Mid-Year Themes

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWilliam Tecumseh Sherman, the U.S. Civil War general, once observed: “War is Hell.” War disrupts the lives of the combatants and those in harm’s way, sometimes irreparably.

The economic consequences of war pale in comparison to the human costs, but they can nonetheless be significant. The World Bank estimates that the loss of global output caused by the war in Iran will be more than $1 trillion; Moody’s Analytics estimates that American households have paid war-related costs of more than $100 billion since the beginning of March.

And the meter is still running. Even under the recently-signed truce, supply chains will take a long time to recover. Countries will need to rebuild their energy reserves, at significant expense. Some will search for alternatives to Middle Eastern supply, which will take time and substantial investment. This will have long-term economic consequences for Gulf States.

The war will take a significant toll on national finances, through costs for repair, consumer support, and debt service. This adds to the fiscal stress being experienced by countries such as the United Kingdom. The currencies of some developing nations have come under pressure, creating financial instability; requests for international aid have jumped.

Read more: Global Bond Diversification: Higher Yields and New Opportunities for Alpha

While difficult to account for, uncertainty created by the war has hindered business investment and added a risk premium into markets that raises costs of capital. While the cease-fire lowers the odds of a worst-case scenario, a successful conclusion to negotiations is far from assured.

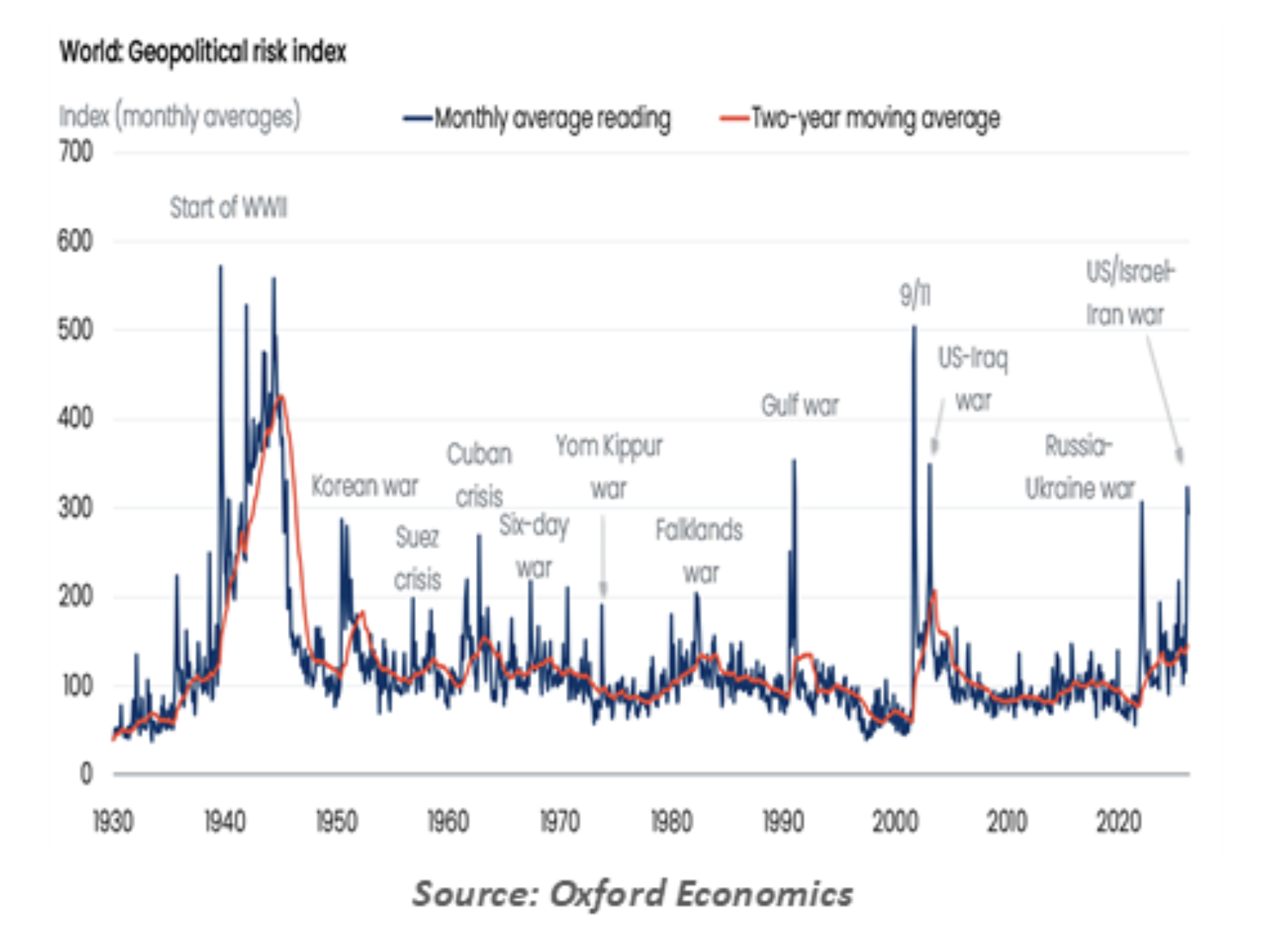

Geopolitical risk is ever-present, but often overlooked. When it manifests, it becomes a dominant driver of economic outcomes. The decline of the global economic order that began in 2008 has been mirrored by a decline in the practice of global diplomacy, leaving the world a more unstable place.

The war in Iran will almost certainly feature prominently in our year-end review this coming December. But we very much hope that we’ll be able to say that the second half of 2026 was far less hellish than the first.

A Measured 180°

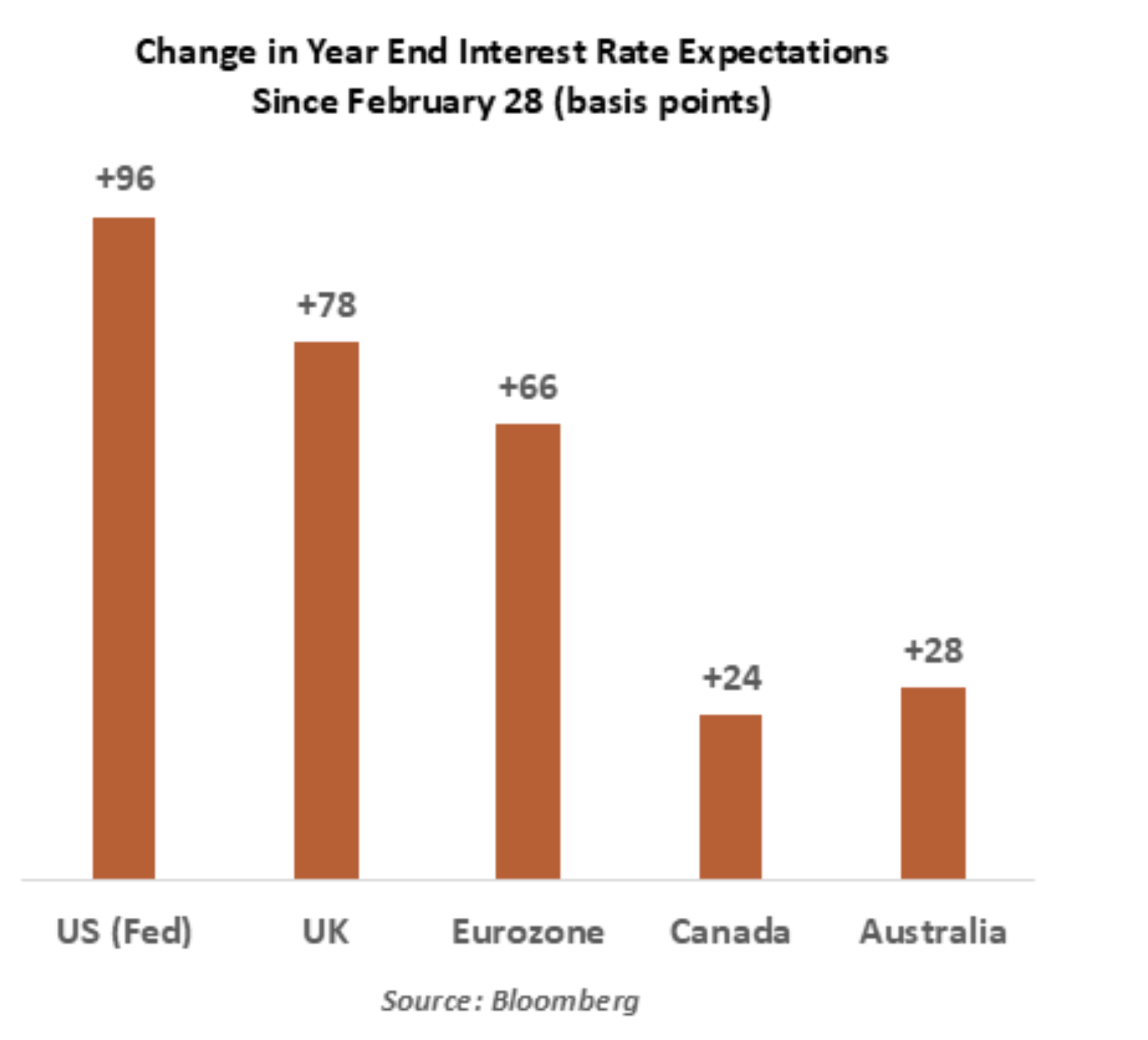

Conventional economic theory suggests that central banks should look past a temporary supply shock. But the largest energy supply shock in history is proving difficult to ignore, forcing global monetary policy into an abrupt about face.

A string of central banks have either raised borrowing costs or signaled their intent to do so if inflation risk remains elevated. The goal is to keep long-term inflation expectations from becoming dislodged.

The timing of dislocations related to the war in Iran is especially uncomfortable. Inflation in major markets like the U.S and the U.K. never fully returned to the 2% mark after the 2021-22 shock. Five consecutive years of above-target inflation have put central bank credibility at risk, raising the cost of inaction.

The policy shift is already visible, and the messaging is converging. The Federal Reserve has signaled possible tightening, while the Bank of England has retained a tightening bias. The European Central Bank (ECB) and the Bank of Japan have already acted, and both continue to keep the door open to further tightening despite the 60-day truce in the Middle East. Some ECB members have cautioned against expecting any meaningful improvement from the peace deal. The Reserve Bank of Australia, which began tightening shortly before the war broke out, has also been compelled to press on.

Markets have executed their own reassessment. At the start of the year, investors were pricing in multiple rate cuts in 2026 across major markets; they are now factoring in rate increases. In some cases, financial conditions have tightened even ahead of concrete policy action.

Underlying this shift is the risk of a more prolonged energy shock. Damage to infrastructure and depleted oil stockpiles mean that normalization could take well into next year.

That said, a repeat of the post-pandemic tightening cycle appears unlikely. Limited evidence of second-round effects, a more benign starting point for inflation in some economies, and less accommodative monetary conditions should cap the scope for further rate increases.

Central banks may have executed a 180° shift, but another abrupt turn toward easier policy looks unlikely anytime soon.

Full Circle

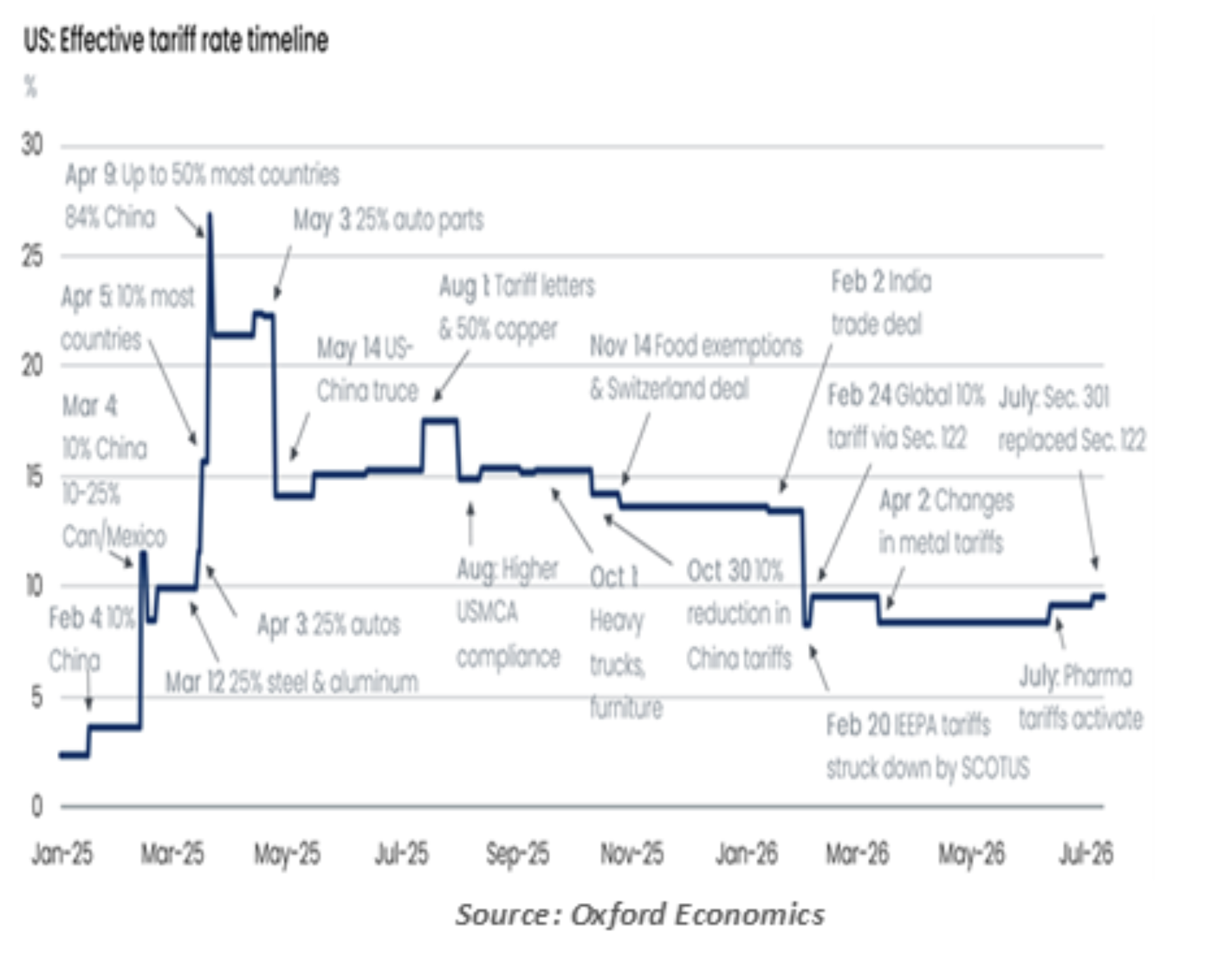

While monetary policy has taken a 180° turn, U.S. trade policy has come full circle.

The shift was triggered by the U.S. Supreme Court’s decision to strike down key tariff measures. For trading partners, this introduced a new layer of uncertainty: concessions negotiated in exchange for tariff relief may no longer hold if the underlying measures are deemed unlawful. For American businesses, the issue has been equally fraught. The ruling complicates pricing and supply decisions already made under a different tariff regime.

The rebuke from the courts did not lead to any form of restraint from the American government. Instead, tariff threats have resurfaced as the administration seeks to preserve negotiating leverage. The message has been clear: even if the 2025 tariffs are unlawful, new tools can be deployed.

The initial response to the court’s action was the use of Section 122 to introduce short-term, broad-based levies. Recognizing their temporary nature, the focus quickly shifted toward more durable mechanisms like Section 301 to justify tariffs on the basis of unfair trade practices. Under this evolving framework, six key trading partners (including Canada, the European Union, and Mexico) are expected to face a 10% baseline rate, while 54 other nations could see slightly higher levies of around 12.5%.

The new system is far from stable. Section 301 tariffs can be stacked and adjusted, with the U.S. trade body gaining the ability to change duties without launching fresh investigations. Add to this the growing likelihood of recurring annual negotiations of the North American trade accord, and the trade policy backdrop begins to look unsettled once again.

Uncertainty will remain embedded in U.S. trade policy, even after the investigations conclude. In that sense, trade policy has come full circle, not to a rules-based steady state, but back to a more transactional world where leverage matters more than rules.

Hemisphere of Influence

When the Americas were first set as destinations for European explorers, the little-known landmass was called the New World. That identity was reinforced as the colonies won their independence from their founding nations. The fifth president of the United States, James Monroe, was the first elected leader to declare that the Western hemisphere should remain its own sphere of influence. That orientation is in renewed vogue as the “Donroe Doctrine.”

The first signals of a stronger hemispheric posture in the second Trump term started with rhetoric like renaming the Gulf of Mexico to Gulf of America and teasing the annexation of Canada (though Canadians did not laugh it off). Pressure around the Panama Canal was consistent with other policies of trade reform. The 2025 U.S. National Security Strategy contained a “Trump Corollary to the Monroe Doctrine,” promising a focus on Western theaters.

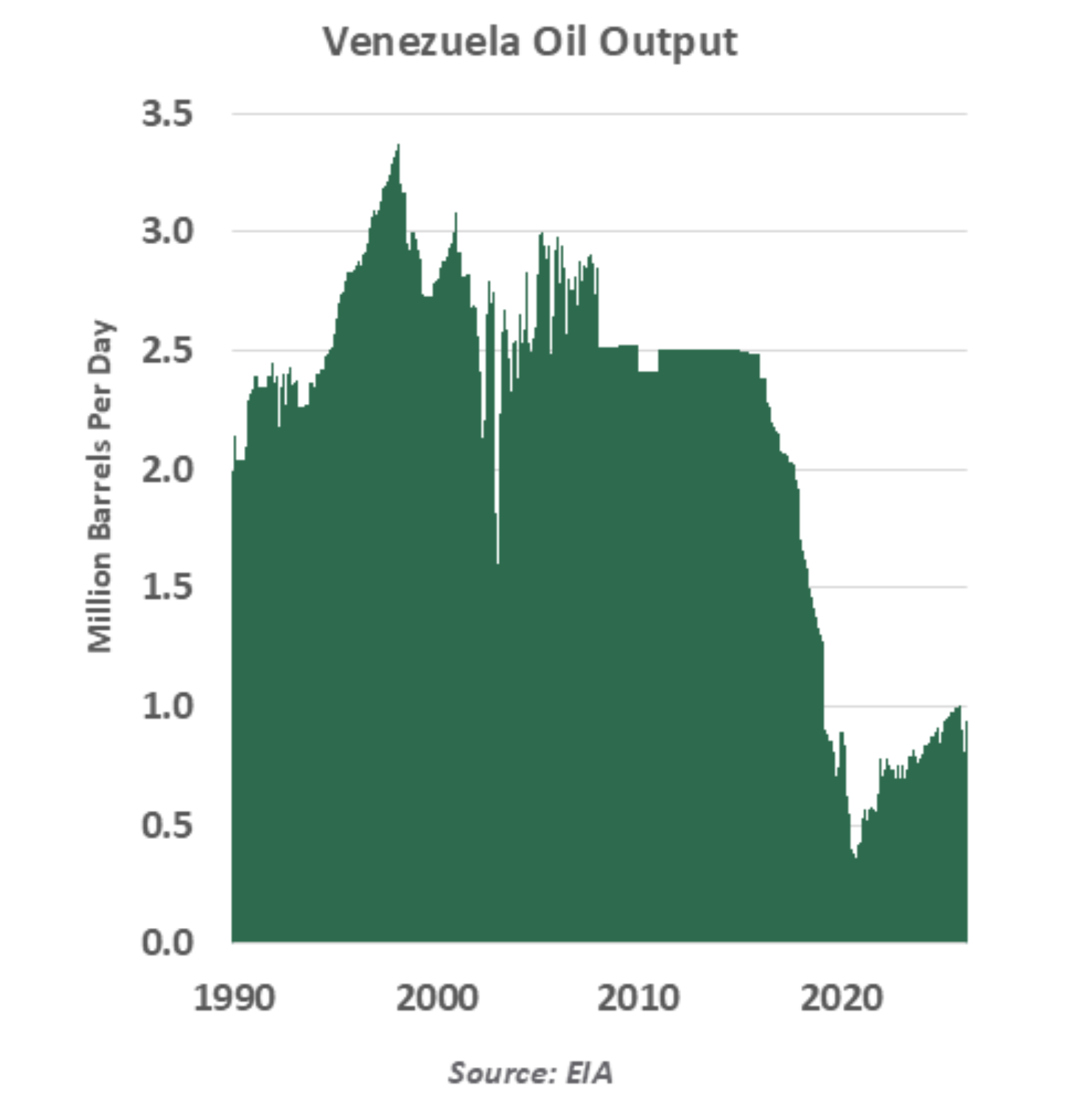

Last year, the U.S. directly attacked private vessels in the Caribbean Sea, alleged to contain narcotics. This year started with the U.S. decapitating Venezuela, installing a friendlier leader with intent to restore its oil sector to its former productivity. Threats to move on Greenland put the NATO alliance in jeopardy. A U.S. blockade on Cuba is causing desperation, likely to reach a climax in the months to come. Along the way, Trump has intervened against Mexican cartels, made overtures to leaders in El Salvador and Ecuador, shown support for former leaders of Brazil and Honduras, offered a fiscal lifeline to Argentina, and warned the president of Colombia about its drug trade.

The western alignment matches other executive decisions: Escalating trade tension with China, distancing from the Russia-Ukraine conflict, and skepticism of NATO among other multilateral institutions. Instead of exerting global influence, the U.S. is aligning itself toward regional supply chains, seeking raw materials closer to home, and reinforcing its regional security perimeter.

The Monroe Doctrine was not always successful, and many past interventions by the U.S. in Latin America were not well received. Time will tell whether the Donroe Doctrine will create a productive a new order for the New World.

Rare Air

It is said that trees don’t grow to the sky. Forces of nature like wind and gravity limit the heights of forests.

This expression has been applied to economic trends, idiomatically suggesting that natural resistance will eventually limit the heights that can be attained. But artificial intelligence (AI) is currently testing the laws of economic gravity.

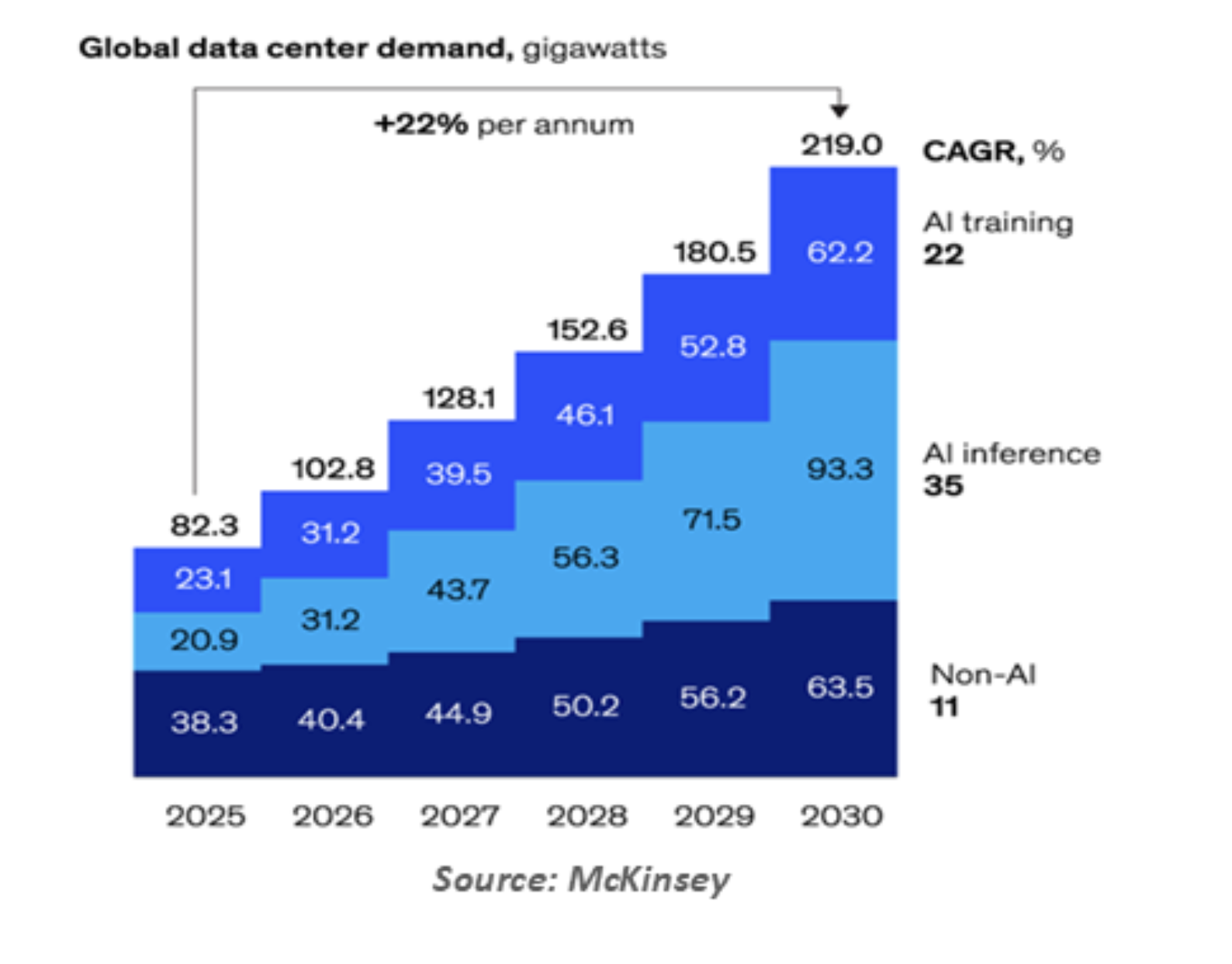

It is difficult to overstate how critical AI has become to global growth. The buildout of infrastructure to support AI processing has been a boon for contractors and the providers of equipment. The skyrocketing prices of leading AI stocks and microchip manufacturers has created immense wealth effects that have supported consumption (albeit in a “K-shaped” fashion). Prospects for productivity gains have given economists hope that another great moderation is at hand.

But a series of forces could limit the ascent of AI. Some come from the natural world: fuel and water needed to operate data centers is in short supply in many areas. Managing the cyber security issues created by AI may require curbs that could slow adoption. And the rise of “AI populism,” born of concerns about labor market impacts and ethical applications, could give rise to policy that impedes progress.

There are many things that distinguish the current interval from the dot-com bubble of the late 1990s, which ended badly. The impressive profitability of leading firms in the AI space is a key differentiator. But the kind of exponential growth which is evidenced in AI-related investment trends may nonetheless be difficult to sustain.

I considered asking Copilot to critique this essay, but I was concerned that it would attempt to suppress any suggestion that AI was less than celestial. Maybe the sky is not the limit this time around. But if the AI boom falls back to earth, the economic consequences will be substantial.

What, Me Worry?

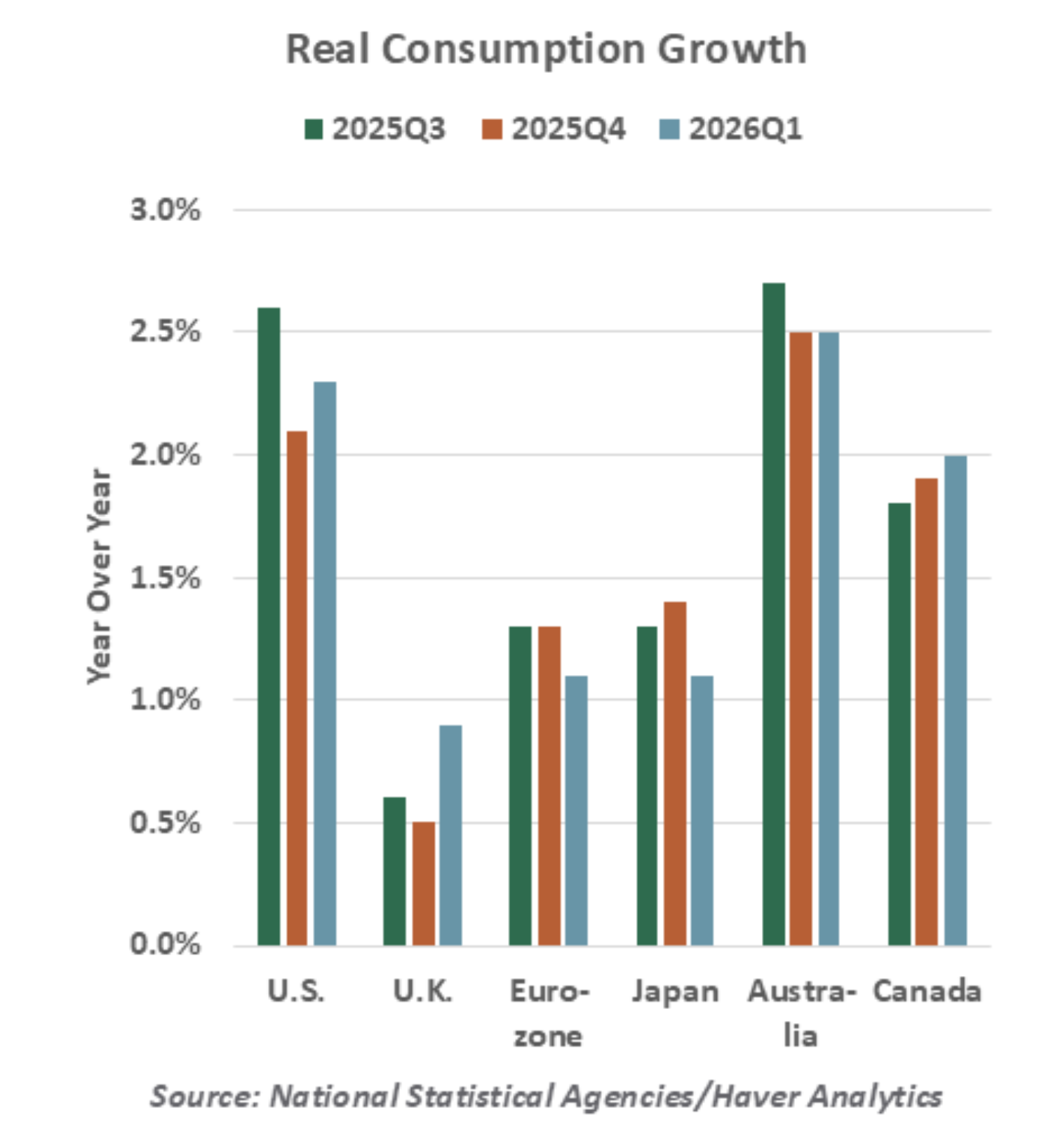

The themes of this issue offer ample reason for caution. The leading news on any given day has often felt disheartening. But scrolling past the troubling headlines reveals a global economy that has again demonstrated its resilience. Our outlook for growth across developed markets is little changed from the start of the year, with favorable data supporting that conclusion.

The primary economic risk to emerge has been inflation, led by motor fuel and airfares. Pass-through to other categories has thus far been limited. We feared that higher energy prices would crowd out other consumer spending, but spending has persisted everywhere we look. In the U.S., core retail sales have grown every month in the year to date; consumers appear to be tapping into savings to deal with the inflationary shock.

Labor markets were the foundation of the post-pandemic “soft landing:” economies avoided recessions because layoffs never took hold. From the start of the year, the unemployment rate is unchanged in the U.S., eurozone and U.K., and two-tenths lower in Japan. Canada and Australia have seen only minor increases in joblessness. Three months of strong payroll gains in the U.S. suggest employers are no longer deterred by uncertainty.

Risk assets have done well in spite of geopolitical uncertainty. Investors have been willing to set the Iran conflict aside as a temporary disruption, not a permanent dislocation. Bond yields have repriced moderately to reflect higher inflation expectations, but credit markets continue to perform well, holding low spreads. Our market-watching partners remain optimistic.

We do not discount the costs of current events. Economies most exposed to the Middle East conflict remain at risk; several Gulf nations are enduring a war-induced recession. Deferred shipments of commodities from the Middle East could have lingering effects for many months ahead. Risks skew toward higher inflation.

Circumstances since 2020 have repeatedly demonstrated how adaptable the economy is in the face of new challenges. We see no reason for that resilience to fade in the balance of the year.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All