AI’s Expansion Runs on Smaller Companies

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

- Specialized memory chips and traditional central processing units (CPUs) have joined graphics processing units (GPUs) as key enablers of artificial intelligence (AI) workloads and agents. In addition to a greater range of chips supporting AI development, several other factors could cause the current cycle to last longer than expected.

- Durable demand for chips to run inference workloads has expanded the supplier base to include companies developing application-specific integrated circuits as well as hyperscalers producing silicon in-house.

- We see the availability of server power components as the next gating factor in building out AI capacity, highlighting the importance of analog companies manufacturing power management chips.

- Memory remains a key source of upside, with tight high-bandwidth memory and Dynamic Random Access Memory (DRAM) supply likely to underpin stronger pricing and earnings through 2027.

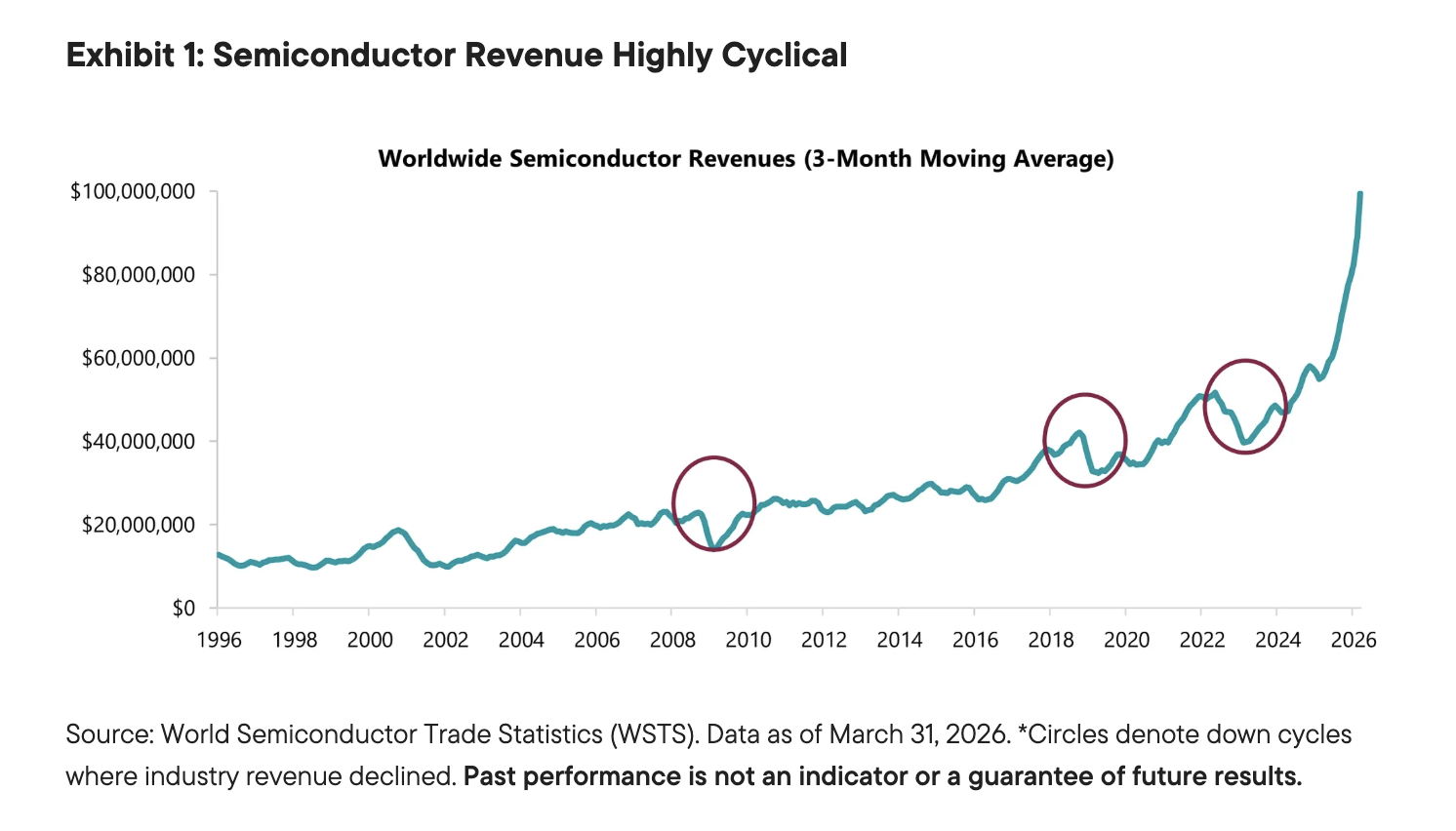

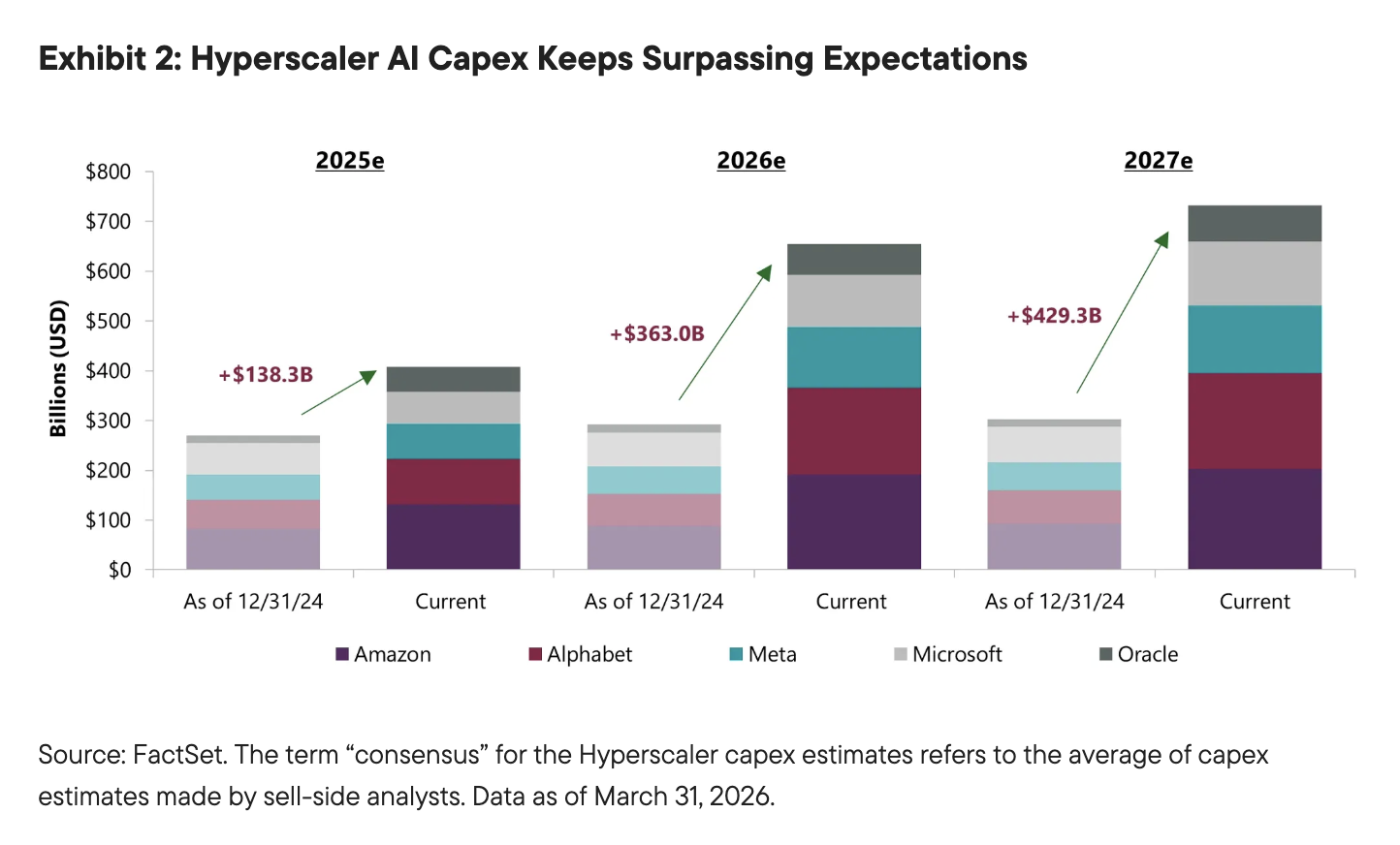

Accelerating capital spending on AI buildouts by mega-cap hyperscalers and emerging AI model developers continues to surpass expectations. The positive trajectory of capital expenditure (capex) has supported equity performance across the semiconductor industry, with memory players seeing particularly strong gains. Just as skepticism has emerged over the potential return on investment from an unprecedented period of capex, investors have also begun to raise concerns over the duration of the current semiconductor cycle (Exhibit 1).

Read more: A Repricing, Not a Reversal

The semiconductor industry has historically proven volatile through waves of technology innovation where chip demand has increased faster than available supply, yet we believe the unique and expansive nature of generative AI could elongate and reduce the severity of the traditional boom/bust cycle (Exhibit 2).

Overall chip demand continues to inflect much faster than supply as the generative AI revolution has transformed what the installed enterprise technology base needs to be. Adding supply, especially for high-end applications, can be an especially lengthy process. For example, an extreme ultraviolet lithography machine that etches intricate circuit patterns required to produce leading-edge chips can take six to 12 months to manufacture and ship to a customer. Indeed, supply is constrained by both physics as well as the production capacity of semiconductor capital equipment makers and leading foundries, especially when building the foundation for an all-new type of compute.

While GPUs have been the workhorse of initial generative AI development, specialized high-bandwidth memory (HBM) chips as well as traditional CPUs are playing increasing roles as more companies develop cloud capabilities to host AI workloads and offer AI agents. In addition to a greater range of chips supporting AI development, we believe three factors could cause the current cycle to last longer than expected.

The first is the durability of inference silicon demand. In addition to market leader Nvidia, other chip companies have seen strong uptake for their application specific integrated circuits (ASICs) designed for inference functions—the outputs produced by commercial large language models. More recently, traditional CPU makers, logic chip designers and newly public AI chip designers have reported growing demand from model developers for silicon to support not only processing but also networking and connectivity. Meanwhile, to better control supply in a constrained market for chips to support AI workloads and to customize silicon for their own needs, several hyperscalers are also producing semiconductors in-house.

The second trend supporting the semiconductor cycle is the increasing power required to efficiently and effectively operate server racks in data centers. We see the availability of server power components as the next gating factor in building out further AI capacity. Analog semiconductors makers produce power management chips that deliver and regulate the precise voltage requirements for servers based on workload intensity. Tightening capacity is causing customers to pay higher prices for analog power chips—from 5% to 20% higher—to ensure available supply. We believe the diversity of customers in this market, a function of more chip makers adding value across the AI supply chain, should help smooth out previous volatility among analog stocks. Notably, the AI tailwind from power management is occurring in conjunction with a broader cyclical recovery in the analog segment.

Memory still a long way from equilibrium

The third driver of visible semiconductor demand is the memory market. Surging demand for DRAM has created a super cycle that we see lasting through 2026 and into 2027 as model developers scoop up HBM, which are a specialized form of DRAM. These products stack DRAM chips together to enable parallel processing. The HBM market is consolidated, with just three primary suppliers globally. DRAM prices are expected to increase for the rest of 2026 and flow directly into supplier earnings. We believe consensus forecasts still underestimate the pricing power these companies maintain.

Not nearly enough DRAM supply has been built in the current cycle. This is due to HBM consuming three to four times more silicon wafers than traditional DRAM. In addition, the top three HBM suppliers currently do not have enough cleanroom space to build for the type of demand we see. The six to nine months it takes from equipment installation to product distribution is one driver of an extended memory up cycle.

What makes this upcycle different is the accelerated growth of HBM, which is sold under longer-term contracts at prices agreed upon before the current supply crunch—which locked in margins that are now running below those of commodity DRAM. That gap is a supply-and-demand story: Commodity DRAM has no such price agreements, so its pricing moves freely with the market, and right now a severe supply shortage is pushing those spot prices—and margins—sharply higher.

HBM is also far more wafer-intensive to manufacture than commodity DRAM, meaning a given amount of fabricator (fab) capacity produces significantly fewer units. That constraint tightens supply across memory types, not just HBM—and it is one reason commodity DRAM margins have improved sharply, as demand continues to outpace what fabs can deliver. It also reduces the risk of an oversupply glut when HBM demand eventually cools, since production cannot be ramped quickly.

In a period where generative AI compute capacity is so constrained, primarily due to supply shortages, and capex appears likely to continue moving higher, the tide has the potential to lift many boats in AI-related semiconductor segments. We expect leading edge capacity to remain tight well into 2027, and possibly into 2028. As supply and demand eventually reach equilibrium and the current constraints are released, however, we expect the best operators in compute (GPU and CPU) and analog to stand out as durable growth winners. We also see the possibility of the memory cycle remaining stronger for longer due to the unique characteristics and increasing revenue mix of HBM.

DEFINITIONS

Capital expenditure (capex) refers to investment spending in long-term assets (fixed assets). These expenditures include new buildings, machinery, and other equipment needed for an organization's day-to-day operations. Most companies use capex financing to fund their long-term investments.

Hyperscalers are companies that own and operate massive data centers to provide highly scalable cloud computing services like Infrastructure as a Service (IaaS) and Platform as a Service (PaaS).

A CPU (Central Processing Unit) is the primary component of a computer that acts as its "brain."

A GPU (Graphics Processing Unit) is a specialized electronic circuit designed to rapidly process and render images, video, and computer graphics.

Dynamic Random Access Memory (DRAM) is the standard type of temporary "working" memory (RAM) used in most desktop computers, laptops, and smartphones.

High Bandwidth Memory (HBM) is an emerging type of computer memory that is designed to provide both high-bandwidth and low power consumption. Typically, it will be suited and used in high-performance computing applications where that data speed is required. HBM uses a 3D stacking technology.

An Application-Specific Integrated Circuit (ASIC) is a microchip custom-designed to perform a single, specific task rather than intended for general-purpose use.

A semiconductor cleanroom space is an ultra-sterile, highly controlled manufacturing environment. Designed to eliminate microscopic dust, chemical vapors, and static electricity, it protects fragile silicon wafers during chip fabrication.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

To the extent the portfolio invests in a concentration of certain securities, regions or industries, it is subject to increased volatility.

Equity securities are subject to price fluctuation and possible loss of principal.

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

Investment strategies which incorporate the identification of thematic investment opportunities, and their performance, may be negatively impacted if the investment manager does not correctly identify such opportunities or if the theme develops in an unexpected manner. Focusing investments in the information-technology-related sectors carries much greater risks of adverse developments and price movements in such industries than a strategy that invests in a wider variety of industries.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

WF: 10931010

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits