Earlier this year, in a series of articles (Does Rebalancing Really Pay Off?? and Does Rebalancing Reduce Risk?), Michael Edesess argued that rebalancing neither increases returns nor reduces risk, although in the latter case his conclusion was based on one’s definition of risk. However, it turns out that the debate on whether there is value in rebalancing – in terms of return enhancement and/or risk management benefits – actually depends on the similarity (or lack thereof) of the returns between the available investments in the first place.

The conventional view of portfolio rebalancing is that it enhances long-term returns by periodically selling the investments that are up (and overweighted) to buy those that are down (and underweighted), in the process of realigning the portfolio to its original target allocation.

Yet the reality is that because most investments go up far more often than they go down, systematic rebalancing is more likely to consistently liquidate the best-performing investments to buy ones with lower returns instead – especially when rebalancing across investments that have very significant return differences in the first place (e.g., rebalancing from stocks into bonds).

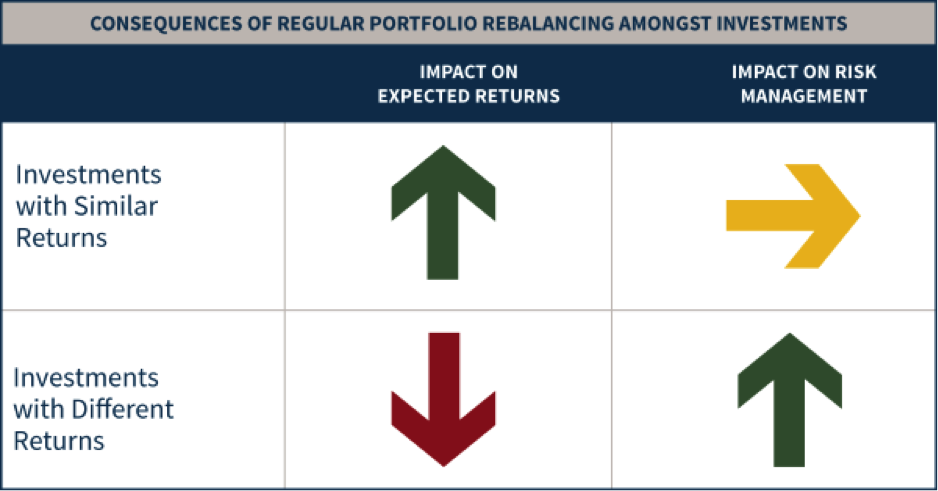

As a result, rebalancing may be helpful as a risk management strategy – otherwise higher-returning stocks would compound to the point that they are significantly overweighted relative to lower-returning bonds – but it’s only when rebalancing amongst investments with similar returns in the first place that rebalancing can provide a return-enhancement potential.

In other words, it’s crucial to recognize the role that rebalancing really does – and does not – play in a long-term portfolio. For the typical diversified stock/bond investor, the expectation should be that rebalancing will likely reduce long-term portfolio returns, but that it may be worthwhile anyway because even if returns are lower, risk-adjusted returns may be improved if the risk is reduced by even more. On the other hand, in some cases returns really can be enhanced as well, but likely only when rebalancing across similar-return investments, such as amongst sub-categories of equities.

How portfolio rebalancing can reduce long-term returns

The classic purpose of portfolio rebalancing is to realign the balance of investments in a portfolio, generally to stay in accordance with its original target weightings. In a world where asset classes have materially different long-term returns, this is critical to ensuring the portfolio does not compound to the point of violating the investor’s risk tolerance.

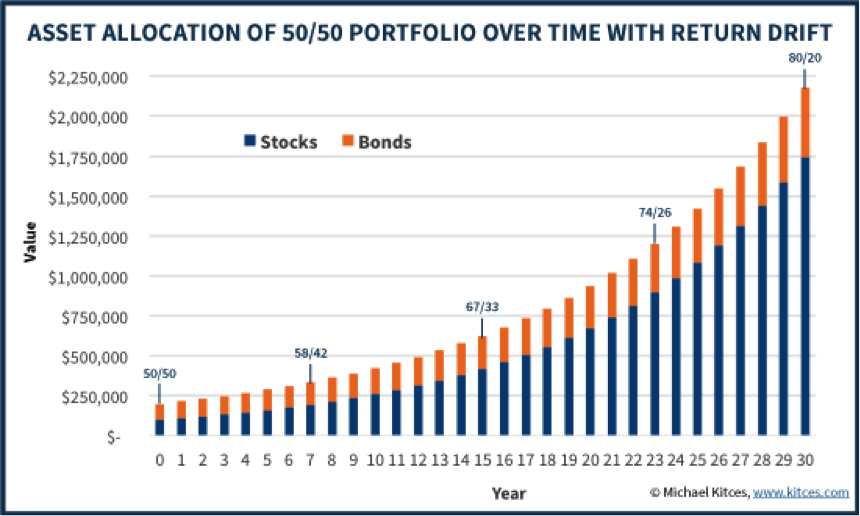

For instance, the long-term nominal return on stocks is about 10% per year and for bonds it is only 5%. As a result of the different compounding rates, this means the percentage of the portfolio allocated to equities will become larger and larger over time.

As shown above, the “bad news” is that over time, what starts out as a 50/50 portfolio drifts to 67/33 by 15 years, and nearly 80/20 after 30 years! Thus, an investor’s equity exposure will become far greater than what was originally intended and perhaps greater than what he or she can tolerate.

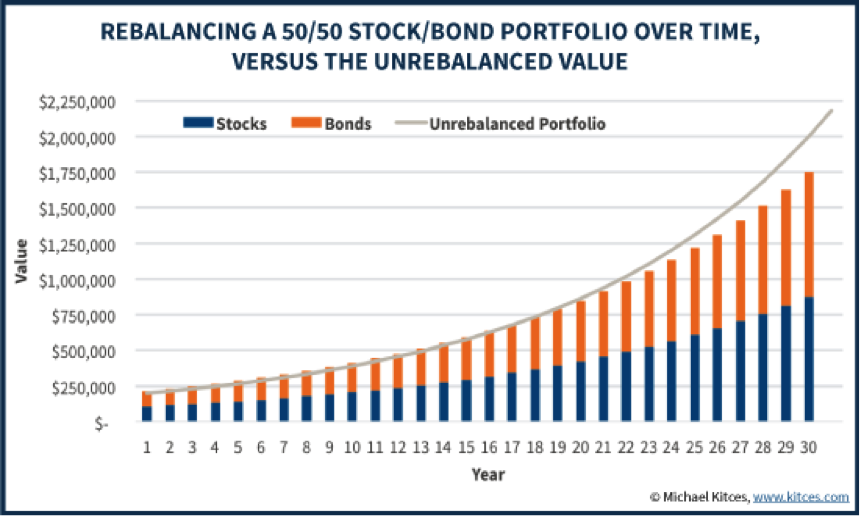

Yet the reality is that regular rebalancing to keep the client’s equity exposure from drifting too high leads cumulative portfolio returns to be reduced, not enhanced! After all, rebalancing will systematically sell the higher-returning asset (stocks) to buy more of the lower-returning asset (bonds), which just drags down the long-term return.

The graph below compares the cumulative wealth of an annually rebalanced 50/50 stock/bond portfolio to a buy-and-hold portfolio that starts out 50/50 but is allowed to drift over time.

As these results show, rebalancing to prevent equity exposure from drifting higher also curtails the favorable returns that come with allowing equities to compound. The portfolio that starts out at $100,000 each in stocks and bonds and is annually rebalanced only grows to $1,750,991 over time, compared to the buy-and-hold portfolio that grew to $2,177,134.

Granted, the buy-and-hold portfolio grew because it allowed equity exposure to drift higher and higher, potentially beyond the client’s tolerance (and the client may not have even needed to take the risk). Still, rebalancing to keep risk exposure constant was not a return enhancement; it was a detriment to returns, albeit an outcome the client may have deemed necessary as a trade-off to manage risk.

The risk management benefit of rebalancing with (real-world) volatility

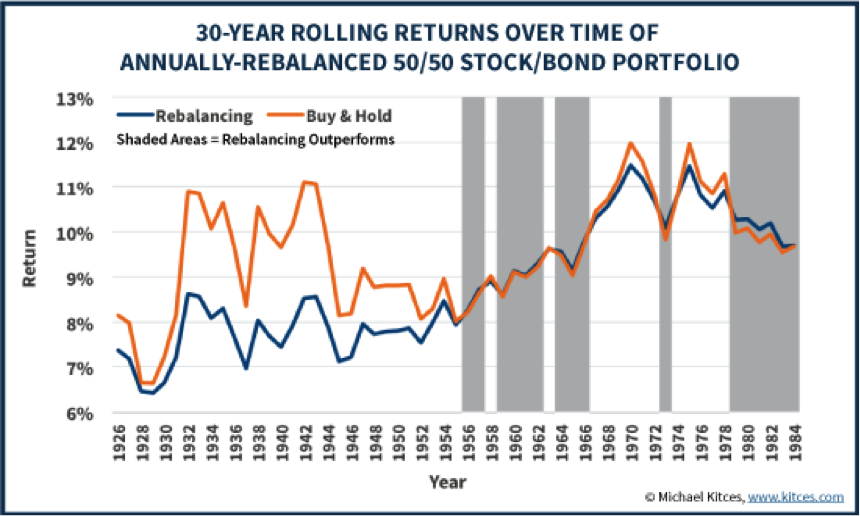

Of course, while stocks may outperform bonds in the long run, they rarely do so in the exact “straight line” path shown above. Instead, bond and especially stock returns are more volatile, introducing the possibility of selling stocks when they’re up to buy bonds when they’re down, or selling bonds when they’re up to buy stocks after a crash.

A question emerges then: is the return sacrifice of rebalancing from stocks into bonds mitigated or offset by the potential for sell-high buy-low opportunities that emerge given the volatility along the way?

To evaluate this question, the chart above uses rolling 30-year historical periods to compare rebalancing between large-cap U.S. stocks and intermediate-term government bonds (given real-world volatility) to a buy-and-hold strategy (which allows equity exposure to drift higher over time). As the chart reveals, over most 30-year periods, buy-and-hold outperforms rebalancing. And when the rebalanced portfolio does beat the buy-and-hold portfolio (the zones shaded grey, where the blue line is above the orange line), the difference is usually negligible.

On the other hand, given that a buy-and-hold portfolio can drift to 80%+ in equities over a multi-decade period, regular rebalancing may still be appealing to manage risk and avoid excess exposure to risky-but-high-return investments. Or viewed another way, if rebalancing allows for similar returns to the buy-and-hold portfolio but does so with less risk (by not drifting to 80%+ in equities), rebalancing may be superior on a risk-adjusted basis even if absolute returns aren’t higher. Still, though, this means that rebalancing is not a return enhancing strategy, but instead a return reducing strategy that is done for risk management purposes, and perhaps the possibility of slightly higher risk-adjusted returns and a slightly improved Sharpe ratio.

Enhancing returns by rebalancing amongst equities (or other similar-return asset classes)

While rebalancing between high- and low-return asset classes (e.g., stocks and bonds) systematically sells higher-returning investments to buy those with lower returns (and therefore enhances risk management but generally reduces returns), in the case of rebalancing between investments that have similar returns in the first place, the expected outcome is different.

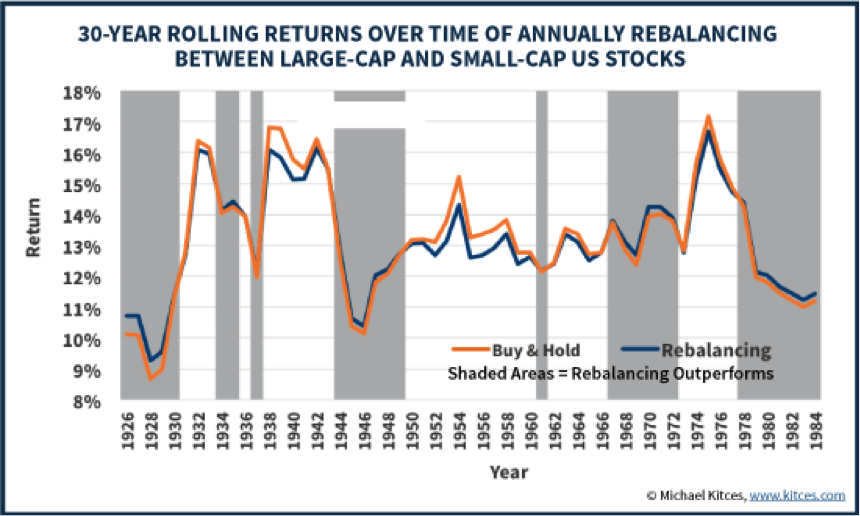

The distinction is that when the investments have a roughly similar long-term return to begin with, rebalancing will not necessarily reduce the long-term compounding of high-return investments. Instead, it will create opportunities to sell high and buy low as the investments periodically outperform or underperform each other (even as they converge to similar long-term returns).

In other words, if we assume that the investments will have a similar long-term return, then short-term outperformance by one implies that the other may be more likely to outperform in the future as their long-term returns revert towards the mean. Rebalancing should be able to take advantage of those regression-to-the-mean opportunities.

And in fact, that’s exactly what we see when we look at two volatile asset classes – large-cap and small-cap U.S. stocks – which have roughly the same long-term historical returns (small-cap stocks have historically outperformed, but only slightly). Rebalancing between the two, which have similar returns and a high (but less than 1.0) correlation, does enhance the returns compared to just buying-and-holding each, as shown below.

In fact, investment guru William Bernstein (in a white paper aptly entitled “The Rebalancing Bonus”) found that in general, for similar-returning asset classes, the higher the volatility of assets and the lower their correlations – creating even more rebalancing opportunities – the greater the potential “rebalancing bonus” will be. (Though Bernstein also noted that, with different-return asset classes, like stocks and bonds, rebalancing will lead to lower returns, albeit with lower risk.)

The fuzzy economic benefits of rebalancing – Better returns, risk management, or higher risk-adjusted returns?

When it comes to quantifying the economic benefits of rebalancing, it is surprisingly difficult, as most studies fail to make a distinction between rebalancing among similar-return investments and different-returning investments.

For instance, a 2010 study from Vanguard by Jaconetti, Kinniry and Zilbering found that rebalancing stock/bond portfolios reduced returns, generally by about 0.50% annually in the long run. Portfolio volatility was reduced as well because rebalancing reduced the average equity exposure. The significant reduction in volatility, combined with only a slight reduction in returns, did at least enhance risk-adjusted returns.

Other studies have found a return enhancement to rebalancing, but typically no more than 0.50%/year (and often less), with the results highly contingent on the underlying asset classes used in the analysis. Ironically, the more equity-centric the portfolio already is – and the more sub-categories of equities that are used – the better rebalancing looks, as it limits the return-reducing aspect of systematically selling high-return investments (e.g., stocks) to buy lower-returning ones (e.g., bonds) and accentuates rebalancing amongst similar-return investments instead.

In other words, in the context of Bernstein’s “rebalancing bonus” study, the benefits of rebalancing will vary directly as a function of types of investments/asset classes held, and in particular the differences in the volatilities and correlations of the investments. The best investments for rebalancing are the ones that are volatile and uncorrelated (creating more opportunities for rebalancing), but with similar underlying long-term return expectations. Yet if rebalancing does not extend to lower-return investments (e.g., bonds) as well, eventually the portfolio may spin up to an undesirable level of risk.

Either way, though, rebalancing does produce some benefit, whether it’s risk management (across high- and low-return investments), higher returns (across similar-returning investments with less-than-perfect correlation) or better risk-adjusted returns (where returns are reduced but volatility is reduced even more). It’s important to recognize in which situations each may apply as it impacts the way that rebalancing should be implemented and the expectations to set about its prospective benefits!

The original version of this article appeared here on the Nerd’s Eye View blog.

Michael Kitces is a partner and the director of research for Pinnacle Advisory Group, co-founder of the XY Planning Network and publisher of the financial planning industry blog Nerd’s Eye View. You can follow him on Twitter at @MichaelKitces.

Read more articles by Michael Kitces