Milton Friedman’s famous one-liner that anchors half the inflation debates on financial television leaves out the part where the actual economics live. Once you put it back in, the doomist case gets a lot smaller.

Per Bylund recently wrote a sharp piece for The Daily Economy arguing that CPI and GDP have become Goodhart’s Law in action. When a measure becomes a target, it ceases to be a useful measure. He has a point, and we’ll come back to it. But the bigger problem with the inflation conversation isn’t really about CPI. It’s about the way the famous Milton Friedman inflation quote gets weaponized by people who almost certainly haven’t read past the comma.

The line you always hear is, “Inflation is always and everywhere a monetary phenomenon.” Full stop. Print money, get inflation, or corporations cause inflation. Then, the doomers grab a chart of M2 and a warning about hyperinflation.

That’s not what Friedman actually said.

What Friedman Actually Said

The complete sentence is,

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

That trailing clause changes everything.

The monetary doomists drop it because it complicates the bumper sticker. But “than in output” is where the real economics is.

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work. Friedman’s claim was that, over the long run, sustained changes in the general price level can come only from money growing faster than the economy’s productive capacity. Supply was already inside his framework. A collapse in output with steady money produces the same price effect as money growth with steady output.

So the “supply and demand drives inflation” intuition isn’t competing with Friedman. It’s living inside his model. The question is whether the imbalance persists, which depends on whether monetary policy accommodates it.

The Distinction Everyone Misses

Friedman drew a hard line between relative price changes and sustained inflation. That distinction is what gets lost in the modern debate.

When oil prices spike due to a war, consumers spend more on energy and necessarily less on everything else. Relative prices shift. Energy goes up, discretionary goods come under pressure. The general price level doesn’t have to rise unless monetary policy expands the money available to spend on everything. Without that accommodation, you get a one-time level shift in the price index, and then prices stabilize. That’s not inflation in Friedman’s sense. That’s a relative price adjustment.

This is why Friedman could call inflation “a monetary phenomenon” without being naive about supply shocks. He simply argued that supply shocks alone don’t produce sustained inflation. They produce volatility around a level. The trend in the level comes from the money side.

Here’s the problem with how this gets used today. Both the inflation alarmists and the cable news pundits flatten the distinction. The doomists see any money growth and forecast persistent inflation, ignoring that velocity might collapse and absorb the expansion. The pundits see any price spike and call it inflation, ignoring that without monetary accommodation, it’s likely to fade.

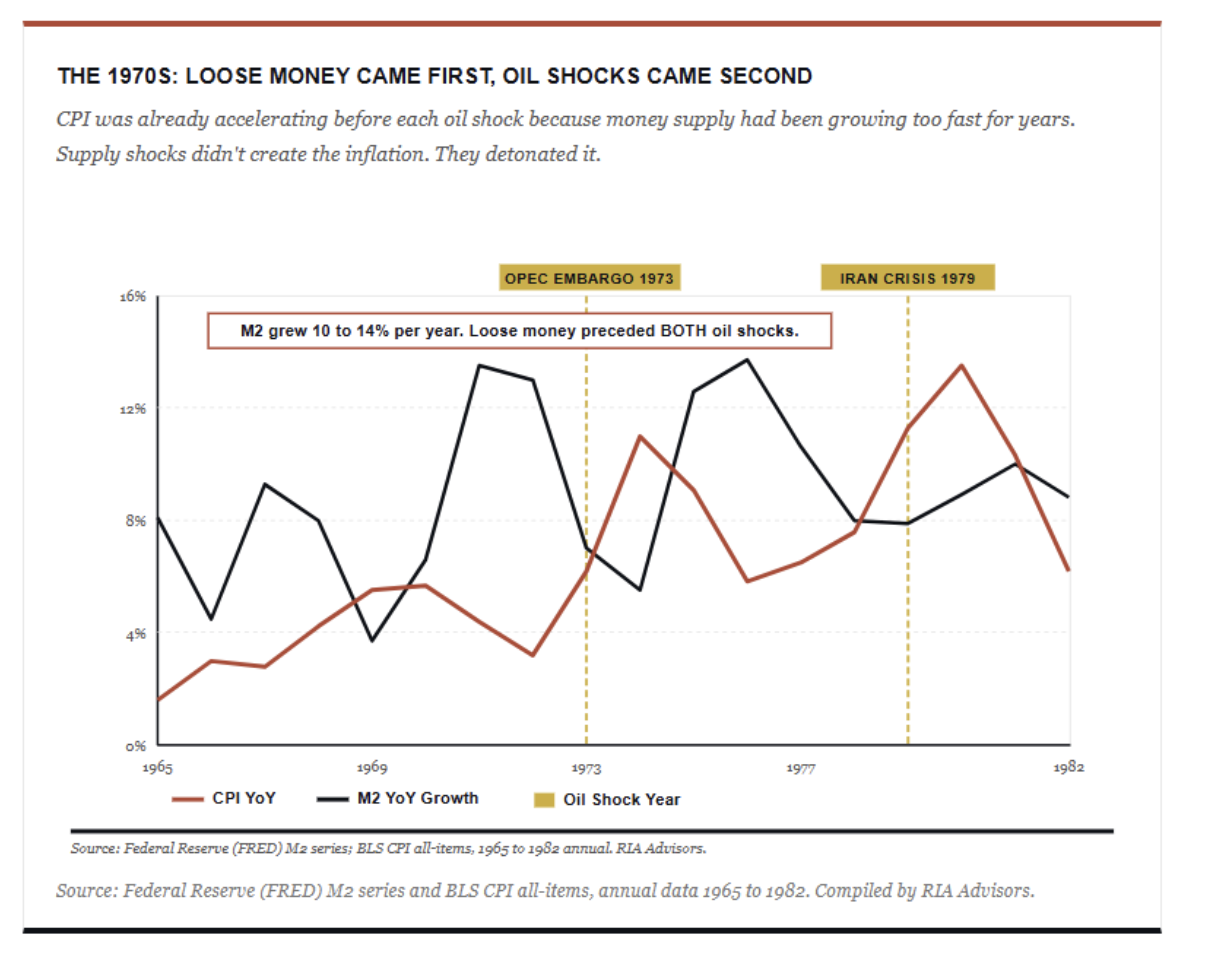

The 1970s are the clearest historical illustration of why both supply and money must be present for sustained inflation. Most people remember the decade as an “oil shock” story, but that’s only half right. CPI was already running hot before the 1973 Arab oil embargo and again before the 1979 Iranian revolution.

Money supply growth had been excessive for years, and interest rates had been held too low. The oil shocks didn’t create inflation out of nothing. They pushed an already-loosened cork out of an already-pressurized bottle. Lacy Hunt has been making essentially this argument about the current setup, and he’s right to flag the parallel. A supply shock landing on top of loose money is the configuration that produces a sustained inflation problem. A supply shock landing on a disciplined monetary base produces a level shift that fades.

Read more: Tech Rally Grounded in Fundamentals

Money Has to Grow for the Economy to Grow

Here’s where the doomist case really starts to fall apart. The accusation is that “money printing causes inflation.” But in a modern fiat system, every dollar of money in circulation is debt. Either it’s a commercial bank loan that created a deposit on the other side of the ledger, or it’s government borrowing financed through the banking system. There is no third option.

The Bank of England’s 2014 paper, Money Creation in the Modern Economy, laid this out explicitly. Banks don’t lend out reserves. They create deposits when they make loans, and the reserves are created in parallel. So the entire monetary base is, in a real sense, debt that has to be serviced with growing nominal income.

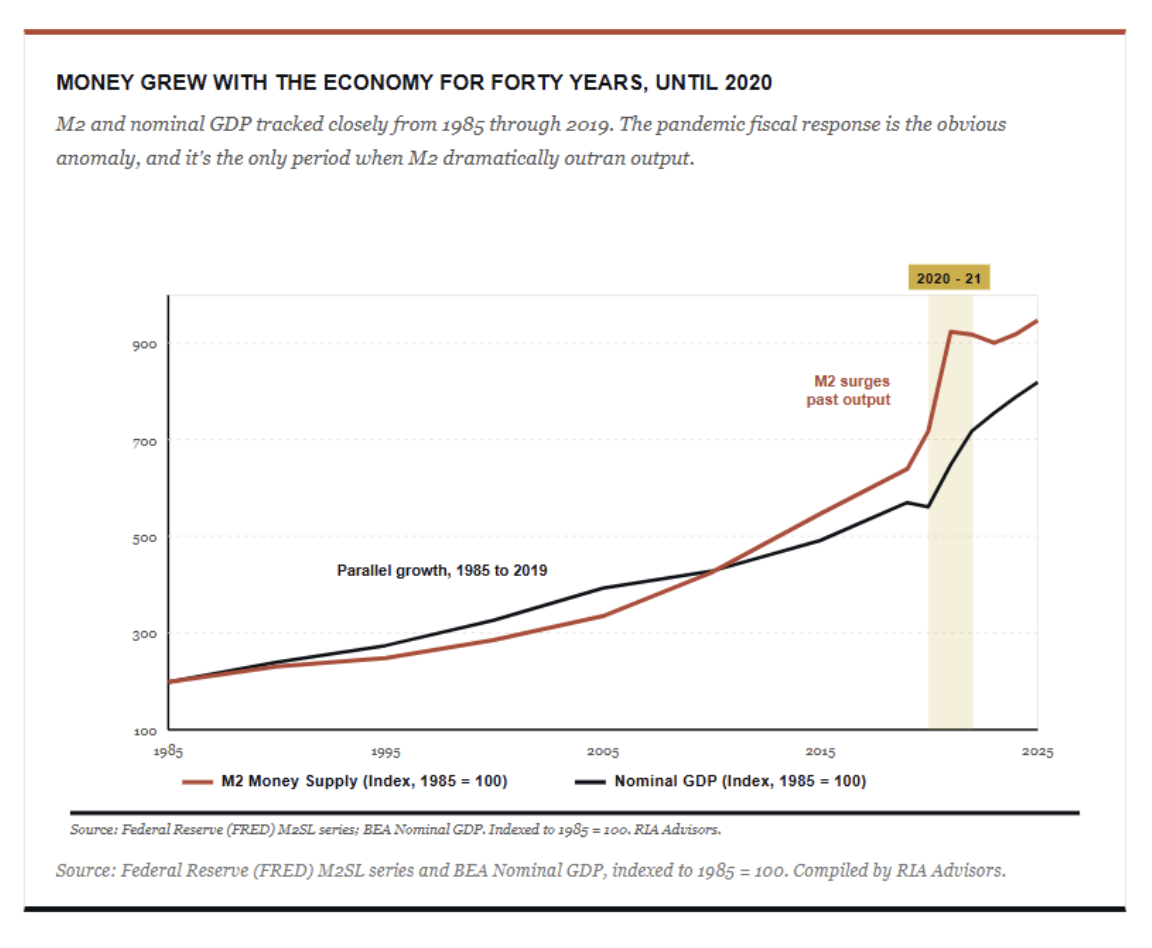

That has a structural implication that most armchair monetarists miss. If money doesn’t grow, the economy can’t grow either. Real debts (fixed in nominal terms) become heavier as nominal income stagnates. Defaults cascade. Credit contracts. You get 1933, which is exactly what Irving Fisher described in his debt-deflation theory. The system is built to require expansion.

So when someone screams about M2 going up, the relevant question isn’t whether M2 went up. M2 has to go up. The relevant question is whether it went up faster than the economy’s productive capacity could absorb it. That’s the real Friedman test, and it’s a much higher bar than the doomists set.

“In a debt-based system, the question isn’t whether money grew. Money has to grow. The question is whether it grew faster than what the economy can produce.”

Velocity Is the Missing Variable

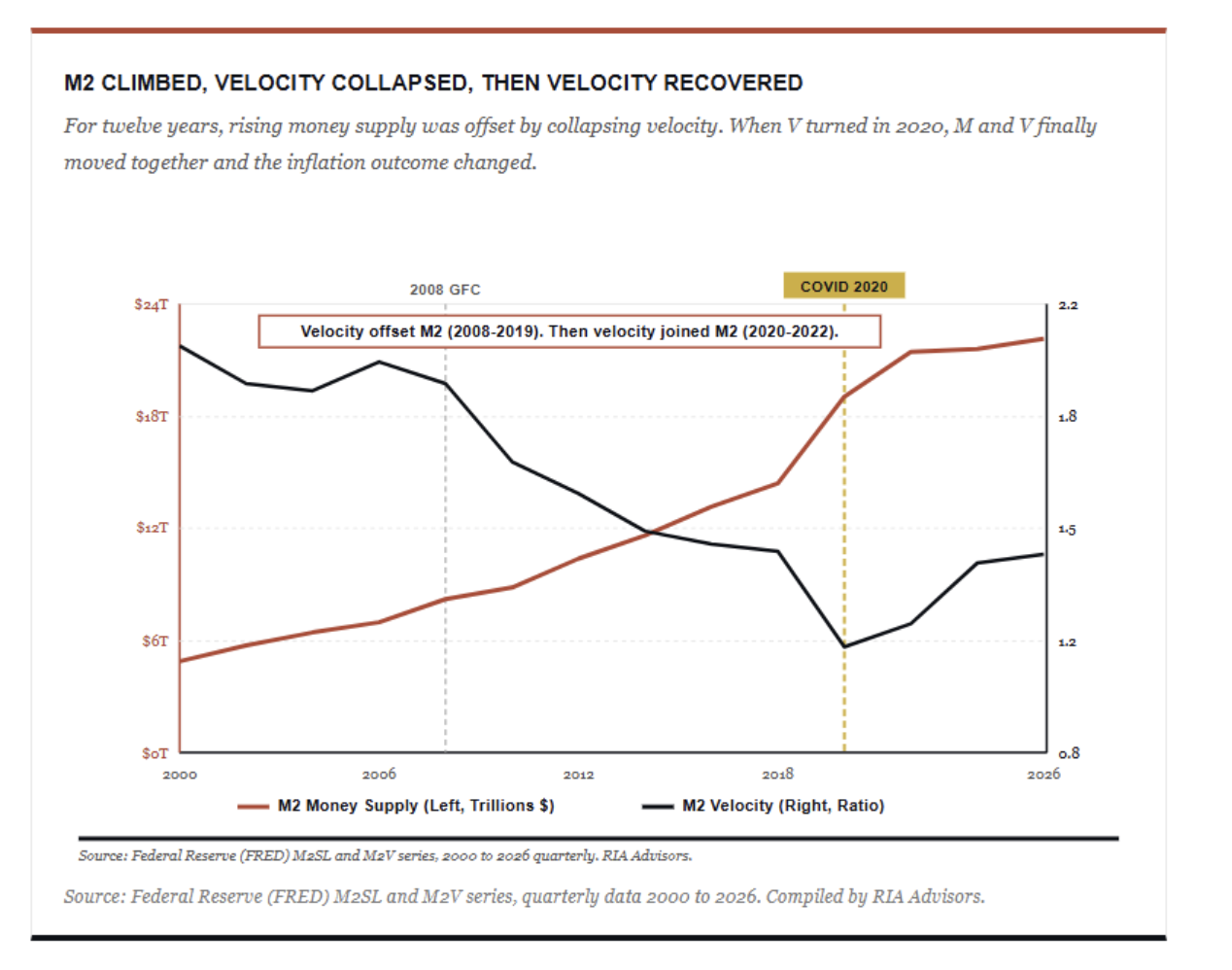

The other piece almost nobody talks about is velocity. MV = PQ has four variables, not three. And V, the rate at which money circulates through the economy, is wildly unstable. Ignore it, and you get inflation forecasts that look ridiculous in hindsight.

Consider the cleanest natural experiment we’ve ever had. From 2008 to 2020, the Federal Reserve expanded its balance sheet by trillions through three rounds of quantitative easing. The doomists screamed about hyperinflation for the entire decade. It never came. Why? Because velocity collapsed. Banks parked the new reserves rather than lending them. Consumers deleveraged rather than spent. The money sat still. M went up, but V went down by roughly the same amount, and PQ barely moved.

Then 2020 happened. The Fed expanded the balance sheet again, but this time the government also sent stimulus checks directly into consumer bank accounts. Supply chains broke. Workers stayed home. And velocity, instead of falling, recovered. You had money growing fast, money circulating again, and productive capacity disrupted, all at once. Inflation hit 9.1% by June 2022.

That’s the cleanest example we’ll ever get of why the simple “M2 up means inflation up” framework is incomplete. Inflation emerged when M, V, and the supply constraint on Q all moved in the same direction simultaneously. The doomists were wrong from 2009 to 2020 because they ignored V. The “transitory” crowd was wrong in 2021 because they underestimated how all three would compound.

And now here we are in 2026, with a setup that’s worth watching closely. The Fed restarted bill purchases earlier this year, calling it a technical operation to ease strain in the repo market. Whatever the label, bank lending has surged. Loans and leases are growing at a 10% annualized pace. Commercial and industrial lending is running closer to 20%. Money supply is accelerating again. This is no longer a 2009-to-2020 regime where money sits idle on bank balance sheets.

The money is being put to work, the velocity question is firmly on the table, and the Treasury’s pivot to short-term bill issuance is forcing the Fed to operate at the short end of the curve whether it wants to or not. That’s the setup Friedman would have flagged. Money plus velocity plus a fiscal-monetary configuration that looks an awful lot like accommodation.

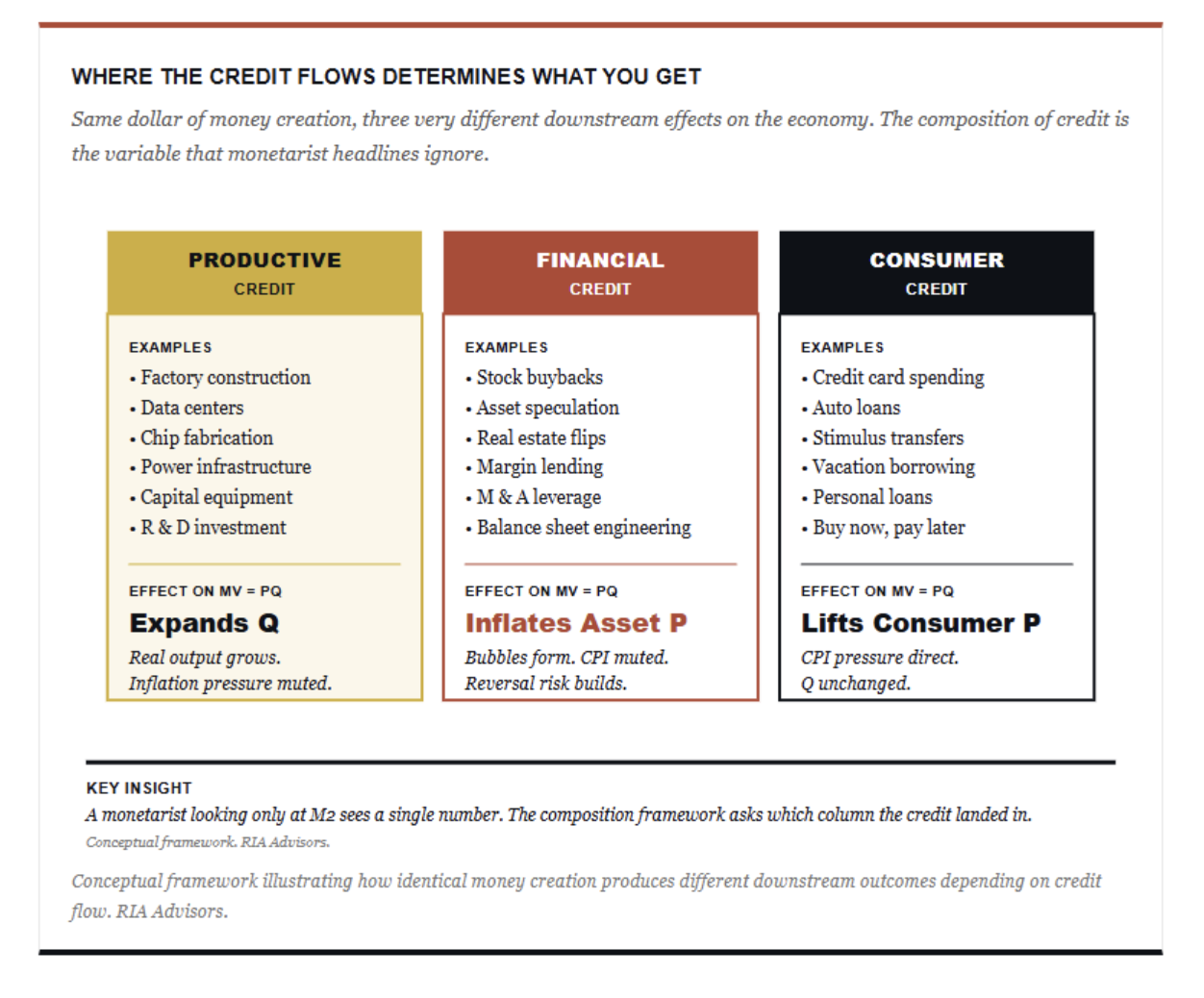

The Composition of Credit Matters More Than the Quantity

Beyond velocity, there’s a second piece that the bumper-sticker monetarism completely misses. Where the credit flows matters as much as how much credit gets created.

A dollar lent to build a factory expands future productive capacity, but a dollar lent to fund a stock buyback inflates current asset prices without expanding the economy’s productive capacity. A dollar lent to a consumer for a vacation expands current consumption without leaving any productive residue. Same dollar, same “money creation,” very different downstream effect.

The Austrians, including the school from which Bylund writes, have a real point here that monetarists routinely flatten. When credit funds are invested in malinvestment rather than productive capital, you can have apparent “growth” that’s really just hollowing out the productive base while inflating asset prices. Most of the post-2008 era worked exactly like this. Credit aggregates exploded, but the flow disproportionately went into financial assets, real estate, and corporate balance-sheet engineering. Consumer prices didn’t move much. Asset prices went vertical. That’s not inflation in the CPI sense. But it’s also not “growth” in any meaningful sense either.

The current AI capex boom is the live test of this framework. The bank lending surging through the financial system right now appears to be funding data centers, chip fabs, power infrastructure, and the related buildout. That’s productive credit by definition, as it expands future capacity to produce. If that’s what’s happening, the inflation impact of the recent money growth should be more muted than the simple M2 chart suggests, because Q is being expanded alongside M.

If, on the other hand, a large share of this credit is funding speculative valuations rather than real capacity, you get the Austrian outcome. Asset prices go vertical, productive capacity doesn’t expand to match, and the inflation eventually shows up either in consumer prices or in a brutal asset-side reversal. We won’t know which scenario we’re in for another year or two. But the framework tells you exactly what to watch. Track where the credit is landing, not just how much of it is being created.

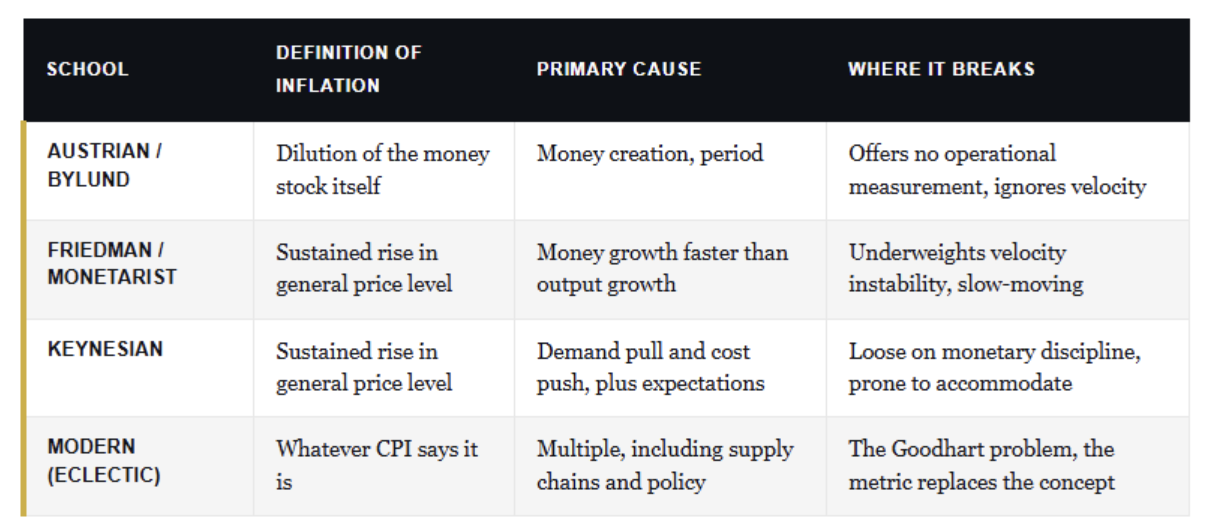

How Different Schools Define Inflation

The reason these debates feel like everyone is talking past each other is that the underlying definition of inflation differs across schools. The table below lines up where each tradition starts and what it treats as the cause.

That last row brings us back to Bylund. His argument is that CPI and GDP have ceased to be useful measures because they’ve become policy targets. Goodhart’s Law in action. He’s not wrong about that. Price controls don’t fight inflation. They suppress the symptom (measured CPI) while worsening the disease, which is real shortages and capital misallocation. The 1971 Nixon wage-price controls are the textbook case. Government spending that produces no productive output really does inflate GDP without inflating wealth. The Soviet Union had impressive GDP growth on paper for decades before it collapsed because the “output” wasn’t producing things anyone valued.

So far, so good. But here’s where the critique runs into a wall. Bylund attacks the measures without proposing how policymakers, central banks, investors, or ordinary readers should actually operate without them. “Just understand the underlying concept better” isn’t operational. The Fed has to make decisions, allocators have to deploy capital, and investors have to make portfolio choices. You can’t run a $27 trillion economy on Austrian methodological purity.

Yes, CPI is flawed. Every serious economist knows it, but the answer isn’t to abandon measurement. It’s about using multiple measures rigorously, understanding their limitations, and triangulating. PCE, trimmed-mean CPI, sticky-price CPI, the Cleveland Fed’s median CPI, and M2 velocity-adjusted measures of money. These exist precisely because thoughtful people know any single number is insufficient. The “experts” Bylund attacks for treating CPI as ground truth are largely a strawman of cable news pundits and political talking points, not the actual analytical community.

What This Means for Investors

The bottom line is that both ends of the inflation debate are wrong in mirror-image ways. The doomists who quote Friedman as “money printer go brrr” stripped away the second half of his sentence, ignored velocity, and missed a decade of disinflation that should have updated their model. The CPI-is-everything crowd ignored the monetary side and got blindsided in 2021 by an inflation surge they kept calling transitory.

The synthesis that actually survives contact with the data is this. Sustained inflation requires money and velocity growing faster than productive capacity. In a debt-based system, money has to grow, so monetary expansion alone isn’t a signal of anything. The real signal is when the growth of money times velocity decouples from the growth of real output. That’s the Friedman test as he actually wrote it, and it’s still the right test.

For portfolios, this means that you should NOT:

- React to M2 data in isolation; look at M2 times velocity together.

- React to single CPI prints, look at the trimmed mean, and the sticky components.

- Assume government spending creates growth just because it shows up in GDP, ask whether it actually expanded productive capacity or just shuffled financial claims.

- Treat the measures as imperfect signals, not as ground truth, but don’t pretend you can invest without them.

There’s one more thing worth flagging for 2026. The Treasury is now funding a deepening deficit by tilting heavily toward short-term bill issuance, with the share of bills in total outstanding debt exceeding the 20% ceiling the Treasury Borrowing Advisory Committee recommends. When the borrower of last resort floods the short end of the curve, the central bank is pulled into providing liquidity there, whether it wants to or not.

That’s the textbook definition of fiscal dominance, and it’s the configuration that turns a discretionary central bank into an accommodator. Combine that with the bank lending surge and the AI-driven credit boom, and the relevant question for investors isn’t whether the Fed will tighten policy. The relevant question is whether the fiscal setup will leave the Fed any room to tighten in the first place.

That’s how you take Bylund’s Goodhart critique seriously without throwing out the analytical toolkit. And it’s how you read Friedman without becoming a caricature of him.

Sources:

- Friedman, Milton. The Counter-Revolution in Monetary Theory, Institute of Economic Affairs, 1970. Full text of the “always and everywhere” passage.

- Bylund, Per. “CPI Meets Goodhart’s Law: Can Economic Metrics Become Fallacies?” The Daily Economy, May 18, 2026.

- McLeay, M., Radia, A., and Thomas, R. “Money Creation in the Modern Economy.” Bank of England Quarterly Bulletin, 2014 Q1.

- Federal Reserve Bank of St. Louis (FRED). M2 Money Stock series (M2SL) and M2 Velocity series (M2V).

- U.S. Bureau of Labor Statistics. Consumer Price Index, all-items series, 2009 to 2022.

- Fisher, Irving. “The Debt-Deflation Theory of Great Depressions.” Econometrica, Vol. 1, No. 4 (October 1933).

- Federal Reserve Bank of Cleveland. Median CPI and 16% Trimmed-Mean CPI methodology, ongoing series.

- Mauldin, John. Thoughts From the Front Line, 2026. Summary of Dr. Lacy Hunt presentation on bank lending acceleration and the Fed’s bill-buying program.

- Edwards, Albert. SocGen Global Strategy commentary, 2026. Analysis of T-bill issuance, fiscal dominance, and the “not-QE QE” framework.

- DoubleLine Capital. Commentary on Treasury short-term debt issuance and balance sheet recalibration, 2026.

- Treasury Borrowing Advisory Committee (TBAC). Recommendations on optimal share of bill issuance in total outstanding debt.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice