The first few years of retirement are the most vulnerable to risk from adverse market movements. Clients nearing or in retirement ask me how to mitigate that risk. There are many methods I’ve reviewed; most have problems and a few even increase that risk. I’m going to review the research on safe spending rates and then critique common methods of risk mitigation.

The first few years of retirement are the most vulnerable to risk from adverse market movements. Clients nearing or in retirement ask me how to mitigate that risk. There are many methods I’ve reviewed; most have problems and a few even increase that risk. I’m going to review the research on safe spending rates and then critique common methods of risk mitigation.

I’ll offer the practical methods to reduce sequence-of-return risk that I suggest to my clients.

Safe spending rates

I’ve done extensive Monte Carlo modeling. Though there has been quite a lot of criticism of Monte Carlo modeling, much of it is misplaced. Many Monte Carlo simulation outputs are garbage, but the fault is in the assumptions, not the modeling. As they say, “garbage in, garbage out.” Assuming past returns will continue is dangerous. So is ignoring costs. One fair criticism is in the use of a normalized distribution when we live in a world of fat tails. For example, at the start of 2022, the yield on the Bloomberg U.S. aggregate bond index (AGG) was approximately 1.6%, which represented the expected return for that asset. But since then, through June 3, the return for the AGG has been -9.15%, which is a three standard deviation event. That should happen once every three centuries. If rates continue to rise, we will soon hit four standard deviations, which would truly be a black swan event. Jason Zweig recently wrote in The Wall Street Journal that this has been the worst start of the bond market since 1842.

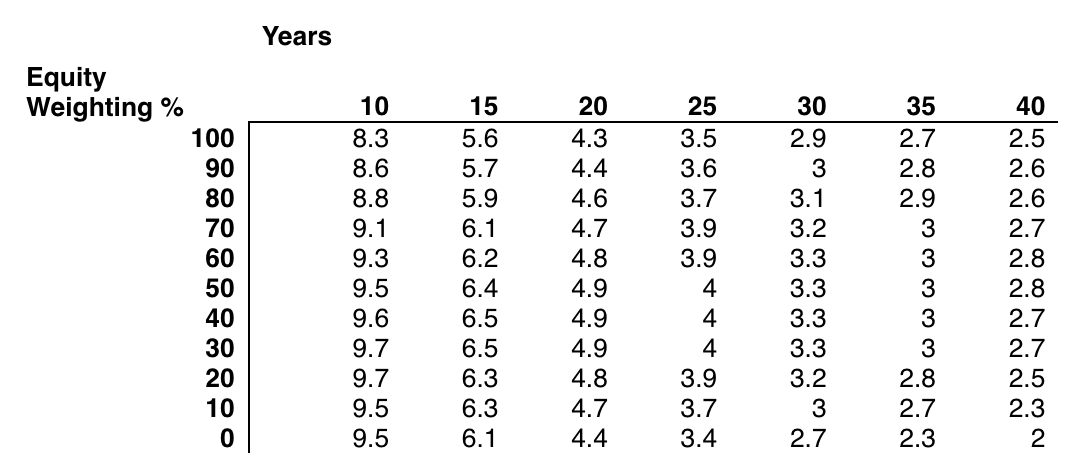

My own simulations come up with safe spending rates (increasing with inflation) far below the famous 4% rule. The best work I’ve seen came last year from Morningstar with its paper, The State of Retirement Income: Safe Withdrawal Rates. The study by Christine Benz, Jeffrey Ptak, and John Rekenthaler replaced the 4% rule with the 3.3% rule, meaning a portfolio of 50% equities has a 90% chance of lasting 30 years or longer.1 But that is not for everyone; the asset allocation greatly impacts the outcome. Based on a 90% success rate, they came up with the following table, showing the safe spending rate depending on the clients’ life expectancies and asset allocation:

The future is very hard to predict, and 90% success may be exaggerated when considering long periods of time. That’s why it’s important to have ways to mitigate risk rather than blindly spending at these percentages with increases each year based on inflation.

Traditional risk-mitigation strategies

There are several traditional ways of mitigating sequence-of-return risk. Many have emotional appeal but are flawed. Here are a few:

Cash reserve – Keeping a few years’ cash is often recommended to allow markets to recover. It is the traditional way to manage sequence-of-return risk. It feels great to know you have this bucket as a reserve, but, like most things in investing that feel good, it’s an imperfect approach. Since cash returns very little, it ends up increasing risk later. It’s the one asset class that’s virtually guaranteed to underperform inflation. As of the end of April 2022, cash bought 8.3% less than it did a year earlier.

Income laddering – Building bonds or CDs to mature in years when the money is needed also has emotional appeal. Unfortunately, it suffers from inflation risk (unless TIPS are used) and return of principal is not income. In addition, sticking to an overall asset allocation is key, so it would have the client selling equities.

Dynamic spending rules – There are many rules about when spending would need to be cut based on portfolio performance. These aren’t bad but don’t go far enough in helping the client to know where spending would be cut.

Reverse mortgage – Wade Pfau is an advocate for reverse mortgages. He provides an intuitive argument. I respectfully disagree. I agree with him that a reverse mortgage should not be looked at in isolation as an expensive source of cash. But it’s a very expensive source. Not only are the costs high, but it generally makes no sense to lend money out (a bond) at a lower rate than one borrows at (any mortgage). It could work as a last resort, though I believe in disintermediating the bank and mortgage broker whenever possible.

SPIAs and QLACs – These annuities also have emotional appeal and give some protection against a long life. While these mortality credits have value, I’m more afraid of inflation. Some may disagree with me, but there is a reason the insurance company actuaries no longer offer these with CPI-U escalators. And those annuities with annual fixed increases have more inflation risk, as it increases duration. In 25 years, the cash stream from a fixed-rate SPIA loses 52% of its purchasing power with 3% annual inflation and 85% with 8% annual inflation.

Real-life risk-mitigation strategies

These won’t have as much emotional appeal as those I just discussed. But they are superior in reducing risk and lead to long-run safety, allowing clients to enjoy retirement.

Retire slowly – It’s very hard to go from working full-time for decades to suddenly having nowhere to go. I’ve found that people typically have more free time in the earlier years of retirement, as they have more time to travel and do other things that cost money. I often suggest getting a part-time gig doing something that gives them satisfaction. This brings in some money to lower the withdrawal rate in early years, and the client has less time to spend money. And, if the client is below Medicare age, the work could provide lower cost health insurance.

Develop a flexible budget – I’m not against dynamic spending rules, but they don’t go far enough. One must have a plan to quickly implement should markets not cooperate. Thus, I recommend a budget with line items separated between discretionary and non-discretionary. For example, a couple could budget $15,000 for travel, but allocate $10,000 for discretionary trips and $5,000 for non-discretionary trips such as visiting the grandchildren. A new car could be all discretionary, since one can delay buying the new car as long as the old one is safe to drive. Also, regarding non-discretionary expenses, it’s important to have a line item called “contingencies.” This is for unexpected expenses that happen every year, like needing a new roof or expensive dental work.

Buy the right annuity and spend more now – I’m not referring to SPIAs or QLACs that have a ton of inflation risk and costs. I’m referring to delaying Social Security. It’s an inflation-adjusted annuity backed by the U.S. government with a 100% survivor benefit. In addition, the Social Security mortality table is based on average life expectancy, and wealthier people statistically live longer because they are better educated, take better care of themselves, and have better access to health care. I tell clients they can spend more now than the safe spending rate, as they should think of the money they would have received from taking early Social Security as buying the best annuity on the planet. The spouse with the greater Social Security benefit should wait until age 70 unless both spouses are in poor health.

The home – This is the one asset that can be enjoyed and appreciates in the long run. Cars can be enjoyable but depreciate. Hopefully, the client doesn’t enjoy that low-cost index fund. At some point, a client could sell the home to downsize or, if the client absolutely refuses to leave the home, they could opt for a reverse mortgage as a last resort if they were completely running out of money.

Start conservatively – This is the least appealing of the real-world risk-mitigation methods. For example, the client could decide to use a 3% spending rate instead of a 3.3% rate. The downside is that they have worked so hard to achieve financial independence and they should enjoy it. But I tell clients that I’d rather them come back to me in a few years saying they have too much money than they are running out of money. The first is an easier problem to solve.

If I compare the traditional to real-world risk-mitigation strategies, an analogy is eating pizza versus broccoli. We know one tastes better, but the other is better for us. Keeping a cash reserve of a few years is like pizza, while developing a flexible budget is like steamed broccoli. Real-life solutions lead our clients to more enjoyment from life in the long run.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

1In fairness, that study was rebutted by Bill Bengen here.

The first few years of retirement are the most vulnerable to risk from adverse market movements. Clients nearing or in retirement ask me how to mitigate that risk. There are many methods I’ve reviewed; most have problems and a few even increase that risk. I’m going to review the research on safe spending rates and then critique common methods of risk mitigation.

The first few years of retirement are the most vulnerable to risk from adverse market movements. Clients nearing or in retirement ask me how to mitigate that risk. There are many methods I’ve reviewed; most have problems and a few even increase that risk. I’m going to review the research on safe spending rates and then critique common methods of risk mitigation.