Editor’s note: we’re publishing an early, abbreviated issue in advance of the U.S. holiday weekend. For those commemorating America’s 250th, we hope you enjoy the occasion.

Former Fed Chair Alan Greenspan’s passing has brought a stream of retrospectives on his approaches to managing the economy. He erred on the side of parsimony, favoring short public statements. Greenspan’s vague communication style offered little clarity over the future path of interest rates. Observers would guess the outcome of policy meetings by the heft of his briefcase.

Scrutiny of the Fed’s communications was not unique to Greenspan’s tenure. Outside of crisis intervals, the Fed has a narrow tool kit. The Federal Open Market Committee (FOMC) sets the overnight Fed Funds Rate and a handful of other benchmark rates that move in tandem, and it can adjust its bond portfolio holdings. But the Fed can amplify its influence by talking.

The Fed’s communications about the potential future path of monetary policy are known as forward guidance. This broad term encompasses any message, from any official, with any hint as to the direction of interest rates, even minor details like choices of adjectives to describe conditions. The use of forward guidance is now under review.

Read more: The Federal Reserve’s New Leader Lays Out His Agenda

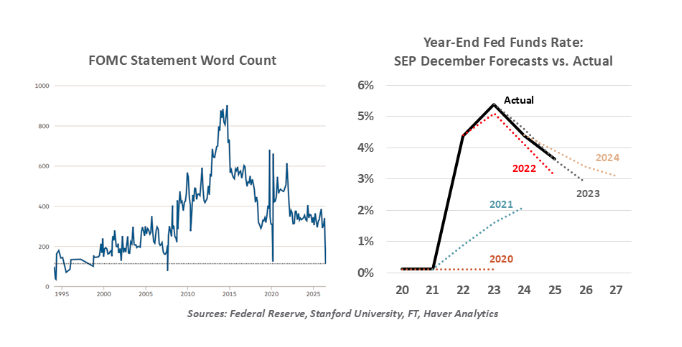

By law, the Fed’s only mandatory communication is for the Chair to give testimony to Congress twice per year. Beyond that, the FOMC has wide discretion. The first FOMC post-meeting statement was issued only in 1994, when the Fed changed rates; even Greenspan saw some value in being clear with markets. Starting in 1999, statements followed every meeting, regardless of the decision.

The quarterly Summary of Economic Projections (SEP) debuted in 2007. Quarterly press conferences started in 2011; former Chair Jerome Powell shifted to a cadence of press conferences after every meeting in 2019, stating a goal to “improve communications.”

Change is coming, however. New Fed Chair Kevin Warsh stated at his confirmation hearing: “I don’t believe in forward guidance.” Committing to a future path can make the FOMC too late to change course when necessary, a criticism levied against his predecessor’s tenure. True to his word, Warsh declined to contribute to the SEP in his first meeting, and he cut the statement’s length by more than half to remove all hints of a future outlook.

Warsh added that the FOMC felt that forward guidance “was not well suited to the current policy conjuncture.” This concern was not new to Warsh’s tenure: Three voting members dissented from the prior meeting’s decision, objecting to the statement’s forward guidance. Recent experience gives the committee good reason to be cautious. The last time inflation exceeded 4%, the Fed’s projections expected it to recede in an orderly manner, and their projected rate path widely underestimated what actually occurred.

We would certainly agree that uncertainty complicates forecasting. But the Fed’s projections don’t need to prove correct in order to be useful. The range of FOMC expectations offers a service by illustrating the range of potential outcomes, and how the Fed will react to them. Since interest rate changes work with a lag, having a sense of how conditions will evolve in the coming quarters is essential to making monetary policy decisions today.

Asked how markets might respond to less guidance from the Fed, Warsh argued that financial markets should respond to new information directly, not colored by expectations of the Fed’s reactions. But asset valuations will remain sensitive to interest rates, and best guesses of the Fed’s next moves will still be a factor in market pricing. Less guidance from the Fed could make valuations more volatile.

The specifics of “regime change” at the Fed are still coming together, but a few themes are clear. The Fed will abide by its 2% inflation target, and it will provide less forward guidance. With the personal consumption expenditure price index exceeding an annualized rate of 4%, rate hikes are expected in the market for interest rate futures. Warsh could have offered guidance that inflation was likely to settle and rate hikes could be avoided. He chose not to.

Asked about his plans for future press conferences, Warsh was noncommittal, opining that they should be held “when you have something useful to say.” Already, speeches from other FOMC members are occurring at a slower pace than typical. Markets will need to adapt to a Fed that communicates less. If Warsh’s goal is to move back toward older communication conventions, we would suggest he consider carrying a briefcase.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

More Tax Loss Harvesting Topics >