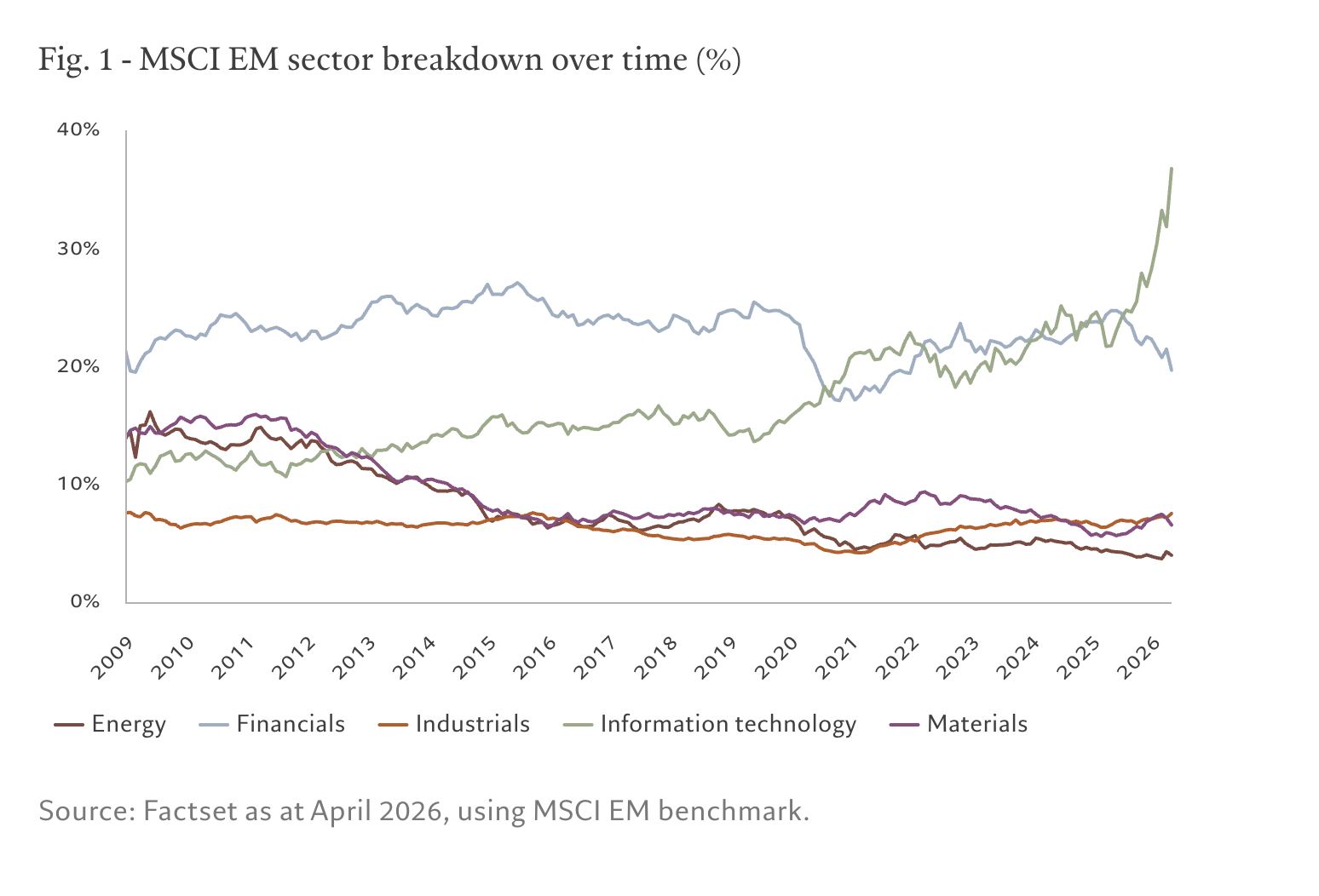

At first glance, allocating to emerging markets appears to add diversification to a portfolio. Look more closely, and the reality is more nuanced. In the late 1990s, the MSCI EM index was dominated by materials and telecoms, driven by the growth of mobile telephony and the internet bubble. Then, at the nadir of the global financial crisis in 2008, materials and energy together accounted for more than a quarter of the index. China's infrastructure-led growth drove metals and energy prices higher and rewarding the countries that supplied them for the following couple of years.

Today, this composition has shifted again. Technology now dominates the index, representing more than a third of the benchmark, compared with just 10% in 2008.

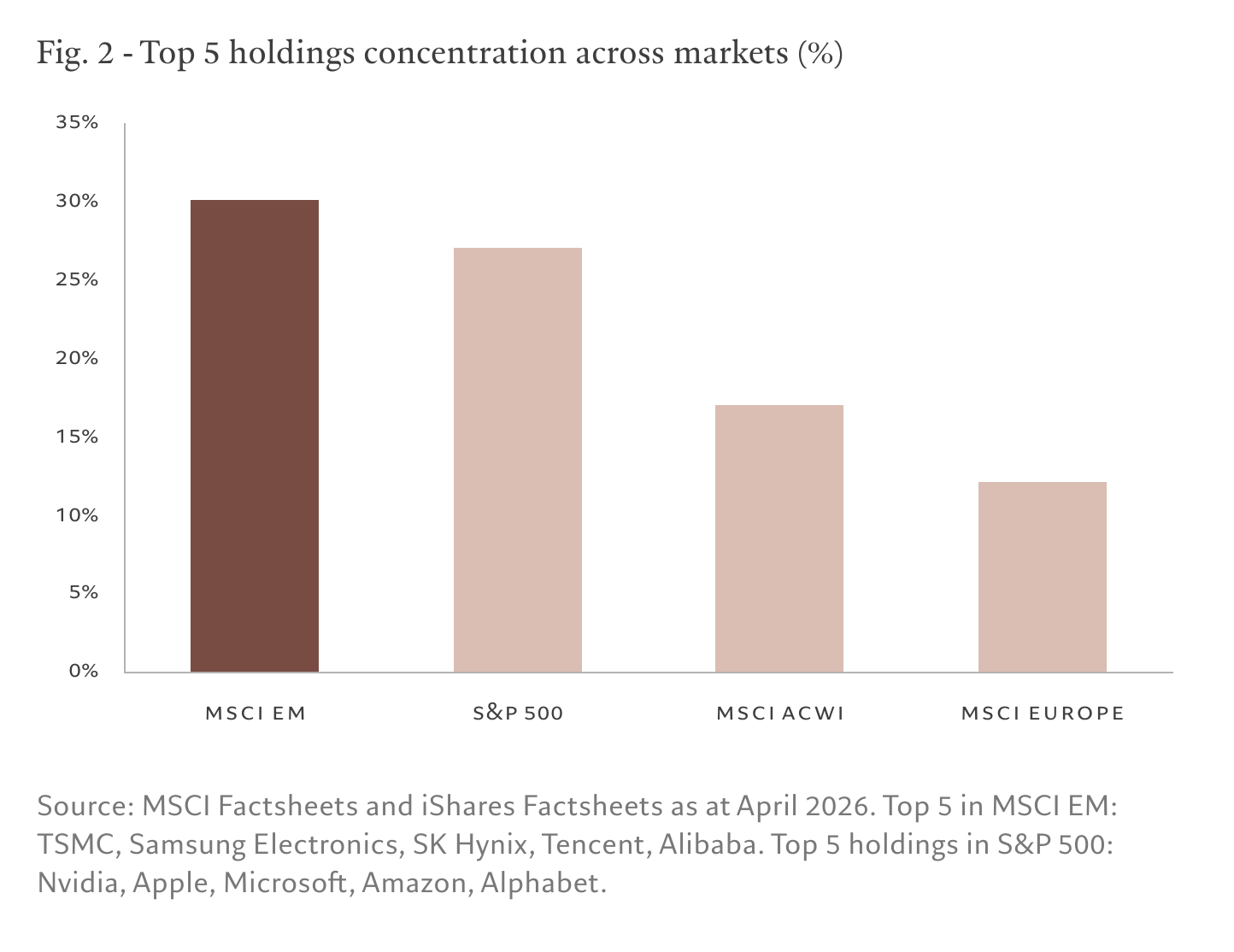

This concentration is even more pronounced at a stock level. The top ten holdings – mostly in technology – represent almost 40% of the index, up from 21% in 2008, with Taiwan’s TSMC alone accounting for some 14%. A group of five influential stocks– TSMC, Samsung Electronics, SK Hynix, Tencent and Petrobras – drives roughly half of all earnings growth across the index. This is more concentrated than in the US, where a similar portion of earnings growth is generated by the Magnificent Seven1 of big tech stocks.

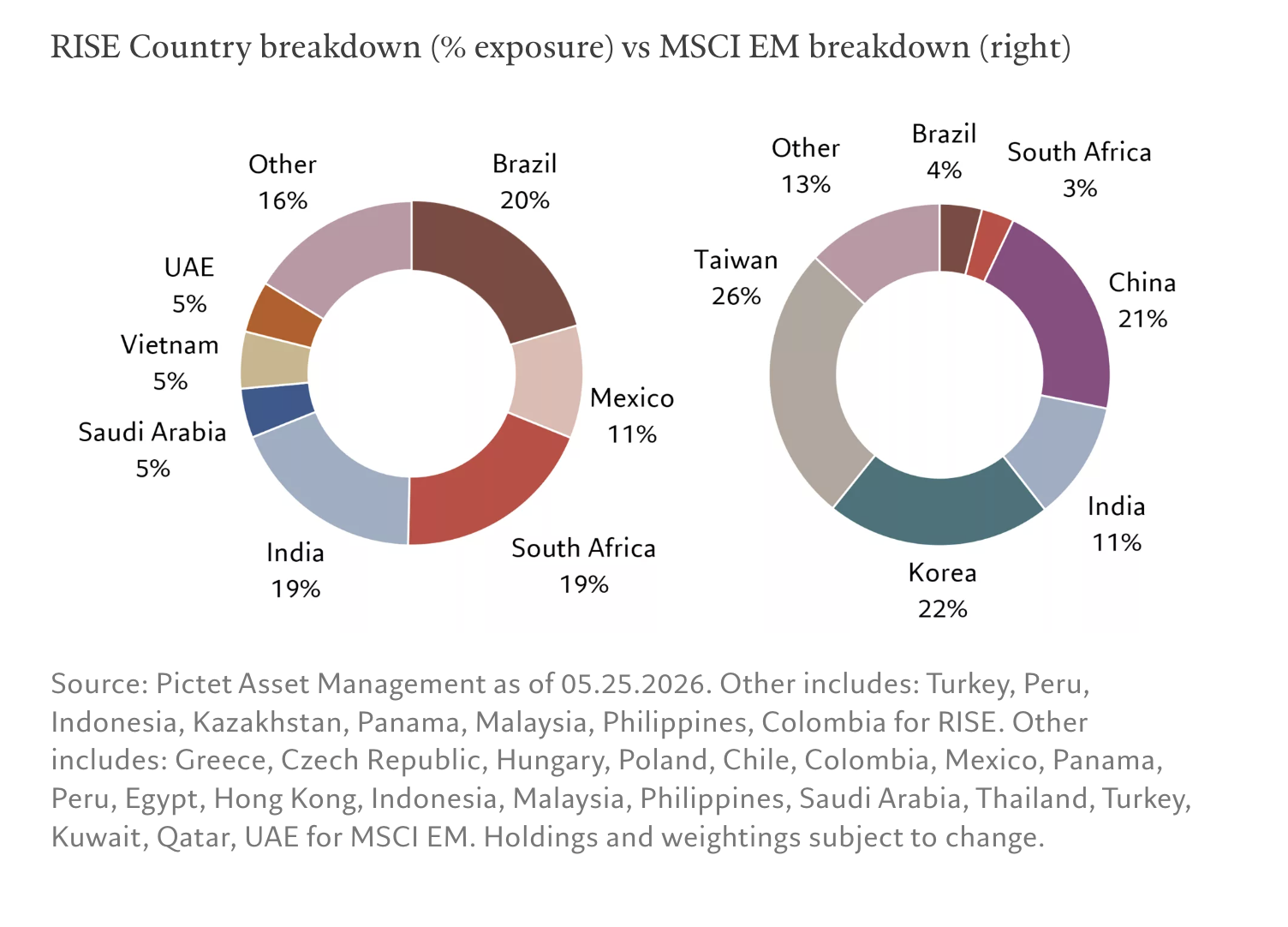

The shift in country weights tells a similar story. China, Korea and Taiwan together account for nearly two thirds of the MSCI EM index and a disproportionate share of index risk, particularly through technology and hardware exposure.

For investors already holding global or developed equities, this creates an unintended overlap with tech-heavy parts of the equity market, limiting the true diversification benefits of EM allocations.

Diversification is not defined by how many countries or stocks you hold, but by the independence of return drivers. Today, as those drivers become more aligned than many investors realise, the label on the tin no longer matches the contents.

This is particularly relevant for US investors with significant exposure to large-cap growth, where positioning has become structurally crowded. In such cases, adding conventional emerging markets exposure can reinforce existing positioning rather than diversify it.

Read more: Straitening Out

Rethinking emerging markets exposure

Emerging markets remain a structurally attractive investment universe. EM earnings grew 25% year-on-year in early 2026, the fastest pace since the post-Covid rebound.

The question should no longer be whether to invest in emerging markets, but how.

In practice, this means looking beyond the dominant North Asian markets to access a broader range of investment opportunities where returns are driven more by domestic expansion than by global technology cycles.

India and Brazil demonstrate this clearly. Growth in these markets is supported by domestic factors: expanding middle classes is boosting demand for housing, consumer goods and digital payments, while a rapid build-out of roads, rail and logistics is improving the movement of people and goods. Demographics are central to this: countries with growing working-age populations tend to deliver stronger economic growth, which over time has translated into more resilient and differentiated sources of equity returns.

This is the thinking behind RISE (Pictet Emerging Markets Rising Economies ETF). By deliberately stepping away from the parts of the index most heavily dominated by semiconductor and export-driven technology exposure, specifically China, Korea and Taiwan, the strategy focuses instead on economies where returns are driven by domestic demand and earlier-stage financial development.

The constraint that is breaking

The result is a portfolio that stands apart through:

- Focusing on markets where growth is driven by domestic demand and structural growth trends, including positive demographic trends, rising consumption and infrastructure investment

- Reducing exposure on a handful of dominant technology companies, lowering concentration risk

- Accessing value outside the most crowded and expensive areas of the emerging markets universe, including select frontier markets.

Positioning for tomorrow's opportunities

Diversification is not static. It evolves as markets change, sometimes in ways that are not immediately visible, as the history of the MSCI EM index clearly shows.

Today, a mainstream EM allocation delivers unexpectedly large exposure to the AI infrastructure cycle via Asian semiconductors. For investors already exposed to global growth equities, this may represent an unintended concentration.

Used alongside a core EM allocation, a strategy like RISE can help broaden the range of return drivers within a portfolio, supporting more resilient growth and comprehensive diversification.

Fund holdings are subject to change. The latest top 10 holdings of the RISE ETF are accessible here: etf.am.pictet.com/rise/

1. The Magnificent Seven (‘mag7”) in this context means the seven biggest, most influential US tech stocks: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla. This is a group of giant companies that have had an outsized impact on the stock market in recent years. These companies are often talked about together because they are large, fast-growing, and heavily shape major stock indexes like the S&P 500

Important information

Regulatory Statement: Before investing, carefully consider the fund’s investment objectives, risks, charges, and expenses. This and other information can be found in the fund’s prospectus or, if available, the summary prospectus, which may be obtained by calling (855) 994-4778 or visiting www.pictet.com/etf. Read it carefully before investing.

Investment Risks: Investing in Exchange Traded Funds (ETFs) involves risk, including possible loss of principal. ETF shares are bought and sold at market price, not net asset value (NAV), and are not individually redeemed from the fund. Market price returns may be calculated using the midpoint between the bid and ask prices.

Performance Disclosure: Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance data may be obtained by visiting www.pictet.com/etf.

Tax Considerations: ETF distributions may be taxable as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account.

Market Volatility: ETF shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

Non-FDIC Insured: ETF investments are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. They may lose value.

Professional Advice: The information provided on this website is for general informational purposes only and should not be considered as investment advice. Consult with a financial advisor or professional before making any investment decisions.

Performance: Market price returns are determined using the official closing price of the fund’s shares and do not represent the returns you would receive if you traded shares at other times.

Pictet Asset Management exchange-traded funds (ETFs) are actively managed and do not seek to replicate a specific index. ETF shares are bought and sold through an exchange at the then current market price, not net asset value (NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV when traded on an exchange. Brokerage commissions will reduce returns. There can be no guarantee that an active market for ETFs will develop or be maintained, or that the ETF’s listing will continue or remain unchanged.

By using this website, you acknowledge that you have read and understood this disclaimer and agree to be bound by its terms.

Foreside Fund Services, LLC, Distributor.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Pictet Asset Management

More Insurance & Annuities Topics >