Central bankers generally believe in an abstract phenomenon known as the neutral real rate of interest, or r-star. It’s the inflation-adjusted rate that should prevail when the economy is balanced with price increases subdued and the labor market healthy.

When inflation is too high, policymakers move rates above neutral to rein it in; when employment is too low, they bring rates below neutral to stimulate the economy and foment job creation. It’s a central concept in monetary policy, but no one ever knows exactly where neutral is in real-time.

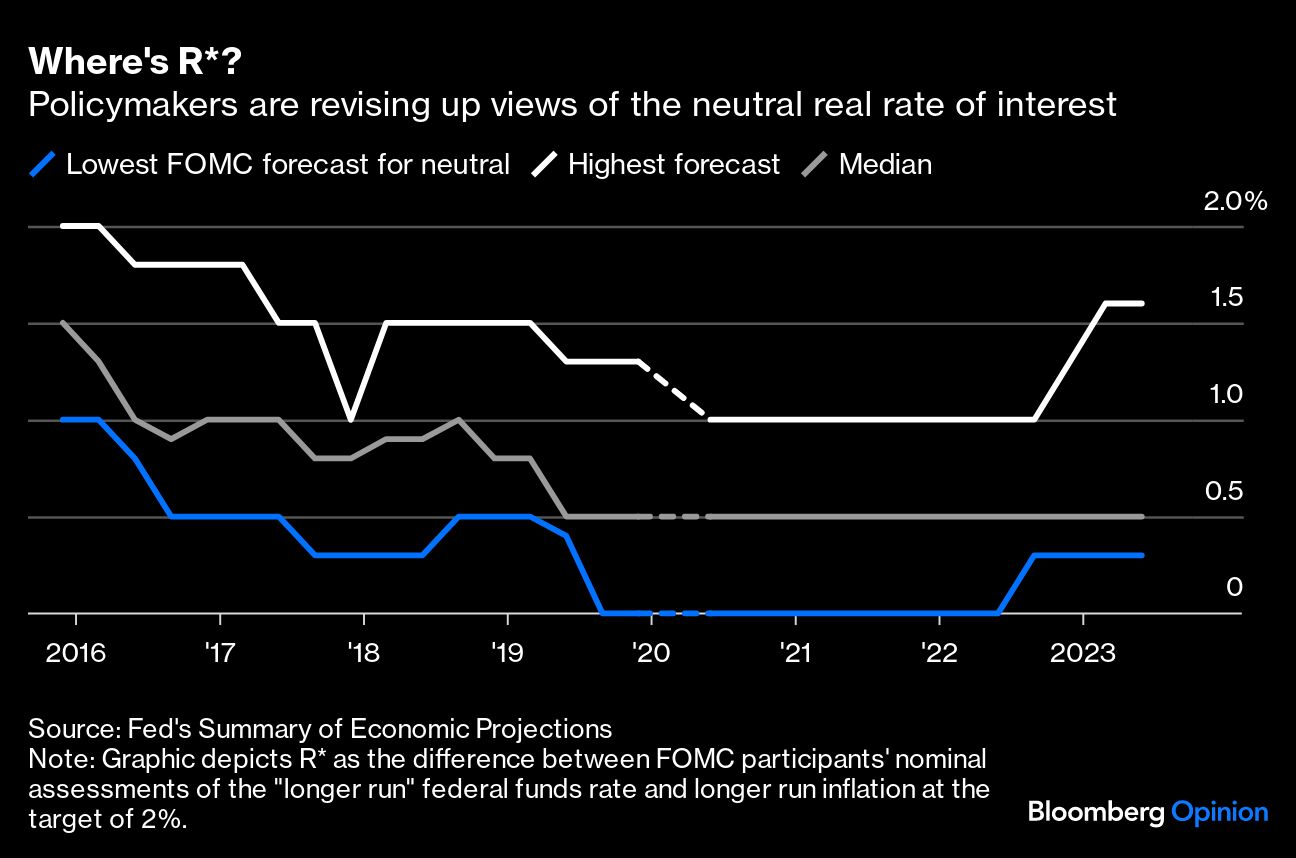

For better or worse, some economists now have a hunch that r-star might be rising in the US — perhaps because of demographics, persistently large deficits, or other factors. On the Federal Reserve’s rate-setting committee, the median participant still ballparks it at around 0.5%, but the latest quarterly survey of Fed participants suggests that a few of them now think it has moved up, as the following chart shows. If true, that would have meaningful implications for where the Fed must ultimately take policy rates to cover the last mile in the inflation fight as well as where longer-term Treasury yields will settle (they recently touched the highest since 2007).

That brings us to this year’s Kansas City Fed symposium in Jackson Hole, Wyoming, which is appropriately dubbed “Structural Shifts in the Global Economy.” Given the title, investors seem eager to hear what Fed Chair Jerome Powell thinks of the r-star debate when he takes to the dais for his annual policy speech.

But Powell has already revealed a lot about his views on r-star — starting with his debut lecture in Jackson Hole five years ago. Here are a couple takeaways from Powell’s early Jackson Hole speeches that hint at where he stands on the equilibrium real rate of interest.

‘Wait One More Meeting’

In Powell’s first Jackson Hole speech, “Monetary Policy in a Changing Economy,” he paid homage to former Fed Chair Alan Greenspan and his policymaking during the 1990s “new economy” period. At the time, Greenspan held interest rates lower than policy orthodoxy would have otherwise called for, fostering the elusive “soft landing” and the continuation of a long economic expansion.

In the lecture, Powell compared the macroeconomic “star” variables (including r-star and its cousin u-star, the natural rate of unemployment) with the celestial stars by which seafarers used to navigate. Powell clearly acknowledged their importance but noted that, unlike the celestial stars, they move unpredictably, making them hard to use as guides. In Powell’s telling, Greenspan succeeded by exercising a healthy skepticism for “imprecise estimates of the stars.” The lesson he drew from that period was to be patient and follow empirical data. Here’s how he put it (emphasis mine):

Under Chairman Greenspan’s leadership, the Committee converged on a risk-management strategy that can be distilled into a simple request: Let’s wait one more meeting; if there are clearer signs of inflation, we will commence tightening. Meeting after meeting, the Committee held off on rate increases while believing that signs of rising inflation would soon appear. And meeting after meeting, inflation gradually declined.

Proactive, aggressive policymaking may have been appropriate at one time before Chair Paul Volcker established the central bank’s credibility in the 1980s and anchored the nation’s inflation expectations. But that hasn’t been the case since the 1990s, and all signs suggest that expectations remain relatively well-anchored, giving policymakers flexibility.

Powell is likely to lean on Greenspan’s wisdom again in the current environment. The Fed has already raised interest rates by 525 basis points since March 2022 and reported inflation has been coming down for months — notwithstanding the increase in energy prices, which should temporarily push headline inflation higher in August.

Some economists are worried that the apparent reacceleration of economic growth in the past couple of quarters could lead to durably higher inflation, all else being equal, but Powell is likely to take the “wait one more meeting” approach and see how far current disinflation trends run.

Respect the Lags

In 2019, Powell weighed in again. The circumstances were much different from those that prevail today, of course, because inflation was running well below the Fed’s 2% target. The median estimate of r-star was falling, and the question before policymakers concerned how best to respond to President Donald Trump’s trade war with China — the unique economic threat of the time. (On Twitter, Trump was campaigning for lower rates and regularly treating Powell like a punching bag, including a below-the-belt jab on the day of the Jackson Hole speech that cast the Fed chair as an “enemy” of America.)

In his attempt to focus on the task at hand, Powell turned again to the stars — and his view about their inherent uncertainty — to gently push back against the demand for impulsive action in his 2019 speech, “Challenges for Monetary Policy.” As he put it:

Because the most important effects of monetary policy are felt with uncertain lags of a year or more, the Committee must attempt to look through what may be passing developments and focus on things that seem likely to affect the outlook over time or that pose a material risk of doing so. Risk management enters our decision-making because of both the uncertainty about the effects of recent developments and the uncertainty we face regarding structural aspects of the economy, including the natural rate of unemployment and the neutral rate of interest.

Powell has returned time and again to the theme of monetary policy’s “long and variable lags,” and — as in his assessment of r-star — he’s been loath to precisely quantify them. In a nutshell, some people think they’re on the longer side, while others think they’ve become shorter — and Powell won’t decide until concrete evidence presents itself.

This Friday

Given all that, there’s no telling whether the consequences of past tightening are fading or just beginning in earnest, and Powell is likely to see that as a reason for caution. History suggests that he will try to talk tough on inflation but will probably refrain from directly attaching himself to any one view of R-star or explicitly endorsing more rate increases.

Clearly, he’s attuned to the debate and must have privately formed some opinions. But he’s likely to wait for evidence that the inflation trend is turning against him — or alternatively, that clear excesses are forming elsewhere in the economy, as they did in the dot-com and housing bubbles. In the absence of those developments, current trends suggest he can follow Greenspan’s lead and wait for another meeting. If inflation keeps converging on the Fed’s target — however sluggishly — he can afford to wait another meeting yet. And then one more.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 a.m. ET. Click here to register.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.