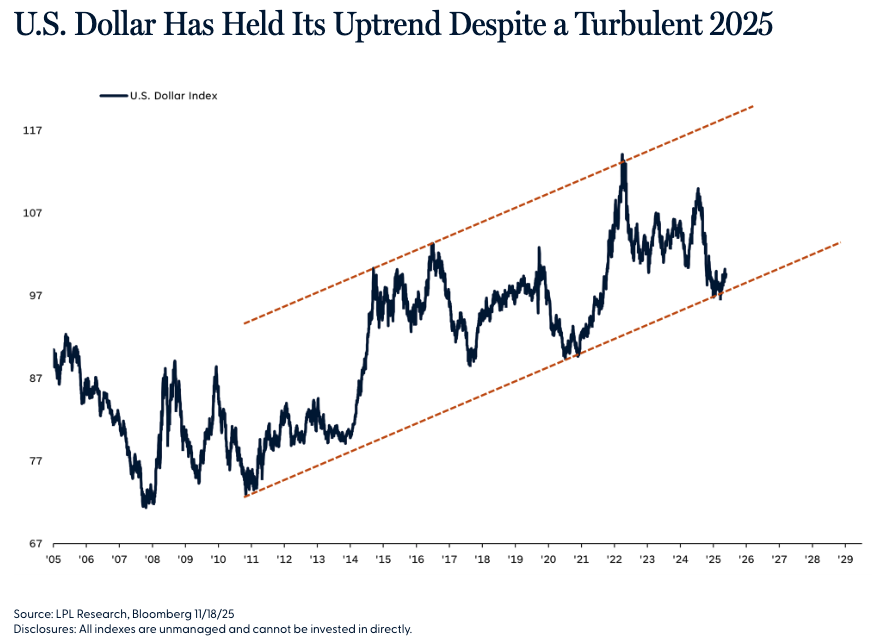

The last extended period of EM outperformance occurred during the 2002–2008 cyclical bear market in the dollar. Over that span, the Dollar Index declined roughly 40% from peak to trough, creating a favorable backdrop for international equities. Interestingly, this episode followed a long period of U.S. dominance during the dot-com boom of the 1990s, when strong dollar conditions and technology-led growth kept global capital anchored in U.S. markets. Fast forward to 2025 and dollar weakness, particularly in the first half, has been a key driver behind strong gains in EM. However, the critical question for investors is whether this year’s move signals the start of a multi-year dollar downtrend similar to the early 2000s, or if it is merely a temporary correction within a longer-term bullish cycle. The evidence so far is mixed. While the Dollar Index is down about 8% year to date and arguably still above fair value, it remains within the broader uptrend that has persisted since 2011.

Historically, sustained dollar weakness and multi-year international equity outperformance have occurred after clear technical breakdowns in the dollar’s chart structure. At present, those signals have yet to materialize and until or unless the long-term trend decisively reverses, it is difficult to be overly bearish on the dollar or, by extension, overly optimistic about a prolonged period of EM leadership.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) recommends well-diversified geographic exposures, with benchmark-level allocations to the U.S., developed international, and emerging markets. Emerging market valuations remain generally attractive, and the technology/artificial intelligence (AI) outlook has improved. From a macro lens, China’s economy has stabilized (the largest country within the asset class) and trade tensions have eased. Nonetheless, the U.S. dollar outlook remains less certain and the technical picture needs to show more clarity before an EM upgrade can be more seriously considered.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #827907

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial