"Water, water, everywhere, nor any drop to drink."

— Samuel Taylor Coleridge, The Rime of the Ancient Mariner

Last week's issue generated more thoughtful replies than we expected. What struck me wasn't that some of you disagreed with a point or two. It was what you agreed on. Almost nobody argued that nothing had changed. The debate was over why.

Some pointed to offshoring. Others pointed to automation, regulation, financialization, and the Fed. A few argued the productivity-wage gap itself is measured wrong. All of it deserves a fair hearing, and we'll spend the next few weeks giving it one.

But before we can discuss potential solutions, such as bringing production back, rebuilding supply chains, even rolling back regulation, we have to talk about the one thing all have in common. Each of these ideas depends on enormous amounts of reliable, affordable energy.

Something Doesn't Add Up

Does it feel like we live in the world's largest energy producing nation? I'd guess not. It feels more like a country where electricity keeps getting more expensive, where utilities warn about shortages, and where large employers can't get enough power to expand.

To me, it's strange. Strange because America is the world's largest producer of oil. It's the world's largest producer of natural gas, by a wide margin, and sits on some of the largest coal reserves on earth. In parts of the Permian Basin, natural gas can trade below zero. There's more of it than the pipelines can carry, and producers are paying companies to take it away.

A country drowning in energy shouldn't also feel like it's running out of electricity. In other words: before we ask whether America can make more things again, we should probably ask whether America can power the production.

We Have the Fuel

For two decades, governments and corporations promised a shift away from oil, coal, and gas toward renewables, the "energy transition." However, fossil fuels still supply somewhere in the high 80% range of global primary energy consumption.

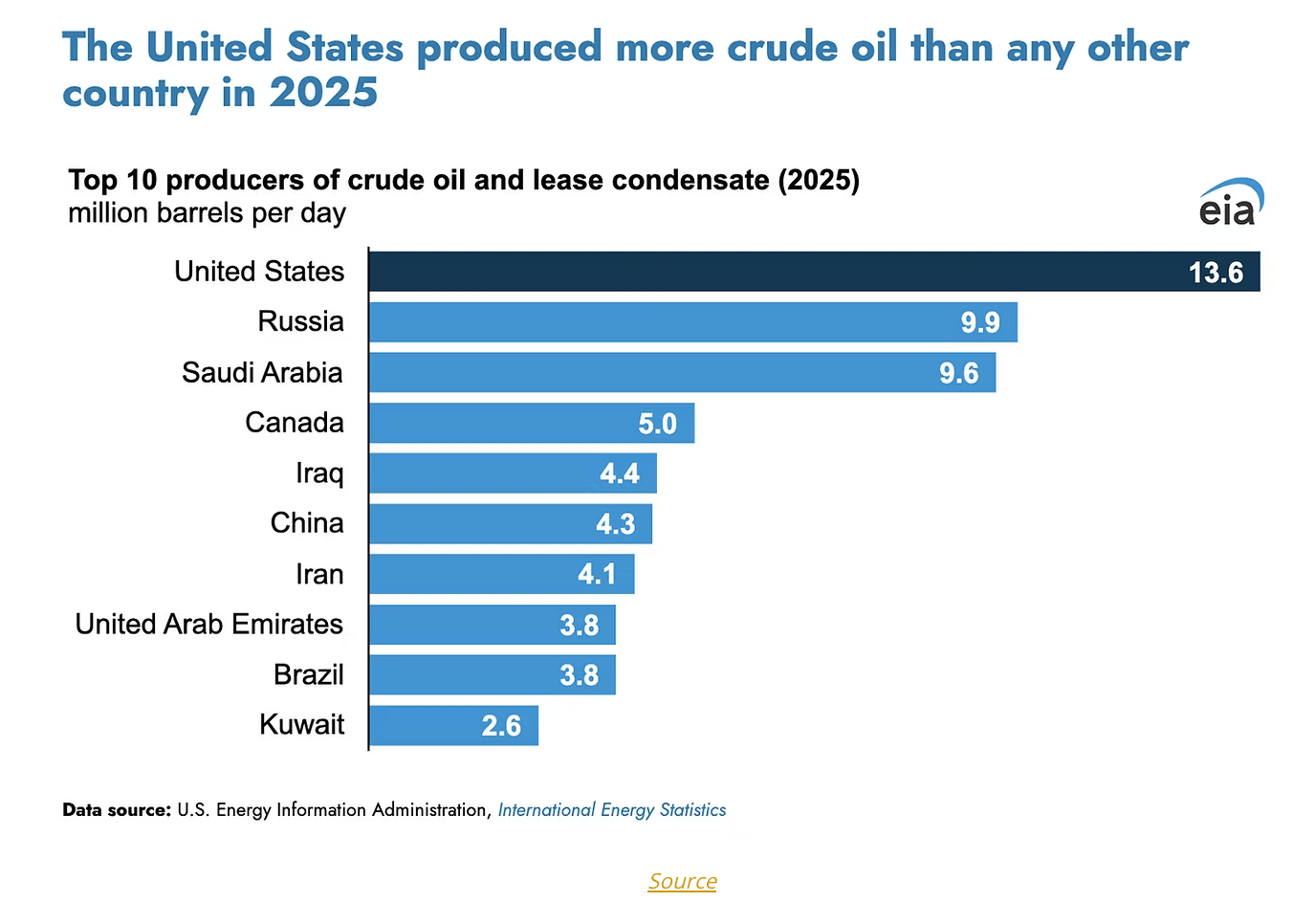

No country produces more of it than we do. America produced 13.6 million barrels a day in 2025, nearly 4 million barrels more than Russia, the world’s second-largest producer, and almost 40% more than Saudi Arabia.

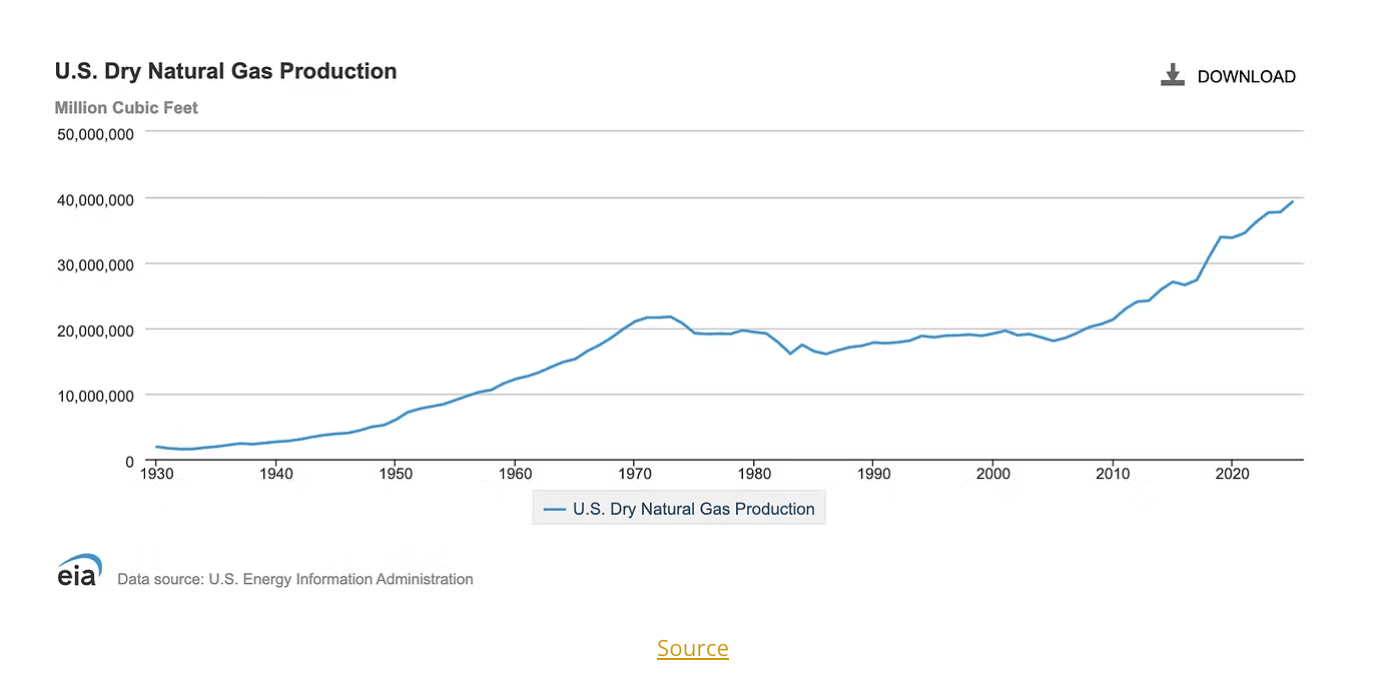

Natural gas tells the same story, stretched over a much longer timeline.

This chart shows nearly a century of US production. Note what happens after 2005.

Production stayed roughly flat for fifty years, from the early 1970s through the mid-2000s. Then the shale revolution hit and output nearly doubled in under two decades. It was the fastest, largest sustained increase in the chart's entire 95-year history.

Here the issue: none of that abundance, on its own, keeps the lights on or data centers running. Oil and gas are inputs. Electricity is what end users need, and increasingly, gas is the fuel utilities burn to make it. So the real question isn't whether we have enough oil and gas (we do). It's whether we can turn that abundance into electricity, and get it where it's needed. All while remaining competitive globally. He who has cheap electricity has a steep advantage on the global stage.

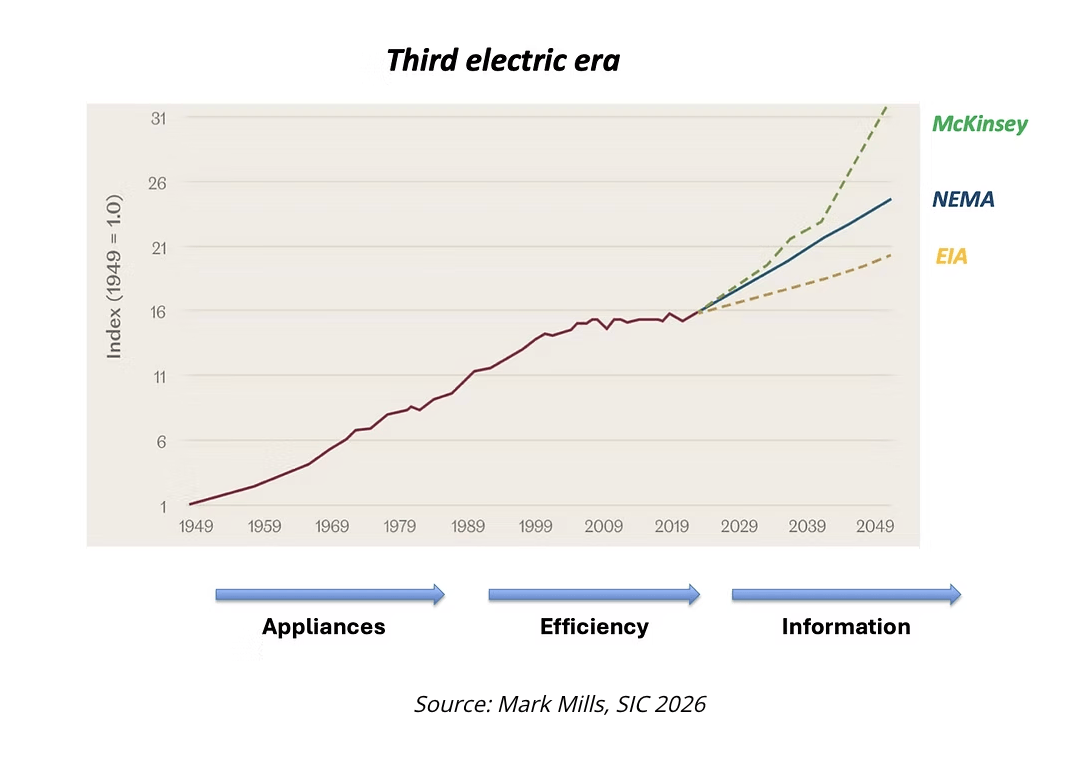

Physicist and energy analyst Mark Mills spoke at this year's Strategic Investment Conference, and his framework for the US electric sector breaks the postwar period into three distinct eras.

The first was the rise of appliances. The decades after World War II when air conditioning, washing machines, and the electrification of the American South drove a long, steady climb in demand. The second, running roughly from the early 1980s through the 2010s, was what he calls the era of efficiency: demand stayed essentially flat, not because people used less electricity, but because LEDs, better HVAC systems, and more efficient motors quietly offset most of the growth that would have otherwise happened. The result was more lumens, more cooling, more everything, for close to the same amount of power.

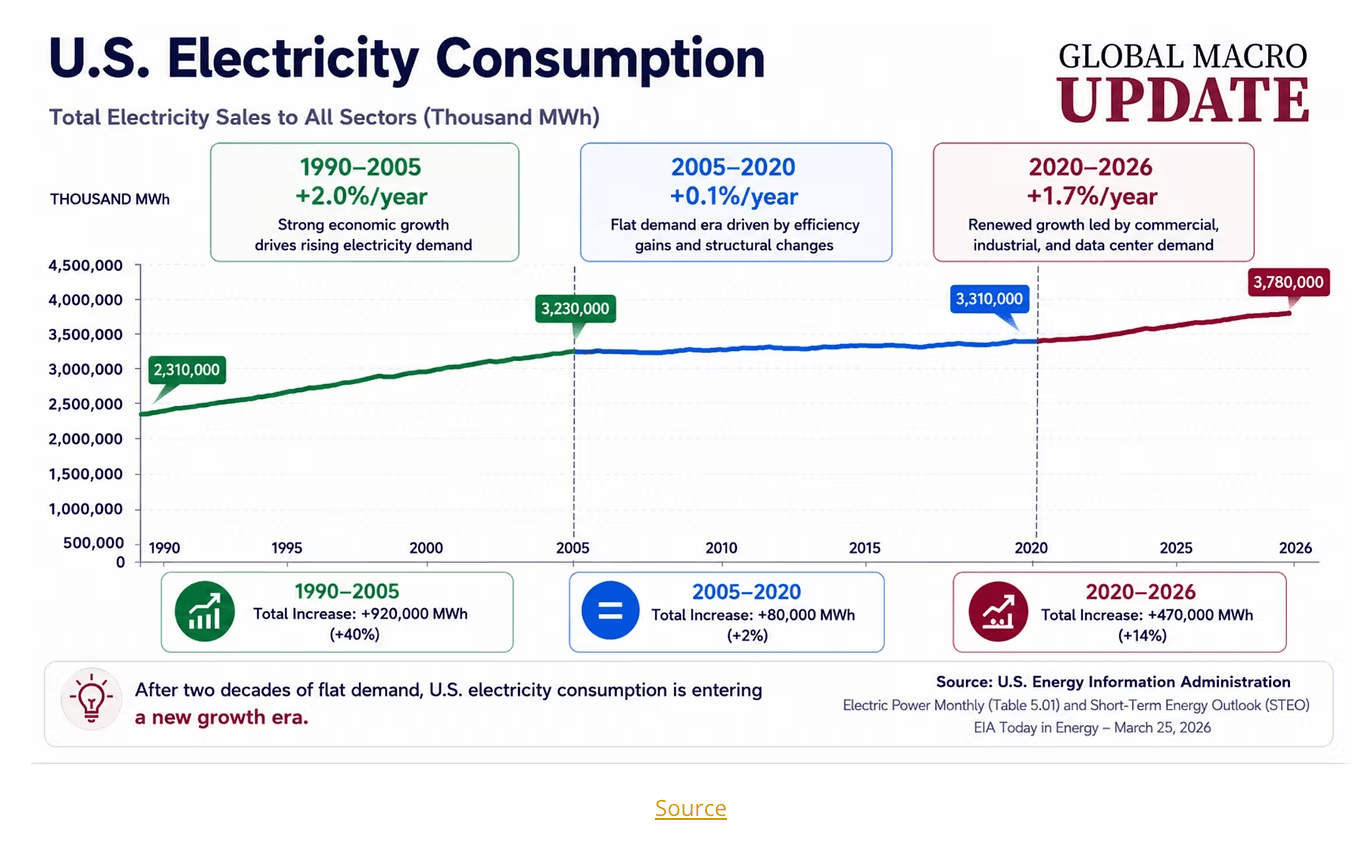

Right around 2020, the line turns. That's the beginning of Mills' third era. It's a bit of a strange move to check someone's slide against a different dataset, but the EIA's own numbers, over just the last three decades, land on the same inflection point, and the shift looks even sharper up close.

For fifteen years, from 2005 to 2020, demand grew at an average of just 0.1% a year, the back half of what Mills calls the efficiency era. Since 2020, that growth rate has jumped to 1.7% a year. Mills attributes it to data centers directly, and to the broader economic growth data centers and AI are inducing across the rest of the economy.

Mills' framework helps explain why this shift is landing so hard, so fast. Large single-site industrial loads of this scale, the kind of demand a steel mill, an LNG terminal, or now a hyperscale data center adds to the grid all at once, have historically been rare. Today that’s changing. Mills made the point that a data center isn't software. In the physics of energy, it's really a building full of heaters, powered by electricity, because everything a computer does eventually turns into heat.

Critics might reasonably say: fine, just build more equipment. The amount of new generating equipment added to US grids is back to its highest level since 2002. But because so much of that new equipment is solar and wind, intermittent, not always-on, the actual energy production capacity being added is, by Mills' account, the lowest of the century.

The point I'm trying to make is we've entered a new electrical era, on the back of a demand curve nobody planned for. Demand is surging, and electric generation capacity (supply) is not keeping up.

If energy becomes harder to deliver, the path to US based manufacturing, reshoring, and household budgets all get more expensive together, not separately.

Abundance Isn't Enough

Part of why the gap is closing so slowly: a 500-mile natural gas pipeline can be built in 12 to 18 months. A 500-mile transmission line takes 24 to 48 months. If you need power fast, gas wins by default, not because it's better, but because it's faster to deliver.

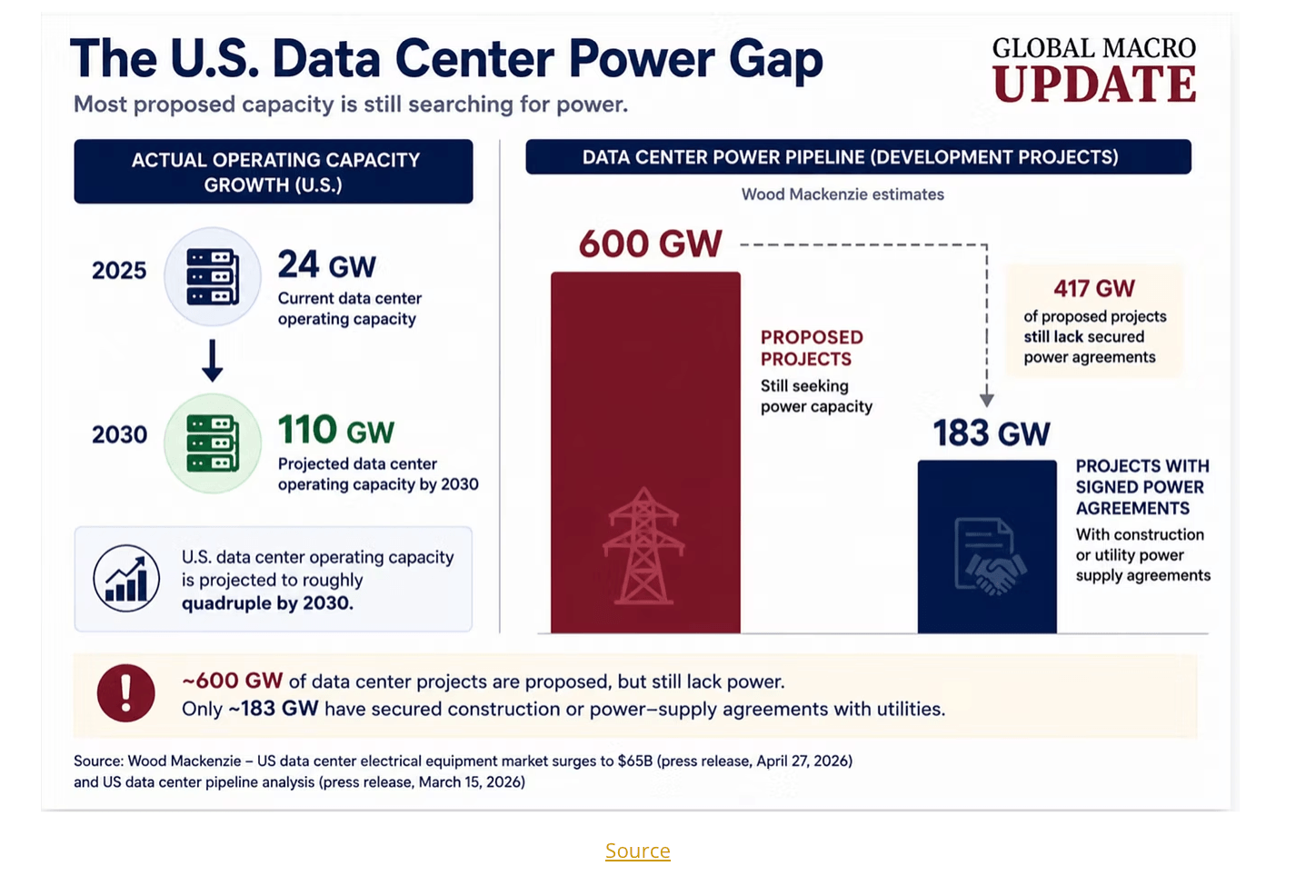

Every data center in this next chart needs electricity, not raw fuel. Electricity has to travel over wires that take years to build, not pipelines that take months. Here’s what the bottleneck looks like:

US data center operating capacity is projected to roughly quadruple by 2030. From about 24 gigawatts today to about 110. That's what's left after accounting for the projects they suspect won't make it. In Wood Mackenzie's own words: "Even accounting for expected project attrition, grid-connected data center capacity is expected to nearly quadruple in the next four years." Meaning, even after subtracting every project that stalls out or never gets built, the demand that survives is still enormous, four times what exists today.

600 gigawatts is the entire wishlist of proposed data center projects across the country, every project anyone has floated, most of which haven't secured power yet. Many of which, they say, will never get built at all. Of that 600 gigawatts, only about 183 gigawatts has actually secured a power supply agreement. The other 417 gigawatts is demand that exists on paper, with no way yet to reach the building.

The reason isn't a shortage of gas, coal, or oil somewhere in the country, it's that there's no way to get those inputs converted into usable electricity.

Utility's ratepayers are already covering the difference. Dominion Energy in Virginia, home to one of the largest data center clusters in the country, saw regulators approve its first base-rate increase in 34 years last November, with additional fuel-cost increases taking effect this July. The stated driver in both cases: data center growth outpacing the delivery system's capacity to keep up.

Not everyone agrees on how much blame data centers deserve. A report commissioned by the Data Center Coalition, the industry's own trade group, points to inflation, grid modernization costs, and gas price volatility as bigger factors nationally than load growth alone. However, even that report concedes data centers account for roughly half of the recent capacity price increases in PJM, the regional grid operator covering Virginia and twelve other states. Half is still a lot. It's just not the whole story.

Where This Leaves Us

The honest answer to "can America power this" is yes, just not yet. And not without someone absorbing the gap while the grid catches up. Right now, that's us, the ratepayers.

Fixing the grid will take years, capital, and permitting fights and delays. In the meantime, who pays for the increase in demand? That question is going to be asked in town halls and state legislatures across the country more and more often.

We have the fuel to grow our electrical generation capacity. We have the technology to do it emission free. Nuclear technology has never been better. Battery technology is advancing to the point where we’ll be able to smooth out some of the intermittent nature of solar and wind. And our ability to convert natural gas to electricity has never been more clean or efficient.

Get electricity right and it stops being the constraint on offshoring, automation, regulation, essentially, the economy. That's what real resilience looks like. In the meantime, rising electricity costs will add to the societal stress we discussed last week.

Next week, we'll pick up one of the causes you raised and take it further.

Let me know what you think — reply to this note or drop a comment