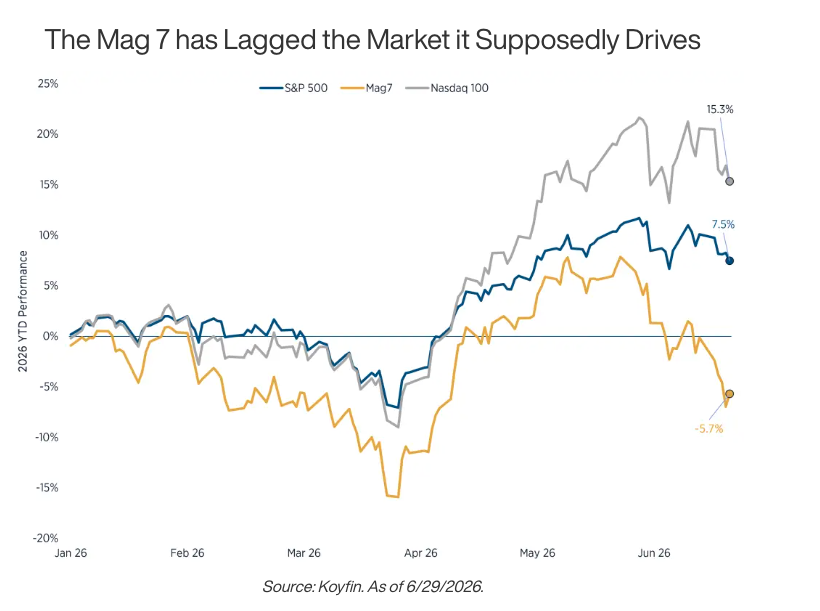

The Mag 7 has been the single largest driver of the stock market’s performance three straight years, accounting for over 20% of the S&P 500’s performance. However, there is a performance divergence happening in 2026 as the S&P 500 continues to go up, while the Mag7 go down.

Through late June, the Magnificent Seven stocks are down roughly 1% as a basket while the S&P 500 has returned over 7%. So the group, that many analysts said was a risk to the market’s long-term upside, is now the one visibly trailing it. And more importantly, the market is still going higher.

This divergence is not a short-term distortion. Instead, it’s a signal that:

- There is a new leadership forming in the broader market (more on this below)

- The market’s reliance on the Mag7 is not as significant as feared, and

- There is widening breadth in the S&P 500

At the beginning of 2026 we said “Returns must be Earned” (2026 Outlook Interview with FintechTV – Returns Must be Earned) this year. So far, that’s not happening with the Mag7. While the group’s earnings growth is still positive in 2026, it is decelerating, running at a pace barely ahead of the other 493 companies in the index, and the market is pricing the deceleration, not the level.

Below, we cover why the group has fractured along fundamental lines, where the 2026 rotation actually came from, and what both developments mean for portfolios built on the assumption that the same names keep working.

The Magnificent Seven Stopped Moving Like a Group

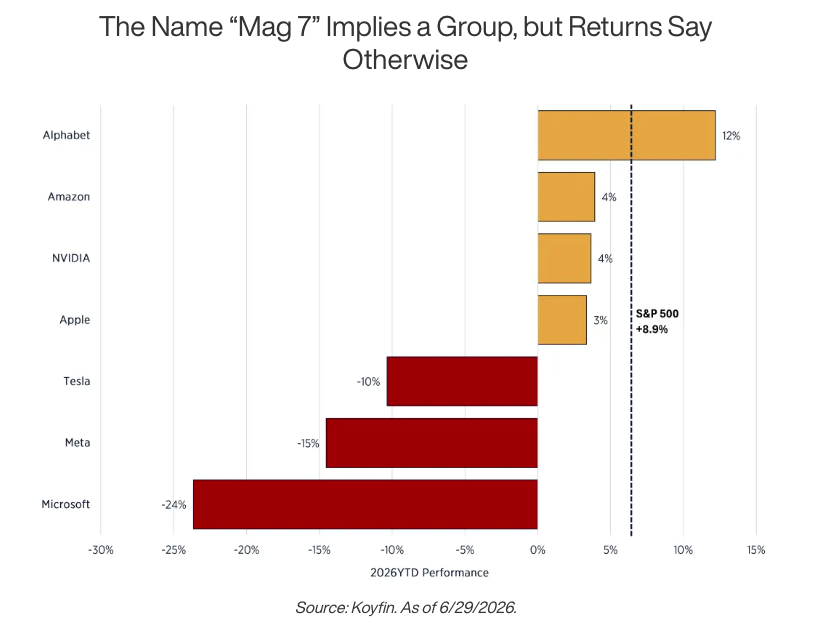

“Magnificent Seven” implies a unified trade. The 2026 return data says otherwise, and the dispersion inside the basket is wider than most investors realize.

Two names have meaningfully outperformed:

- Alphabet is up roughly 12%, rewarded for stronger-than-expected Gemini traction and growing investor conviction that its custom TPU infrastructure is a credible alternative to Nvidia’s ecosystem, not just an internal project.

Both are above the S&P 500 benchmark return of 7%. The rest of the group is not:

- Nvidia is up roughly 4% year to date, still the most important hardware company in the AI buildout, with demand for its chips showing no visible sign of softening.

- Amazon is up roughly 4%

- Apple is up roughly 3%

The three laggards are where the story gets notable:

- Microsoft is down roughly 24%, a significant drawdown driven by investor concern that Azure and Copilot capital expenditure has been large and sustained without converting to revenue growth fast enough to justify the pace.

- Meta is down roughly 15%, having fallen sharply after guiding capital expenditures even higher than its already aggressive 2025 budget

- Tesla is down roughly 10% as a lack of credible growth narrative is weighing on investors.

The dispersion inside the Magnificent Seven is now larger than the dispersion between the basket and the rest of the market.

And importantly, the market is differentiating between AI spenders with a visible payoff, and AI spenders still asking investors to take the return on faith.

What’s Driving 2026’s Market Leadership

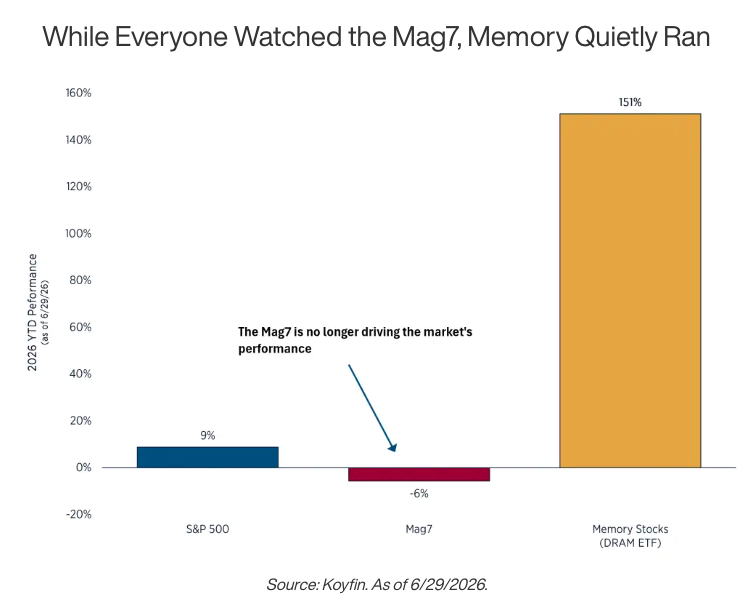

While the debate over the Magnificent Seven’s direction dominated financial media, the year’s most significant rotation happened in a corner of the market most equity investors do not follow closely: memory chips.

The mechanics are simpler than they sound. The same three companies that make the memory in your laptop and phone (Samsung, SK Hynix, and Micron) also make the specialized memory that AI data centers run on, and when AI demand surged, they shifted their factories toward the higher-margin AI product.

Less memory for consumer devices meant a sudden supply shortage that sent prices up 80 to 90% in a single quarter, with data centers now consuming an estimated 70% of global memory production, up from roughly a quarter just a few years ago.

The year-to-date results make the contrast difficult to ignore:

- Roundhill Memory ETF (DRAM): up over 125% since its April 2026 launch through late June, making it among the most successful thematic ETF debuts in recent memory

- Micron Technology (MU): up nearly 300% year to date, as the only U.S.-based DRAM producer in a market otherwise dominated by Samsung and SK Hynix, with record Q3 FY2026 results showing the pricing environment in full effect

- Magnificent Seven basket: down roughly 1% over the same period, essentially flat across a group that attracted the majority of investor attention

Bottom line: The AI trade did not “stall”, it simply shifted to rewarding the picks-and-shovels companies that are already generating positive returns from AI vs. the companies projecting them.

This Kind of Rotation Is Not Unusual. What Is Unusual Is How Few Were Watching.

Leadership rotates in markets constantly, quietly, and almost always without a clean announcement. Energy led in 2022 while growth stocks fell apart. Regional banks and money center banks have repeatedly traded leadership and given it back over the same cycle (See our 1Q26 Commentary for more about market rotations). Value and growth have swapped the baton for a decade, each time looking permanent right before it reversed.

The Mag 7 narrative became so dominant for so long that it started functioning less like an investment thesis and more like a default assumption. The implicit belief embedded in most portfolios was that these seven names carried the index because they deserved to, and that the fundamental case for each one was roughly equivalent to the case for all of them. Neither assumption was ever precisely true, and 2026 has made both of them harder to defend.

Labels like “Mag 7” and “the AI trade” offer the comforting illusion that there is one trade to own and everything else is noise. There is not. There is only where capital is flowing this quarter, and that shifts more frequently, and more quietly, than headlines tend to suggest.

What This Means for How We Think About Positioning

This is not an argument for rotating aggressively into memory stocks at their current prices. DRAM’s move has been violent, and the memory sector has a long and well-documented history of brutal boom-bust cycles once new supply catches up with demand. Chasing a trade that has already returned more than 100% is its own category of mistake, and new fab capacity coming online in 2027 and 2028 should eventually change the supply picture.

The takeaway is that portfolios need to be built to handle rotations that do not announce themselves in advance. Specifically, a portfolio needs enough flexibility to lean toward where genuine strength is actually showing up, rather than staying anchored to a basket that earned its reputation in a prior cycle. That requires a real willingness to reduce exposure where the fundamental case has deteriorated, even when the tickers are familiar and the consensus still believes in them. At the same time, guardrails matter, because rotations rarely resolve cleanly on the first move, and a portfolio that chases every shift without discipline can do as much damage as one that refuses to adjust at all.

If you would like to discuss your wealth and investment strategy with us please reach out today.

Please read important post disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

More Active Management Topics >