Key Takeaways

- Although the June’s jobs report revealed some moderation in new hiring, it reinforced the view that the labor market is still a positive contributor and closed the curtain on rate cuts

- With inflation still above target, the money and bond markets have clearly shifted monetary policy expectations for Fed rate hikes later this year.

- In this environment, a barbell strategy combining zero- or ultra-short-duration exposures with core bonds remains a disciplined approach to balancing income opportunities with interest rate risk.

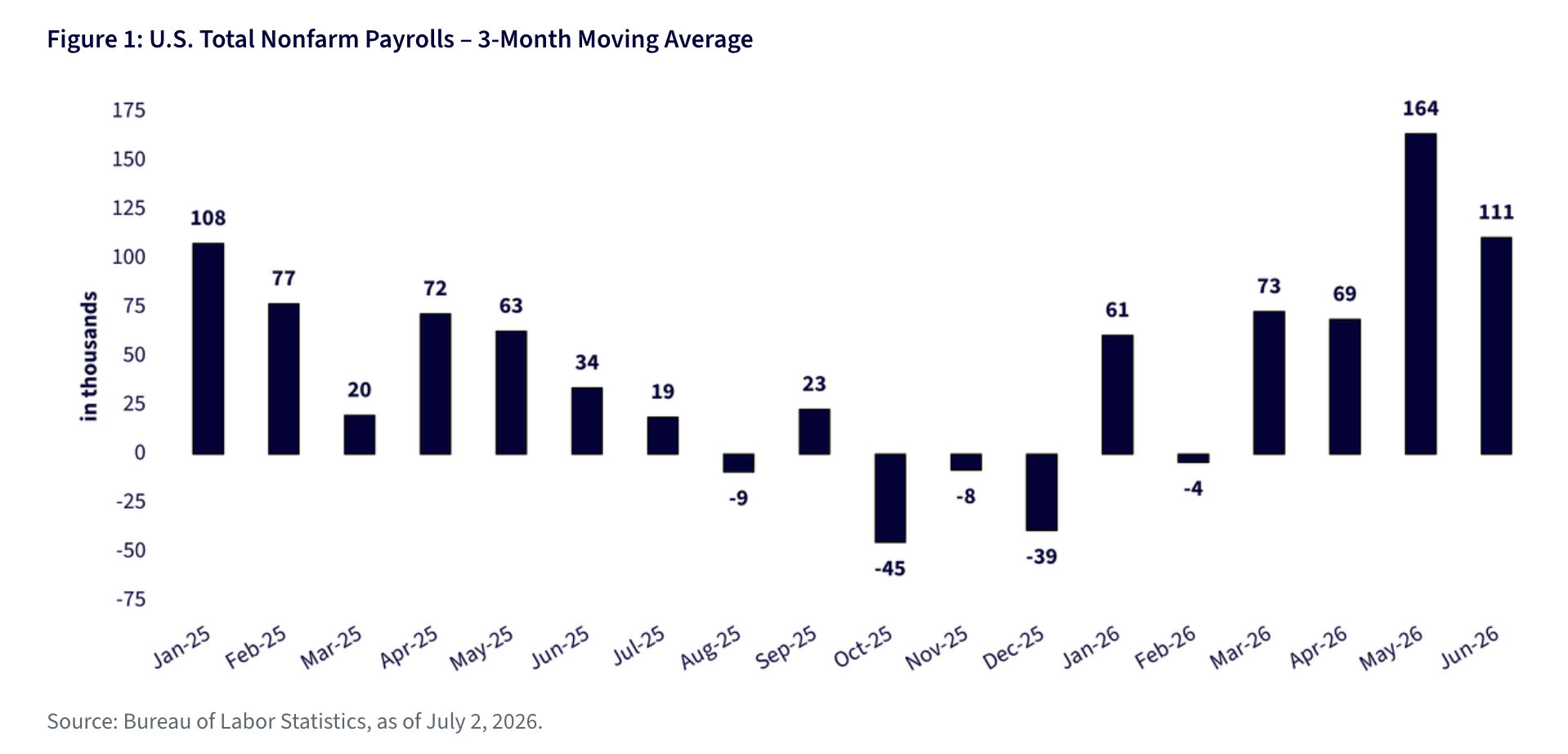

The June jobs report underscored our thesis that while the labor market remains in the 'economic plus column,' some of the prior months' increases in new hiring seemed a bit too high. Right on cue, the Bureau of Labor Statistics (BLS) reported that total nonfarm payrolls rose less than expected and that the prior two months’ gains were revised downward (see Figure 1). Moderate real gross domestic product growth, above Fed-target inflation and Warsh & Co. on hold are our primary themes for the second half of 2026 and this employment report plays right into those scenarios. Here are some key takeaways:

- Total nonfarm payrolls rose +57,000 or only about half of the consensus estimate while the prior two months’ gains were revised downward by -74,000. That places the ‘new’ 3-month moving average tally at +111,000, a bit more in line with what we expect going forward.

- The unemployment rate dropped -0.1 percentage point to 4.2% but this decrease contained a lot of noise—the civilian labor force, employment and unemployment readings all declined in a visible fashion

- This jobs report is not a gamechanger for Treasury yields and supports our Treasury 10-year yield call of maintaining a 4.00%–4.50% range, with the potential for occasional ‘overshoots’. The U.S. Treasury 2-year yield is still pricing in at least one rate hike

-

The U.S. Treasury 2-year/10-year yield curve steepened by +10 basis points post-jobs

See more: Mid-Year Update