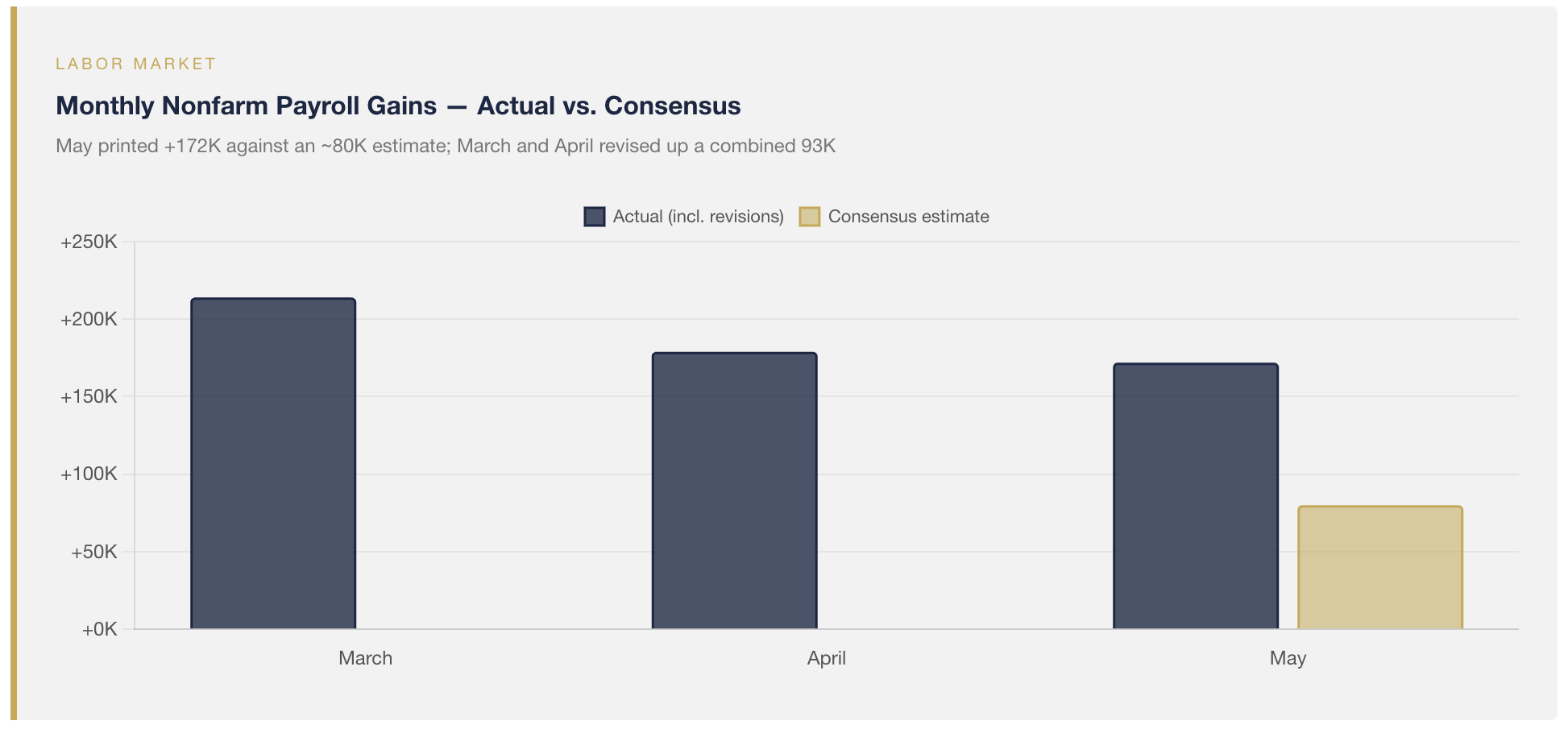

Friday's May employment report did what strong data is supposed to do at this stage of a cycle: it took the last of the rate-cut optimism off the table and forced every asset class that had been leaning on easier policy to re-price in real time. Nonfarm payrolls rose 172,000 in May, more than doubling the roughly 80,000 the consensus had penciled in, and the prior two months were revised up by a combined 93,000 — March to 214,000 and April to 179,000. The unemployment rate held at 4.3%. Average hourly earnings rose 0.3% on the month and 3.4% over the year. By any reading, this was a labor market that is cooling gradually rather than cracking, and the market's response was swift and unforgiving to anyone positioned for imminent easing. We think the reaction was rational. We also think it changes very little about the case we have been making all year.

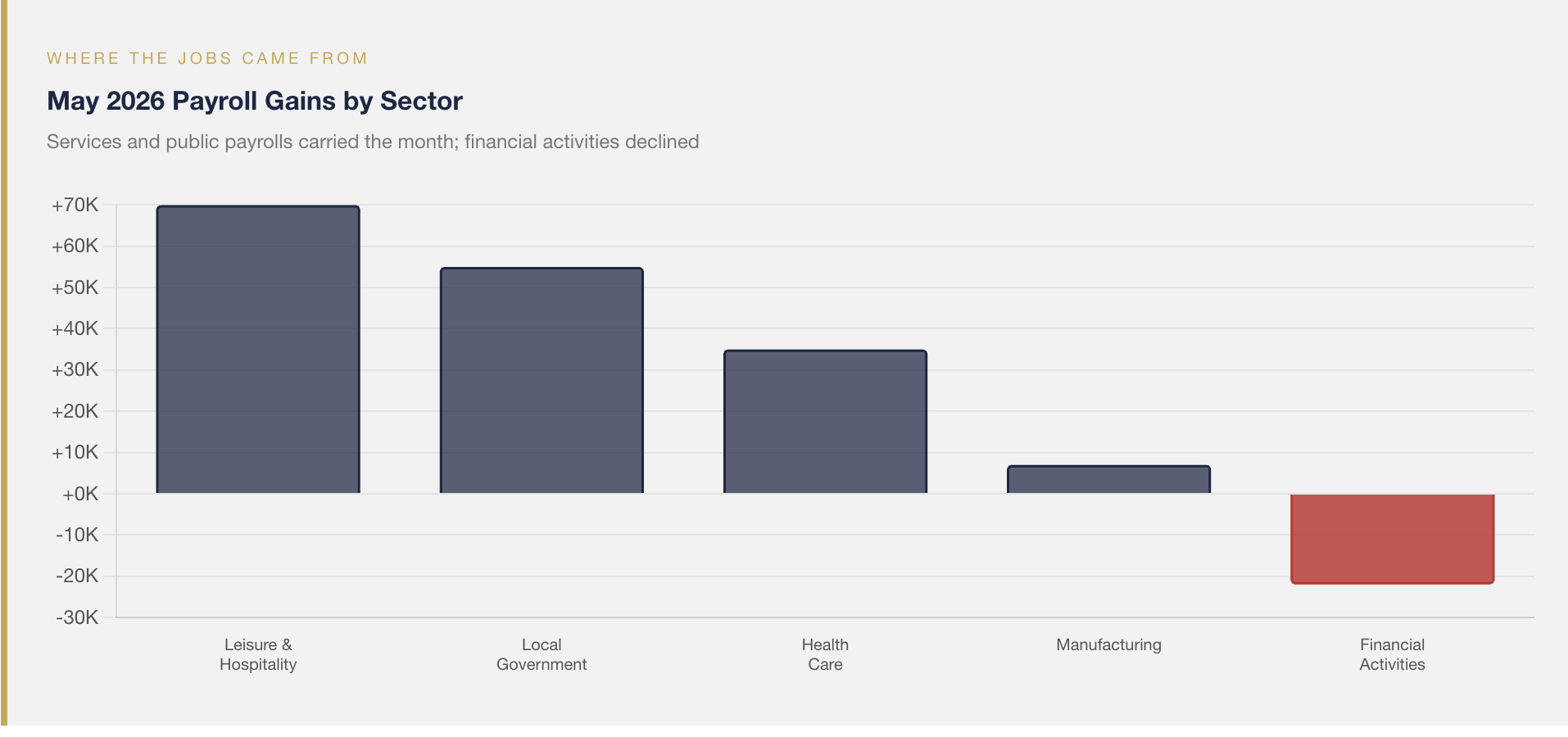

Begin with the print itself, because the headline flatters the internals only slightly. The bulk of May's gains came from leisure and hospitality, which added 70,000 jobs, nearly half of them in food services and drinking places; local government contributed 55,000, health care 35,000, and manufacturing a modest 7,000, while financial activities actually shed positions. This is not the composition of a booming, broad-based expansion — it is the late-cycle mix of services hiring and public payrolls doing the heavy lifting while rate-sensitive and goods-producing sectors stall. But it is also, unmistakably, a number that gives a cautious Federal Reserve every reason to keep sitting on its hands. Job creation comfortably above 150,000, paired with inflation still running above target and widely expected to firm into the summer, leaves both sides of the Fed's dual mandate arguing against cuts. Markets understood the message immediately.

Read more: Soaring Capital Expenditures in the Tech Sector: Good, Bad, or Ugly?

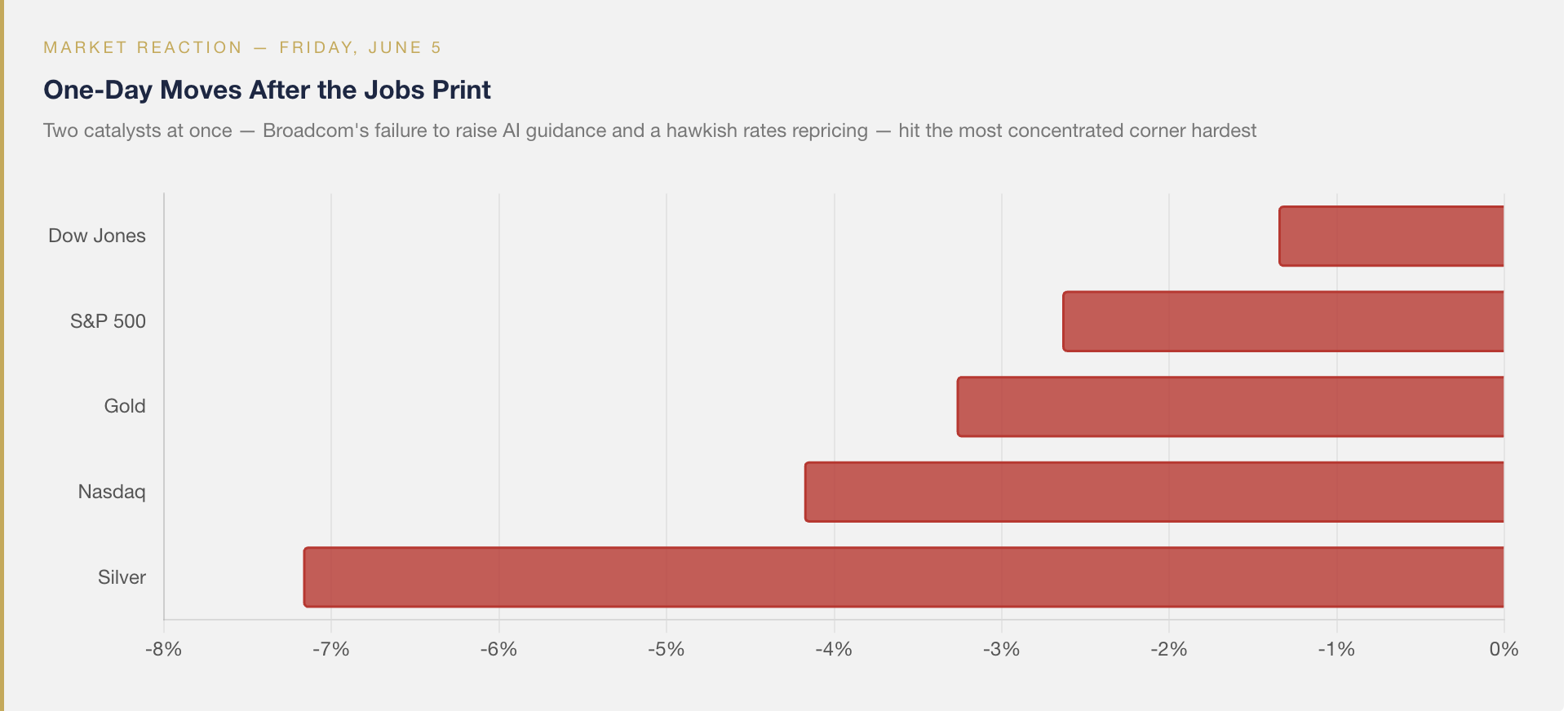

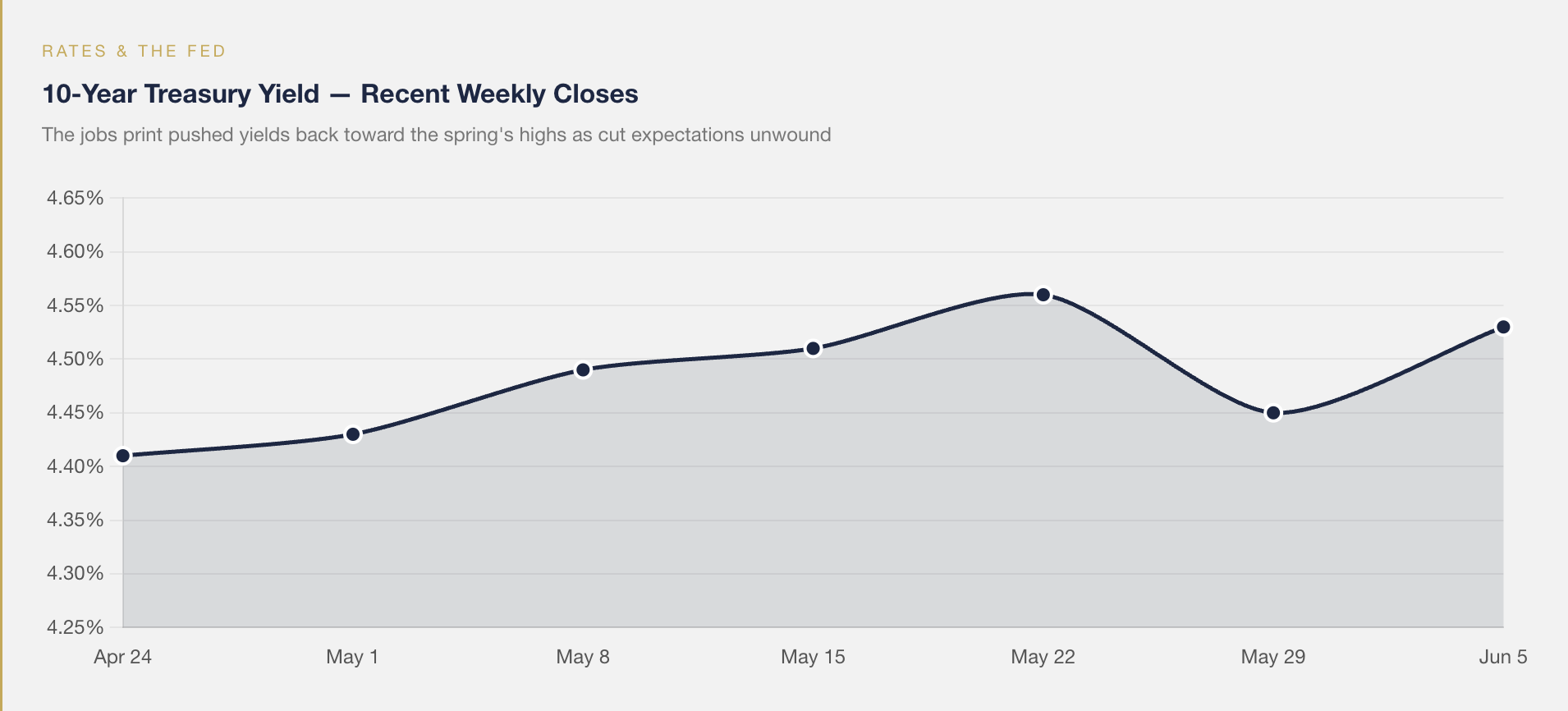

The repricing was violent, but it would be a mistake to lay last week's damage entirely at the Fed's feet, because the chip complex had already been unraveling on a cause of its own. Broadcom, reporting Wednesday evening, actually delivered a record quarter — consolidated revenue up 48% to $22.2 billion, AI semiconductor revenue up 143% — and guided next-quarter AI sales to $16 billion, more than 200% above a year earlier. In an ordinary tape that is a blowout. But the figure landed shy of the roughly $17.2 billion the most aggressive analysts had modeled, and management chose to reaffirm rather than raise its full-year AI target. In a semiconductor group priced for flawless, perpetually accelerating execution — many names trading north of fifty times earnings — “merely excellent” was treated as a failure. Broadcom fell some 14%, and the sell-the-news reaction rippled across the complex: the Philadelphia Semiconductor Index suffered its steepest selloff since 2020, Nvidia shed 6% and briefly surrendered its $5 trillion crown, and AMD and Intel each fell about 11%. Onto that company-specific blow came the macro one: fed-funds futures, which had entered the spring still pricing a chance that Chair Kevin Warsh's first move would be a cut, swung hard the other way, and by Friday's close the implied probability of a rate hike by year-end had climbed to roughly 70%, lifting the ten-year Treasury yield to 4.53% — eight basis points above the prior Friday — with the thirty-year pushing back toward 5%. The two shocks compounded each other in precisely the corner of the market least able to absorb them. The S&P 500 fell 2.6% to 7,383.74, surrendering essentially all of a quietly constructive week, and the Dow gave up 1.3% to 50,866.78, but the Nasdaq Composite dropped 4.2% to 25,709.43 — its worst day since April 2025 — because the indices most levered to the AI capital-spending story are also the most levered to the discount rate applied to it, and last week the story and the discount rate turned at once. That a record quarter from a bellwether could still touch off a rout is itself the risk we have flagged all year in a tape this concentrated: when valuations price perfection, even excellence disappoints.

Gold was not spared, and we want to address that directly rather than around it, because our readers hold it and our conviction in it is well known. The metal fell $146.50, or 3.27%, to settle near $4,339.61, and silver led the complex lower with a punishing 7.2% drop. To anyone watching the screen on Friday, gold looked like just another casualty of higher real yields and a firmer dollar. That read is correct as far as it goes. When the market yanks rate cuts off the table and pushes nominal yields up, the opportunity cost of holding a non-yielding asset rises mechanically, and the most leveraged and momentum-driven money in precious metals gets shaken out first — which is precisely why silver, the higher-beta cousin, fell more than twice as hard as gold. This is a positioning event. It is the kind of technical, sentiment-driven pullback we flagged in late March, when we argued that gold's correction was technical rather than fundamental. Nothing in Friday's data altered the structural reasons gold sits near $4,300 in the first place rather than the $1,800 it traded at a few years ago.

We owe readers the balanced framing we always insist on, and here it cuts in gold's favor as much as against it. The American economy is demonstrably resilient. A labor market still generating 172,000 jobs a month with unemployment at 4.3% is not a recessionary one, consumer spending has held up, and the productivity gains flowing from the AI build-out are real and are genuinely lifting the economy's potential. We have never argued otherwise, and we are not arguing it now. The point is narrower and, we think, more durable: a strong jobs number that closes the door on rate cuts does not repair the fiscal arithmetic underneath the dollar. Federal deficits are still running near 6% of GDP in a full-employment economy, the debt continues to compound at yields above 4.5%, and a Fed that cannot cut without reigniting an inflation problem is a Fed with very little room to socialize the next shock. Higher-for-longer rates relieve the near-term pressure on gold while quietly worsening the long-term debt dynamics that are the metal's deepest bid.

"The short term belongs to the data. The long term belongs to the macro backdrop — unsustainable deficits, a debt load that compounds faster than the economy grows, and a global official sector diversifying out of the dollar — and that backdrop did not change on Friday."

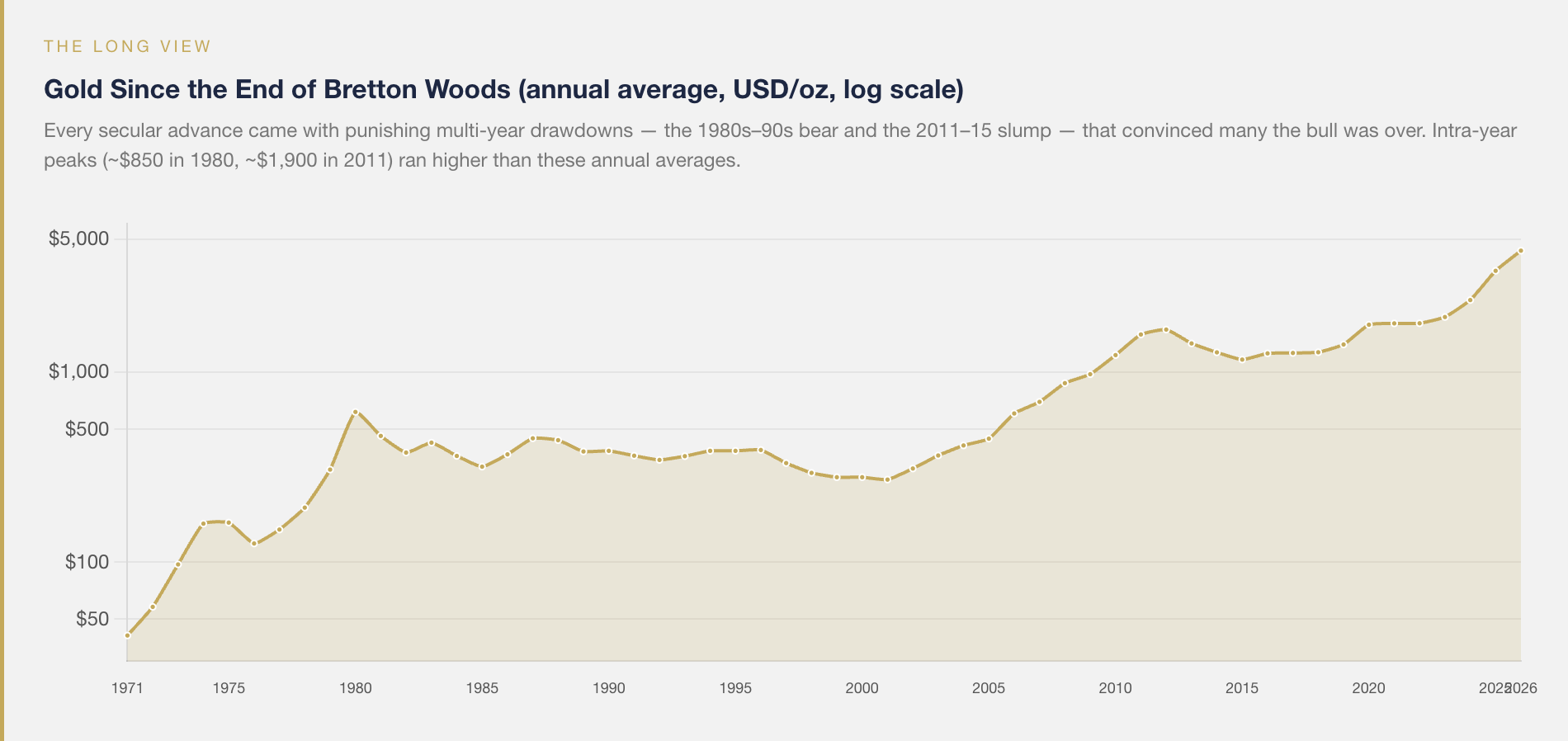

That long-term bid is worth grounding in history, because gold's detractors reliably mistake the short for the structural. When the United States severed the dollar's last link to gold in 1971 and entered a decade of deficits and accommodative policy, gold ran from $35 an ounce to roughly $850 by January 1980 — and it did not do so in a straight line, suffering a brutal nearly 50% drawdown in the mid-1970s that convinced many the bull market was finished, just before its largest leg higher. In the 2000s, against a falling dollar, chronic twin deficits, and negative real interest rates, gold rose from about $250 at the start of the decade to roughly $1,900 by 2011, an eightfold move that again was punctuated by gut-checking corrections along the way. The pattern is consistent: gold's secular advances are driven by fiscal and monetary debasement, not by the month-to-month path of the funds rate, and they are repeatedly interrupted by exactly the kind of yield-driven setback we saw on Friday.

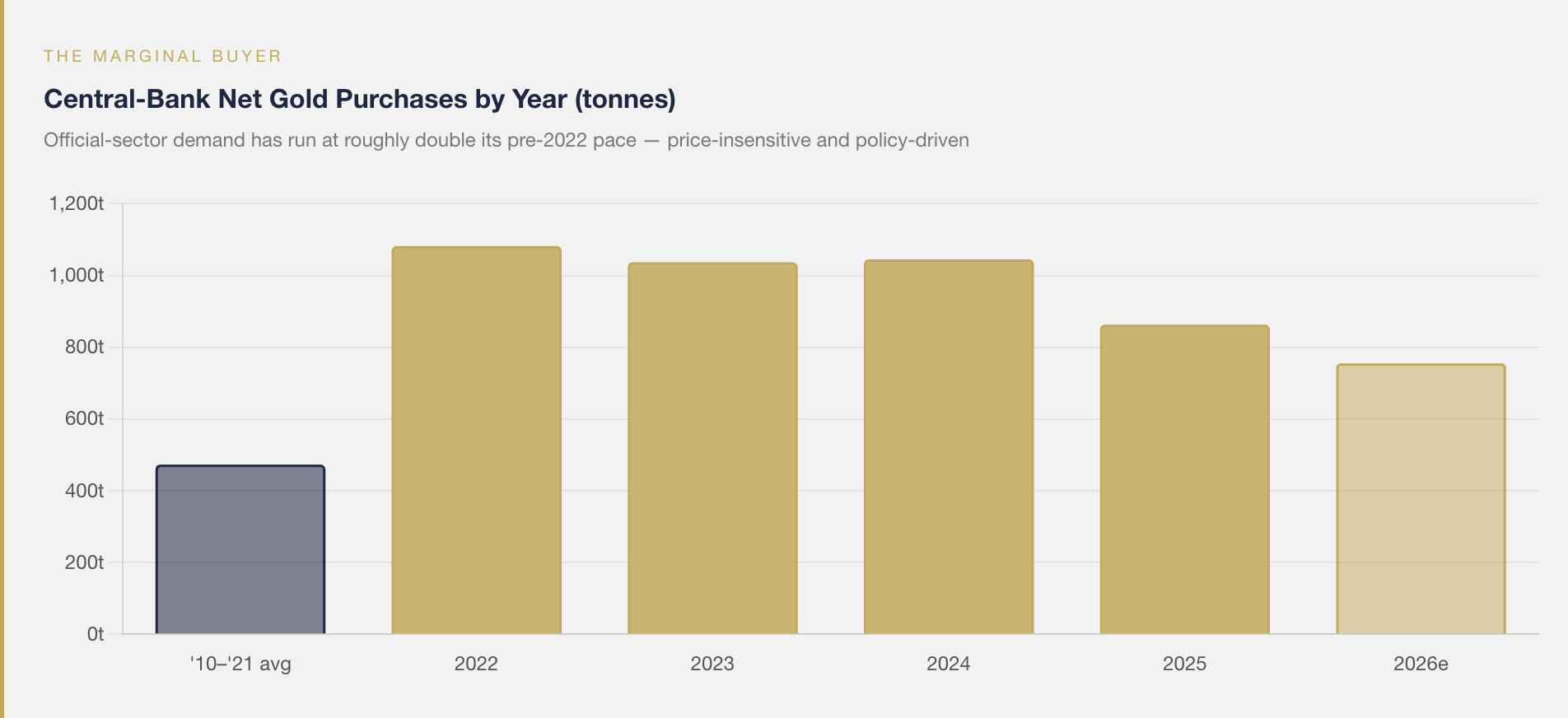

The present setup rhymes with those episodes more than it differs from them, and the marginal buyer has changed in gold's favor. Central banks purchased 863 tonnes of gold in 2025 and are on track for roughly 755 tonnes in 2026 — figures that sit well above the 400-to-500-tonne norm that prevailed before 2022, when the freezing of Russia's reserves taught every non-Western central bank a lasting lesson about counterparty risk in dollar assets. This is price-insensitive, policy-driven demand that does not flinch when the ten-year yield rises eight basis points, and it is a structural support that simply did not exist in prior cycles. Even after Friday's selloff, gold is up roughly 34% over the past year, and the major banks that move institutional money are clustering their year-end targets in the $5,000-to-$6,000 range. We do not traffic in price predictions, but we note the direction of the smart-money consensus has not turned on a single payrolls print.

So we read last week as a repricing, not a reversal. The short term belongs to the data, and the data on Friday was strong enough to send yields up, equities down, and gold through a technical air pocket. The long term belongs to the macro backdrop — unsustainable deficits, a debt load that compounds faster than the economy grows, a central bank boxed in by its own inflation problem, and a global official sector steadily diversifying out of the dollar — and that backdrop did not change on Friday. For the dollar-based investor, episodes like this one are not a reason to abandon hard-asset exposure; historically they have been among the better moments to own it. A portfolio that pairs international value equities with a meaningful allocation to gold is built precisely for a world where the nominal tape is volatile and the real story is the slow erosion of the currency it is priced in. If you would like to discuss how this positioning applies to your own circumstances, we invite you to speak with a Euro Pacific Asset Management advisor or visit EuroPac.com.

Investment risk

Please read about the Risks of investing in the Funds. You should carefully consider the Fund’s investment objectives, risk, charges and expenses before investing. Investing involves risk, including potential for loss of principal. The risks of investing in emerging market and foreign securities may be higher than the risks associated with investing other securities. Diversification cannot assure a profit or protect against loss in a down market. Dividends are not guaranteed and may fluctuate. Fund holdings are subject to change and risk. Past performance cannot predict future results.

To obtain a prospectus or summary prospectus that contains this and other information about the Funds, please Click Here or call 1-866-878-2881. Please read the prospectus carefully before investing. Euro Pacific Asset Management Funds are distributed by Distribution Services, LLC (Euro Pacific Asset Management is not affiliated with Distribution Services, LLC).

Disclosure: Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and it is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Funds nor any of its representatives may give legal or tax advice.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Euro Pacific Capital

More Innovative ETFs Topics >