Some clients are surprised at how I look at critical financial decisions. But when I reframe them from the conventional way of looking at those decisions, I can get them to shift longstanding beliefs and make changes. Here are a few decisions and starting points from the client.

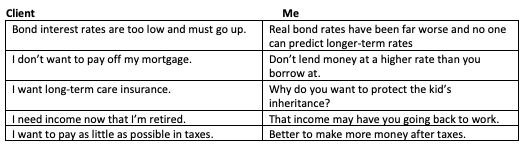

- Client: I don’t want bonds because they produce little income. Interest rates have to go up from our current all-time low.

Me: Real after-tax rates are nowhere near an all-time low. The purpose of fixed income has never been income.

I advise the client to “get real.” By this I mean that they should think in terms of inflation-adjusted after-tax returns since it is spending power that matters. In 1980, nominal rates were 12% which translated to earning $12,000 on a $100,000 bond. If a third went to taxes, that amount was closer to $8,000 or an 8% return. Clients sometimes remember those days fondly until I point out that inflation averaged 12.5% and they lost roughly 4.5% of their spending power. Rates are much better today than a few decades ago.

I remind them that the purpose of fixed income is to stabilize one’s portfolio and to keep up with inflation and taxes. When stocks tank, those boring high-quality bonds act as a shock absorber and allow one to rebalance to buy stocks while they’re on sale. As far as predicting intermediate-term rates goes, the top economists have called the direction of the 10-year Treasury bond correctly about 30% of the time over the past few decades. A coin flip would have been more accurate.

- Client: Why should I pay off my mortgage since my rate is only 3.5%, while my portfolio is doing better? After the tax-deduction, I’m only paying 2.5%.

Me: Because you don’t want to borrow money at 3.5% and lend it out at 2.26% (the annualized yield of the Vanguard Total Bond fund).

A mortgage is the inverse of a bond. And most bonds are taxable, while munis yield far less and have risk (possible defaults from underfunded pension and healthcare liabilities). You want to compare the after-tax ultra-low risk investments to paying off the mortgage. Paying off the mortgage is a risk-free return since it has no impact on the ultimate sales price of the house.

The pushback I get includes:

-

What if rates go up then my mortgage will look good, right? Yes, but your bonds will have gone down.

-

Why should I put more money into my house? You shouldn’t – I’m not suggesting a remodel. I’m only suggesting a change in how you finance the house.

Admittedly, one needs to have enough liquidity, since you can’t easily get this money back. I’m not suggesting paying taxes to get the money out of a tax-deferred account to pay down the mortgage.

Remember that a bank makes money by lending it out at a higher rate than it pays depositors. When you can disintermediate the bank, go for it!

- Client: I need long-term care insurance.

Me: Why, do you want to protect your heirs?

Typically, the client says they think they have a high probability of ending up in long-term care. I’m a big believer in insuring for what one can’t afford to lose. But long-term care insurance has a unique problem in that you can no longer buy long-term care insurance with a guaranteed premium, unless it’s in a hybrid life policy, which has other problems. I have many people come to me and say something like, “after 10-years, the insurance company just raised my premium by 75% and now I’m closer to the possibility of needing it.”

For someone with less money, I recommend against it as they are likely to have Medicaid pay for chronic long-term care. And for someone with a lot of money, I recommend against it because they can self-insure. If the actuaries again underprice the cost of long-term care insurance, they will jack up the premiums and find a way to make money. All insurance companies (even mutual companies) need to cover their overhead and make a profit. Thus the odds are against you. I recommend self-insuring.

It’s only those in the middle with say a $1 to $2 million net worth for whom long-term care is worth exploring. The industry is quick to point out the high costs of long-term care, but fails to mention the costs avoided or the average time one spends in long-term care. For a couple, I note that one is likely to be the caregiver for the other first and ,if the survivor goes to long-term care, she will no longer be spending money on a house, travel, insurance, eating out, etc.

The Center for Retirement Research at Boston College determined that, of those surveyed, 50% of men and 40% of women stayed 100 days or less. Medicare will cover the full cost of care in a skilled nursing facility for 20 days and partial costs thereafter, up to 100 days.

The key reason to buy long-term care is to protect one’s heirs from losing inheritance in the unlikely event of spending several years in long-term care.

- Client: I need an income portfolio now that I’m retired.

Me: Do you like paying taxes and want to go back to work?

It’s completely natural that those of us who were programmed to live below our means and grow a nest egg are terrified at the prospect of spending that nest egg down. Yet I’ve seen more people lose their nest egg by going for income. Take, for example, master limited partnerships (MLPs) that were billed as “safe” alternatives to bonds, real estate partnerships billed with “no market risk,” high-yield bonds that were “really safe,” and even dividend stocks which badly underperformed the so-called overvalued growth stocks. Those were all tax-inefficient and badly underperforming.

Here are two important concepts I teach clients. Think of your portfolio as stored energy that gives you choices in life. You can’t take it with you so it’s okay to spend it down. Look at total return rather than income. And if you really want a tax-efficient and diversified income fund, build your own 4.75% income fund.

- Client: I want to pay as little as possible in taxes.

Me: The much better goal is to make more after taxes.

I’ve seen all sorts of tax strategies backfire. I’ve seen people earning less in muni bond funds than if they had a Treasury money market, even after paying taxes. Tax-deferral strategies such as bad 1031 real-estate exchanges can result in the capital gain completely vanishing (but no taxes were paid). There are many annuities and other insurance products that minimize taxes by minimizing returns. As noted earlier, when I tell the client to pay off the mortgage, it typically results in higher taxes.

As a CPA, a large part of my client engagement includes these tax strategies. Owning tax-efficient and low-cost investments are key along with asset location, withdrawal strategies and the like. But all of those are with the goal of making more after taxes while managing an appropriate level of risk.

Every one of these clients’ wants is instinctual. I have those same instincts and have to continually fight them. When it comes to money, our instincts fail us.

Reframing financial decisions

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

More Fixed Income Topics >