83(b) Election for Startup Equity: What Founders Need to Know

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- Deadline: An 83(b) election generally must be filed within 30 days after the property transfer, and there is no standard extension if that window closes.

- Tradeoff: The election can move income recognition to the grant date, but it creates real risk if the stock declines in value or is forfeited before vesting.

- Planning fit: The election is an early structural decision that connects vesting, taxes, liquidity, and long term founder wealth strategy.

Startup equity decisions often happen before a founder has a full advisory team in place. Formation documents get signed, vesting schedules are approved, and the tax consequences may not feel urgent because the company is still young.

However, this is precisely when the 83(b) election for startup equity can matter most. A filing that looks administrative in month one can shape whether future appreciation is taxed as compensation at vesting, or positioned for capital gains treatment after a later sale.

Below, we cover what an 83(b) election does, when the filing deadline applies, and how founders should connect the election to a broader startup equity tax planning strategy, with particular attention to Pennsylvania’s distinct state tax layer.

Read more: Investing is Hard Enough: Here's How to Avoid Obvious Mistakes

What Is an 83(b) Election for Startup Equity?

An 83(b) election is a federal tax election for certain property received in connection with services, most commonly restricted stock or early exercised options that remain subject to vesting. The taxpayer elects to include the spread between fair market value and the amount paid in income at transfer, rather than waiting until the equity vests.

The election is most relevant when property has been transferred before it is fully earned. Three situations usually drive the analysis:

- Restricted stock: Founder shares or early employee shares are actually issued at grant, but the holder can lose them if vesting conditions are not met.

- Early exercised options: The option plan allows exercise before vesting, creating shares that may still be subject to company repurchase or forfeiture.

- Certain LLC interests: Some partnership or LLC profits interests can raise Section 83 questions when ownership is tied to continued service.

Why the 30 Day 83(b) Election Deadline Is Non-Negotiable

The IRS instructions for Form 15620 state that an 83(b) election must be filed no later than 30 days after the property is transferred. Taxpayers may use Form 15620 or a qualifying written statement.

That deadline is tied to the transfer of property, not when the founder sends documents to their CPA. Four process items should be handled when restricted equity is issued:

- Transfer date: Identify the actual transfer date, because that date starts the 30 day clock regardless of when the documents are reviewed.

- Filing method: Confirm the IRS mailing address and current filing requirements with the CPA or attorney before the deadline approaches.

- Proof of filing: Retain mailing evidence, a signed copy, and permanent records, because the election may matter years later during diligence or a sale process.

- Company copy: Provide the completed election to the company or issuer, since IRS instructions require a copy to the service recipient.

Founders often sign equity documents during formation, financing, or onboarding when cap table logistics take priority over tax planning. By the time a wealth advisor or CPA is involved, the 30 day window may already be closed.

And importantly, if the window has already closed there are limited options. There is no IRS mechanism for late filing, and while some attorneys explore cancellation and reissuance strategies, those approaches carry substantial risk and are not reliable remedies.

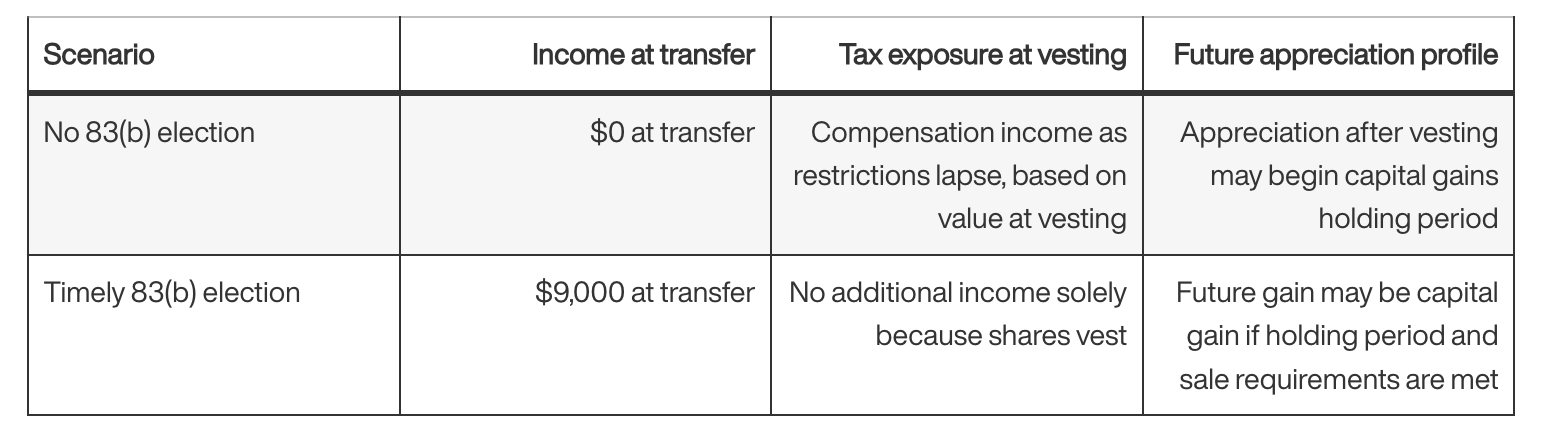

How the Election Changes the Tax Math

Assume a founder receives 1,000,000 restricted shares, pays $0.001 per share, and the shares are worth $0.01 per share at issuance. The company later grows, and each vesting tranche carries a much higher value.

This is the practical appeal of the election. Recognizing income early may be modest compared with recognizing compensation on later vesting tranches at a much higher valuation. The comparison turns on four variables:

- Current value: Lower fair market value at transfer generally makes the election more attractive, assuming the valuation is supportable.

- Amount paid: The taxable amount is fair market value at transfer minus what the founder paid, so a meaningful purchase price at grant reduces upfront income.

- Vesting confidence: The election becomes riskier if the founder may leave, be terminated, or forfeit unvested shares before the schedule completes.

- Liquidity: Even a favorable election can create a cash problem if tax is due before salary, secondary proceeds, or outside assets are available.

When an 83(b) Election May Make Sense, and When It Can Backfire

The election is most compelling when the taxable spread is small, expected appreciation is meaningful, and the founder expects to satisfy the vesting terms. Those facts help, but they do not make the election automatic.

When the Election Fits

Three conditions usually support filing:

- Low current valuation: Shares issued at formation or before major institutional financing may carry a modest fair market value, which limits income recognized upfront.

- High expected appreciation: If the company later closes a priced round or approaches liquidity, the election may help position that growth outside future compensation income treatment.

- Strong vesting probability: The analysis is stronger when the founder expects to remain long enough to satisfy the vesting schedule.

When those three conditions align at formation or in the early stage, the upfront tax cost is often modest and the planning logic is relatively clean. The analysis gets harder as valuation rises and liquidity becomes less certain.

When the Election Can Backfire

The same election becomes costly when those conditions weaken:

- Stock decline: The founder may recognize income early and later own shares worth less than the value reported at transfer.

- Forfeiture: If unvested shares are repurchased or forfeited, tax paid because of the election may not be fully recoverable.

- High upfront value: If the company has already completed several financing rounds, the taxable spread may be too large to justify the upfront cost.

- Cash pressure: A founder may owe tax before any sale, tender offer, or other liquidity event provides cash to pay it.

We evaluate the election alongside the founder’s liquidity position, salary, outside assets, and broader tax picture before recommending it either way.

Restricted Stock, Early Exercise, and RSUs Are Not the Same

Many equity mistakes start with vocabulary. Restricted stock, options, and RSUs have very different tax treatment.

The distinction usually looks like this:

- Restricted stock: Actual shares are issued now, subject to vesting or forfeiture, which is the classic 83(b) election context.

- Early exercise options: An 83(b) election may become relevant after early exercise creates shares that remain subject to vesting or company repurchase.

- Standard RSUs: Traditional RSUs generally do not involve the same immediate property transfer at grant, so an 83(b) election typically does not apply.

This is one reason we often connect 83(b) discussions with broader equity compensation tax planning. The election is only useful when the equity instrument actually fits the rule.

Pennsylvania Founders Have a State Tax Layer

Pennsylvania founders should not treat the 83(b) election as a federal only issue. The Pennsylvania Department of Revenue states that a federal Section 83(b) election is deemed an election for PA personal income tax purposes, that no separate Pennsylvania filing is required, and that a separate Pennsylvania election is not permitted if no federal election is made.

A Pittsburgh founder who files federally is also making the Pennsylvania personal income tax election. Pennsylvania uses a flat 3.07 percent personal income tax rate, which makes the state analysis different from states with progressive brackets.

Pennsylvania’s nonconformity with federal QSBS treatment is separate but related, so federal exclusion planning and PA tax modeling should be reviewed together.

How an 83(b) Election Fits Into Founder Wealth Planning

The 83(b) election is one early structural decision inside a larger founder wealth plan. Those same shares may later drive liquidity planning, estate planning, charitable strategy, and QSBS analysis.

Later planning should revisit four areas:

- Liquidity event planning: Before a sale, IPO, tender offer, or secondary transaction, confirm tax basis, holding period, vesting history, and proof of timely filing.

- Estate and trust planning: Founder stock can become an estate planning asset before liquidity, but transfers are affected by approval rights, valuation, and vesting terms.

- QSBS review: Section 83(b) and QSBS are separate rules, but both matter when original issuance, holding period, entity structure, and trust ownership are reviewed before a sale. See our guide to QSBS stacking for founders.

- Investment transition: After liquidity, planning shifts from concentrated company risk to tax aware diversification, cash reserves, charitable funding, and long term portfolio construction.

Final Takeaway

An 83(b) election is a short filing with consequences that extend across years of planning. The form itself is not complicated, but making the decision on the right timeline, for the right type of equity, at a point where the tradeoffs actually favor filing, is harder than it looks.

The election is one piece of a founder wealth plan that also needs to address vesting risk, liquidity timing, state tax treatment, and potential QSBS eligibility. Treating it as a standalone checkbox rather than a coordinated planning decision is where most avoidable mistakes originate.

For Pennsylvania founders, early coordination among a CPA, startup attorney, and wealth advisor can help ensure the election fits the broader plan. For more on pre liquidity founder planning, see our guides on QSBS for founders and the tax implications of selling a business in Pennsylvania.

Frequently Asked Questions

What is an 83(b) election for startup equity?

An 83(b) election allows a taxpayer who receives substantially nonvested property for services to recognize income at transfer instead of waiting until vesting. For startup equity, this most often applies to restricted stock or early exercised options where shares are issued before they are fully vested.

When do you have to file an 83(b) election?

An 83(b) election generally must be filed with the IRS no later than 30 days after the property is transferred. The transfer date, not the tax filing deadline, controls the timing. Founders should confirm the deadline immediately when equity documents are signed.

Does an 83(b) election apply to RSUs?

An 83(b) election generally does not apply to standard RSUs because RSUs typically do not involve an immediate transfer of property at grant. The election is more commonly relevant for restricted stock or early exercised options where actual shares are issued before vesting is complete.

Can an 83(b) election save taxes for founders?

An 83(b) election can reduce future tax exposure when the stock has a low value at transfer and later appreciates significantly. It does not eliminate tax. It changes when income is recognized and may help position later appreciation for capital gains treatment if other requirements are satisfied.

How does Pennsylvania treat an 83(b) election?

Pennsylvania generally treats a federal 83(b) election as the Pennsylvania personal income tax election. No separate Pennsylvania filing is required, and a separate Pennsylvania election is not permitted if no federal election is made. Pennsylvania founders should coordinate the federal filing with state tax reporting.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits