The Federal Reserve sees progress on inflation, but wants more certainty before it’s prepared to lower the policy rate.

While interest rates have presumably peaked, we remain skeptical that rate cuts will be delivered as forcefully as the market expects.

Municipals experienced their strongest two-month performance since 1986 during the final two months of 2023.

There are material short- and long-term implications for hydrocarbon markets following the COP28 meeting in Dubai, including tailwinds to oil.

Municipal bonds posted their best performance of the year, and we believe municipal credit conditions remain strong.

Starting portfolio yields may be a better guide to optimal spending than knowledge of future market returns.

The market anticipates a swift shift in the Fed cycle.

While the ECB is unlikely to raise rates further, we remain skeptical that it will deliver rate cuts as early as the market expects.

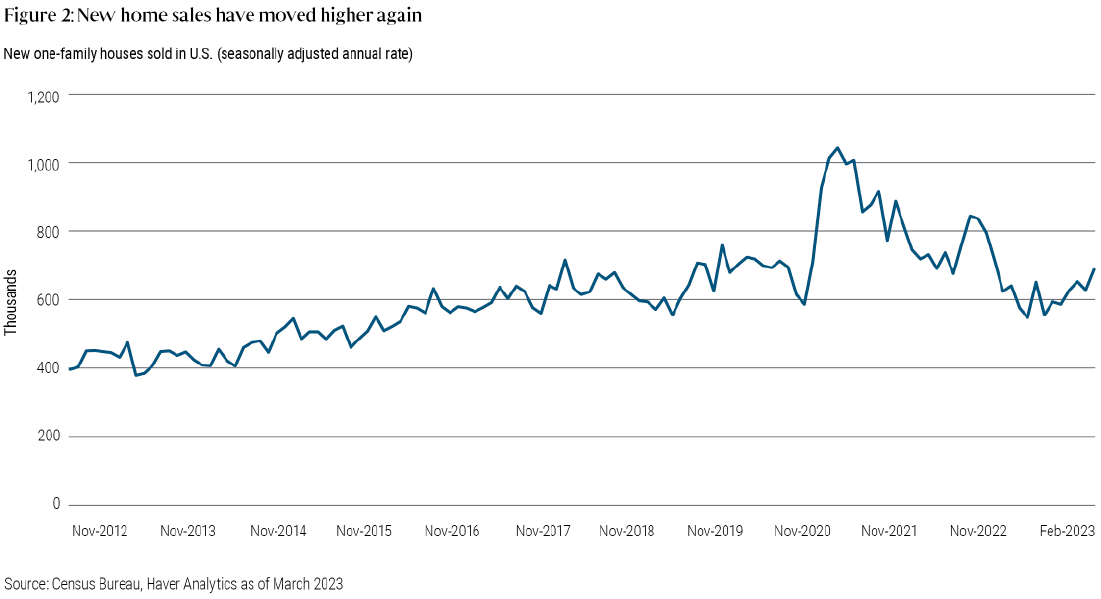

The dearth of homes for sale has underpinned the housing market’s surprising resilience and may further lift home prices despite reduced affordability.

As banks pull back from many types of lending, demand for capital is outpacing supply, providing the best potential opportunities in private credit since the GFC.

U.S. inflation cooled more than expected, and bond markets rallied, but the Fed is likely to remain in a long pause.

In our 2024 outlook, bonds emerge as a standout asset class, offering strong prospects, resilience, diversification, and attractive valuations compared with equities.

Tighter financial conditions prompted Federal Reserve officials to take a step back from data dependence, and suggest a higher bar for future hikes.

The latest inflation report raises the odds of further Federal Reserve action.

Our September Cyclical Forum was the first to be held in London, where the economic situation today reflects what’s happening around the world.

“Restrictive for longer” is now the mantra as monetary policymakers seek to bring inflation reliably to target.

The spike in bond yields presents an opportunity for fixed income investors to earn capital gains and diversify portfolios.

A liquidity gap is growing as banks curtail specialty lending, providing specialty finance investors opportunities for potential better risk-adjusted returns than we’ve seen since the GFC.

Public credit markets offer high quality investments with attractive yields and downside resilience, while we see growing longer-term opportunities in private markets.

The Federal Reserve forecasts only a modest uptick in U.S. unemployment next year as inflation cools, but history and current labor market trends make us less certain.

The European Central Bank is likely at or very near its peak policy rate, but we don’t expect rate cuts in the near term.

PIMCO’s Global Advisory Board discusses economic and geopolitical factors shaping the long-term global outlook.

We believe idiosyncratic credit events may occur over the next 12 months, but systemic bank risk is remote.

The Fed chair’s high-profile speech emphasized the central bank’s focus on taming inflation.

Commodities stand to benefit from underinvestment and the clean energy transition.

We see compelling value in high-quality, liquid fixed income assets that may offer potential resiliency if the economy weakens.

The sovereign credit rating cut is unlikely to significantly change views toward U.S. Treasuries, but questions about debt sustainability may grow louder over time.

The Bank of Japan announced changes that could allow its yield curve control program to expire gradually if economic conditions are favorable.

Amid an outlook for slower growth and more moderate inflation, the Fed shifts to data dependence.

High-quality fixed-income assets may offer the best return potential in more than a decade along with diversification benefits as a likely recession approaches.

After stubborn U.S. inflation in the first half of 2023 kept the Federal Reserve raising rates, June’s softer inflation report suggests July may mark the end of the hiking cycle.

Debt-financed fiscal policy is driving much of today’s high inflation, but as pandemic-era measures fade, central banks will likely return to their key role in managing price levels.

The European Central Bank (ECB) hikes rates and signals more tightening ahead.

Our long-term outlook for commercial real estate investing argues for a flexible, long-term approach to seize opportunities in debt and equity investments across the real estate landscape.

The Federal Reserve paused in June but raised its estimates for the policy rate later this year. We expect a July increase but remain skeptical about subsequent hikes.

State and local tax revenues sank in April, yet we believe most governments have strong fiscal positions, with ample reserves and budget flexibility to manage the decline.

With their ability to act as an inflation hedge, diversified, and return enhancer, commodities should be considered an important portfolio allocation over the long term.

The first few years of the 2020s have seen a number of acute economic, financial, and geopolitical disruptions on a worldwide scale, and it will take time for the ultimate consequences of these shocks to be fully felt.

An in-depth analysis of hedge fund performance demonstrates that, over the past 15 years, lower-beta hedge fund styles have generally achieved higher alpha, aligning with investors' objectives of maximizing returns and diversification.

Despite economic uncertainty, we see compelling value in high-quality, liquid assets that we view as more resilient in the face of a potential recession.

Although affordability remains an obstacle, recent data offer reasons to be more constructive as broader conditions still appear supportive of home prices.

An allocation to fixed income may help investors navigate a potential recession as well as uncertainty around the Federal Reserve’s policy trajectory.

Higher bond yields and improved total return potential may offer advisors a compelling opportunity to move cash off the sidelines.

March inflation data may put the Federal Reserve close to its terminal policy rate this cycle, if it hasn’t already reached it.

History suggests the lagged economic effects of tighter central bank policy are arriving on schedule, but any eventual normalizing or even easing of policy will still likely require inflation to decline further.

Slower credit growth may curtail broader U.S. economic growth, taking pressure off the Federal Reserve.

In a dovish move, the central bank raises rates by half a point.