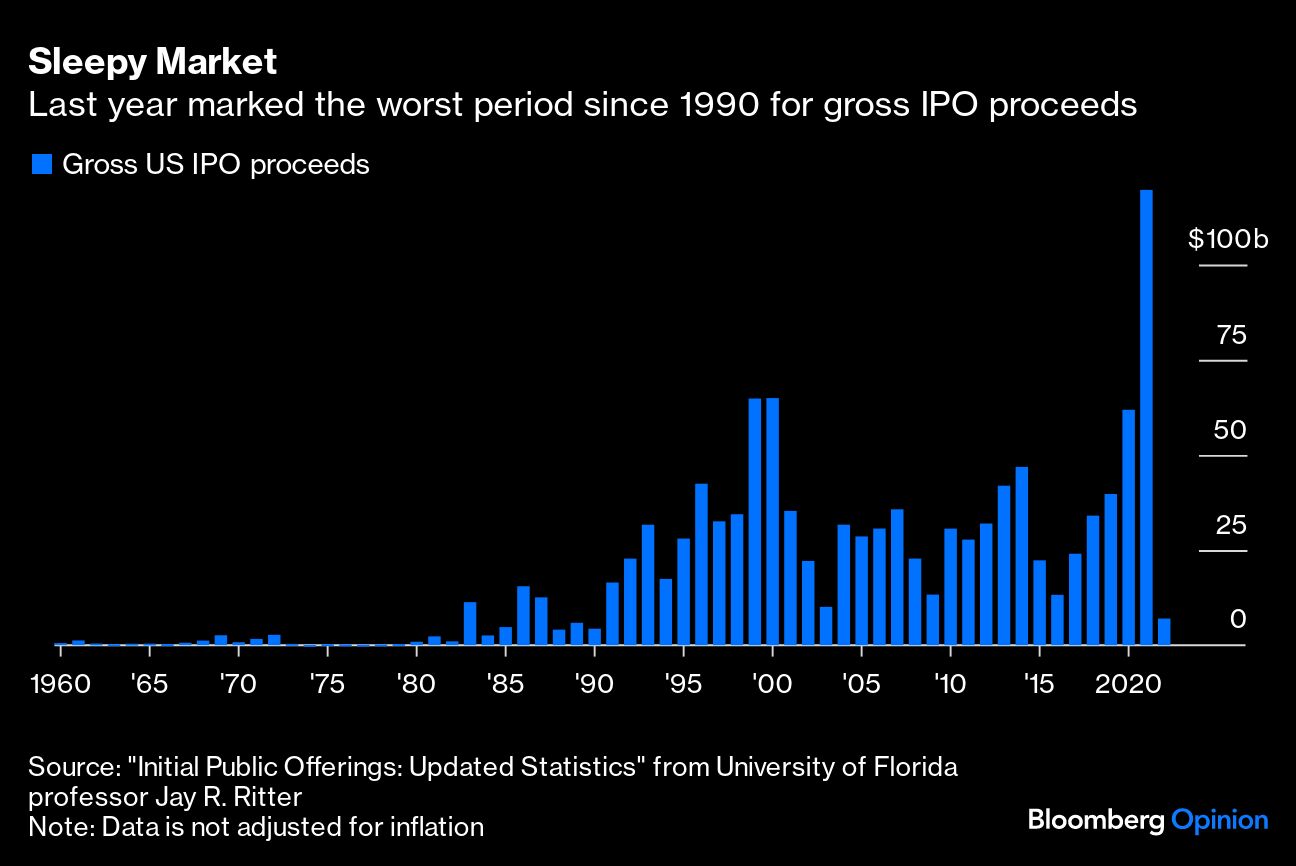

The US market for initial public offerings is finally reopening after the sleepiest stretch in 32 years. Grocery delivery business Instacart, data automation provider Klaviyo and semiconductor designer Arm Holdings Ltd. all filed to go public last week. And if those deals go through smoothly, conventional wisdom holds that others will follow. That’s probably true, but it could take years until the market recaptures its erstwhile sizzle, if ever.

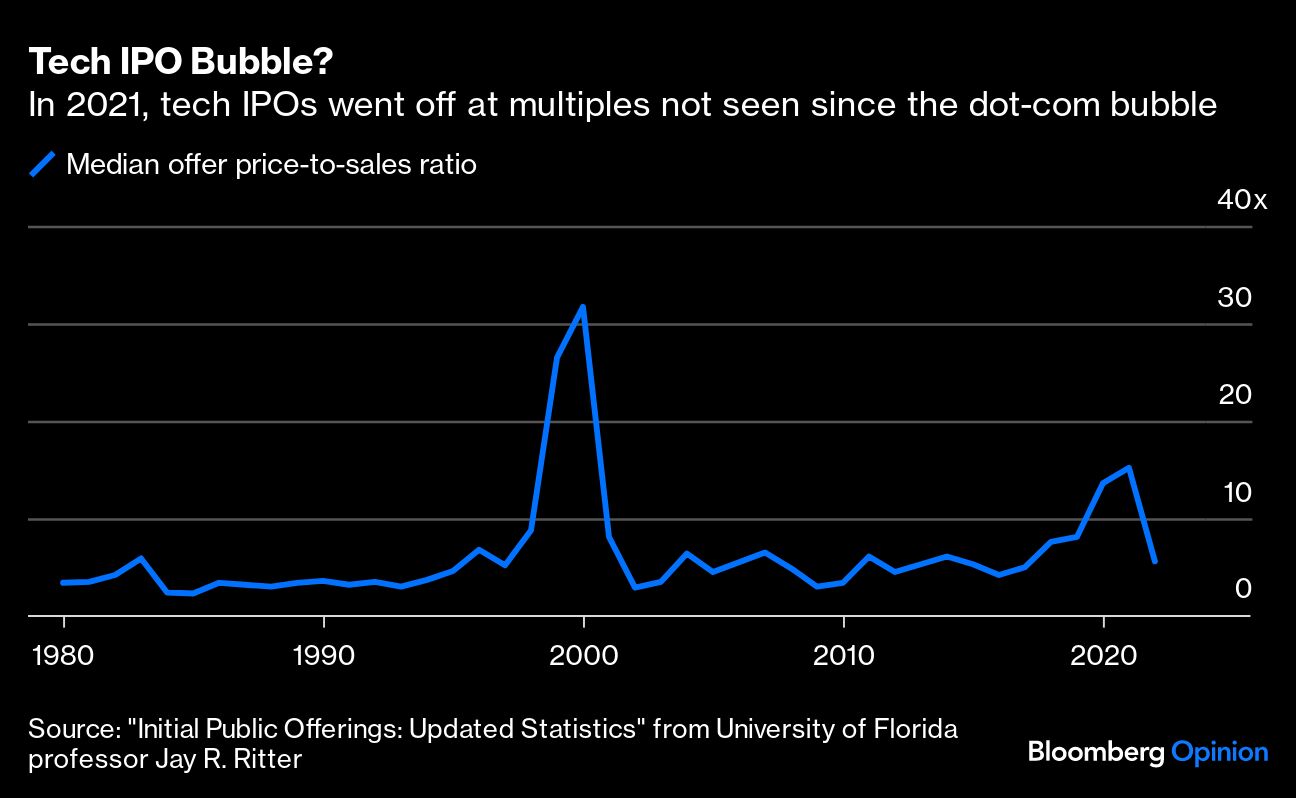

First, consider what University of Florida finance professor Jay Ritter refers to as the market’s unrealistic “anchoring” to the valuations of a couple of years ago. During the peak of the 2021 bull market, companies — and tech firms in particular — carried out IPOs at such extraordinary valuations that it has left issuers with an enduring hangover. Firms are having a hard time accepting that today’s price-sales multiples don’t match the ones that their industry peers received 24 months earlier. Venture capital-backed companies in particular try to avoid so-called down rounds — or raising money at declining valuations — and that’s just what some firms would get if they came to market now.

According to Ritter’s data, the median tech IPO went off at an offer price of 15.2 times sales in 2021, the highest multiple since the dot-com bubble peak in 2000 — a level of frothiness that probably isn’t coming back soon, especially with the Federal Reserve’s policy rate still at a two-decade high. “My reading is that we’re still in a multiyear slow IPO market,” Ritter told me by phone on Monday. If they can, companies would prefer to stay private and perhaps raise more venture capital, where funding can include bells and whistles — usually embedded options — that keep investors happy without formally registering a down round, according to Ritter.

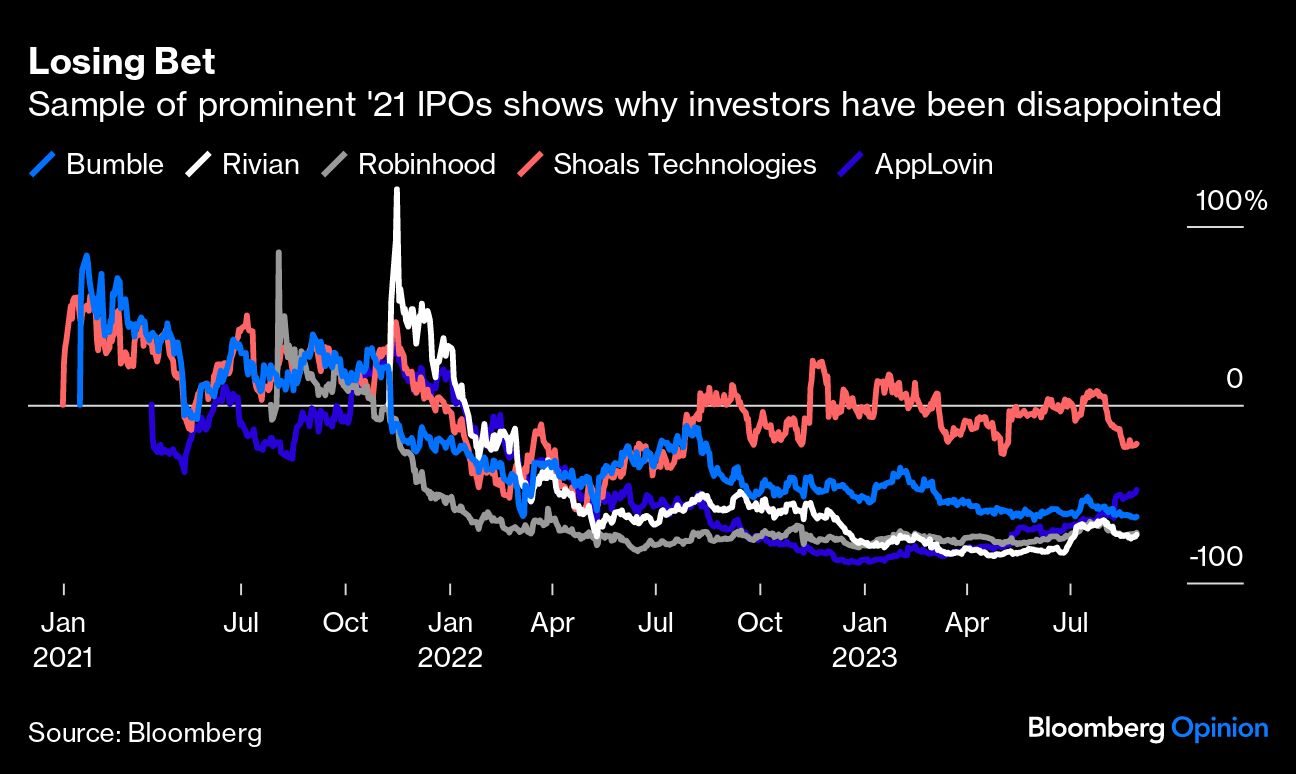

The drought is much more about supply than demand, but IPO bankers may also have some amends to make if they’re going to lure back investors as well. Bankers face the tough task of balancing the interests of their corporate clients (who want to sell on the high side and avoid the perception of “leaving money on the table”) with institutional IPO buyers (who expect positive returns). Lately, they won’t find many satisfied customers among the latter group. From the sample of 2021 US IPOs that raised $500 million or more, the median offer has lost 23% to date, Bloomberg data show.

Second, history provides yet another reason to pump the breaks on IPO optimism. The past five decades have produced a number of pronounced IPO slumps, and all have taken at least a couple of years to give way to recoveries. The inflationary period of the 1970s provides an obvious (if highly imperfect) comparison, given the ostensible macroeconomic similarities. Wild swings in consumer prices and interest rates whiplashed price-earnings multiples, making it that much harder for buyers and sellers of IPOs to arrive at a consensus of what firms were worth. As such, IPO activity was abysmal from about 1974 to 1980. When the market finally reopened, it was a stop-and-go affair. IPO proceeds rebounded sharply in 1981, according to Ritter’s data, but the market cooled again in 1982. In 1983, it finally blasted off in a new boom defined by personal computing enthusiasm, which kept humming through the IPOs of Microsoft Corp., Oracle Corp. and Sun Microsystems in 1986.

IPOs also took time to recover after the dot-com bust and the global financial crisis. In the former, gross proceeds started bouncing back materially after about three years, and it took about two years after the latter.

To be sure, there are key differences between those episodes and today. In the ’70s, it took until July 1980 (seven years) to recapture the January 1973 highs in the S&P 500 Index; from March 2000 to May 2007, it was another seven-year stretch; and from October 2007 to March 2013 it took about five and a half years to climb back to the top. In 2023, by contrast, the market is trading just about 7% below the January 2022 peak after only 20 months. If valuations reinflate further, that would mean that the IPO resurgence probably has some legs.

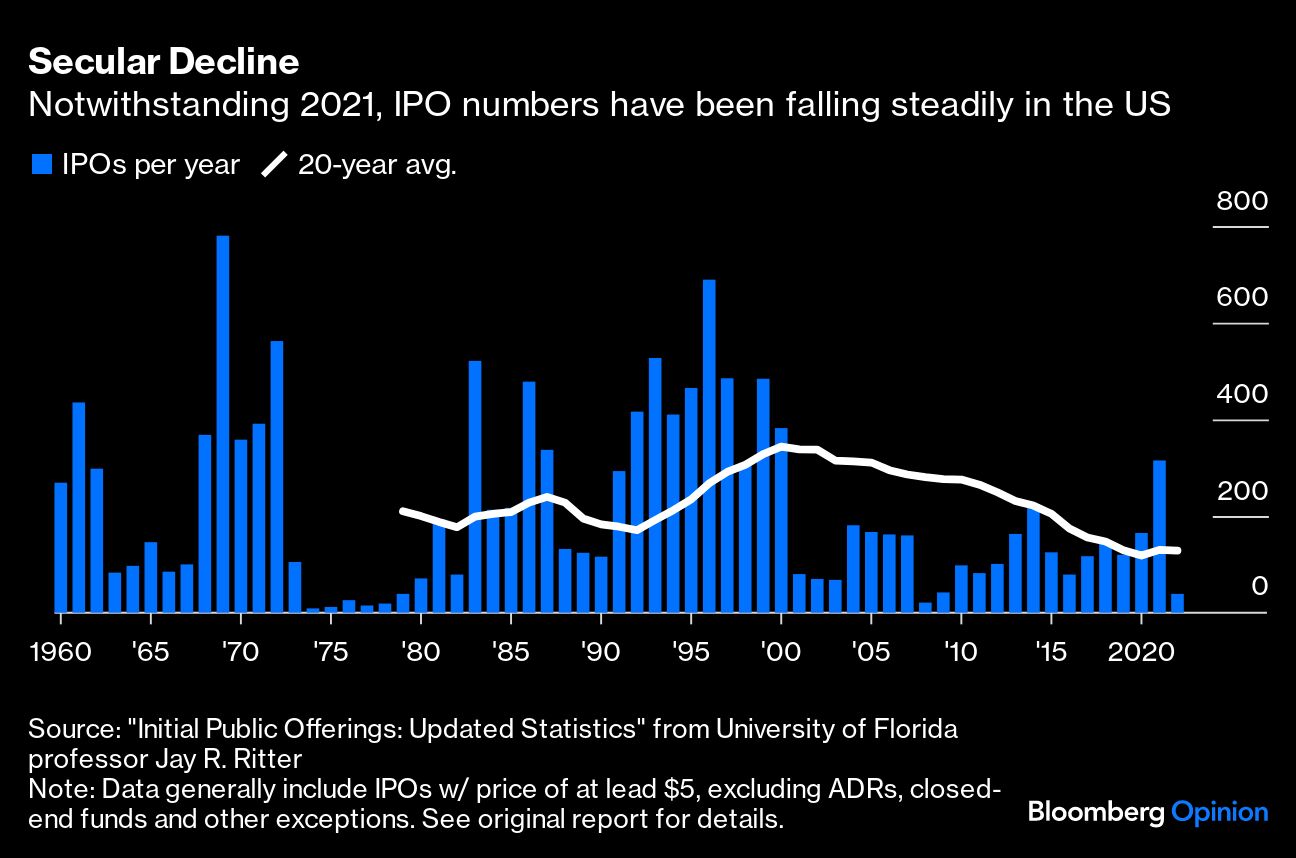

But there’s a third issue that has little to do with the vicissitudes of market prices. Notwithstanding the explosion of activity in 2021, the number of IPOs has been in secular decline since the peak of the dot-com bubble.

As Marshall Lux and Jack Pead found in a Harvard Kennedy School working paper in 2018, the persistent decline appears to be most noteworthy among small IPOs (less than $100 million at 2017 prices) as opposed to medium-sized offerings ($100 million to $500 million) and large-cap ones (which are rare enough that a handful of deals can skew the data in any given year). The probable drivers include the investment industry’s move toward more passive strategies; the growth of venture capital and private equity as public-market alternatives; and the increase of regulatory demands on public companies since the Sarbanes-Oxley Act of 2002. Whatever the precise catalyst, the number of listed US companies has declined sharply since the late 1990s and never recovered.

Granted, there is one scenario in which the IPO market could break out of its enduring slump: Artificial intelligence could, in theory, generate as many exciting new equity offerings as did the dawn of personal computing in the 1980s or the internet boom in the 1990s. In periods of great innovation, the US IPO market will always have an important role to play, and AI could be another such technology — if the hype is to be believed. But until that happens, the US IPO market is likely to struggle to recapture its glory days.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.