Reported inflation has been improving for months, but Federal Reserve policymakers are still understandably worried that it’s a head fake — perhaps none more than Governor Christopher Waller, who has repeatedly referenced the risk of being hoodwinked by the data. His concern is understandable after the events of the past couple years.

Here’s how Waller put it Tuesday in an interview with CNBC’s Steve Liesman on “Squawk Box”:

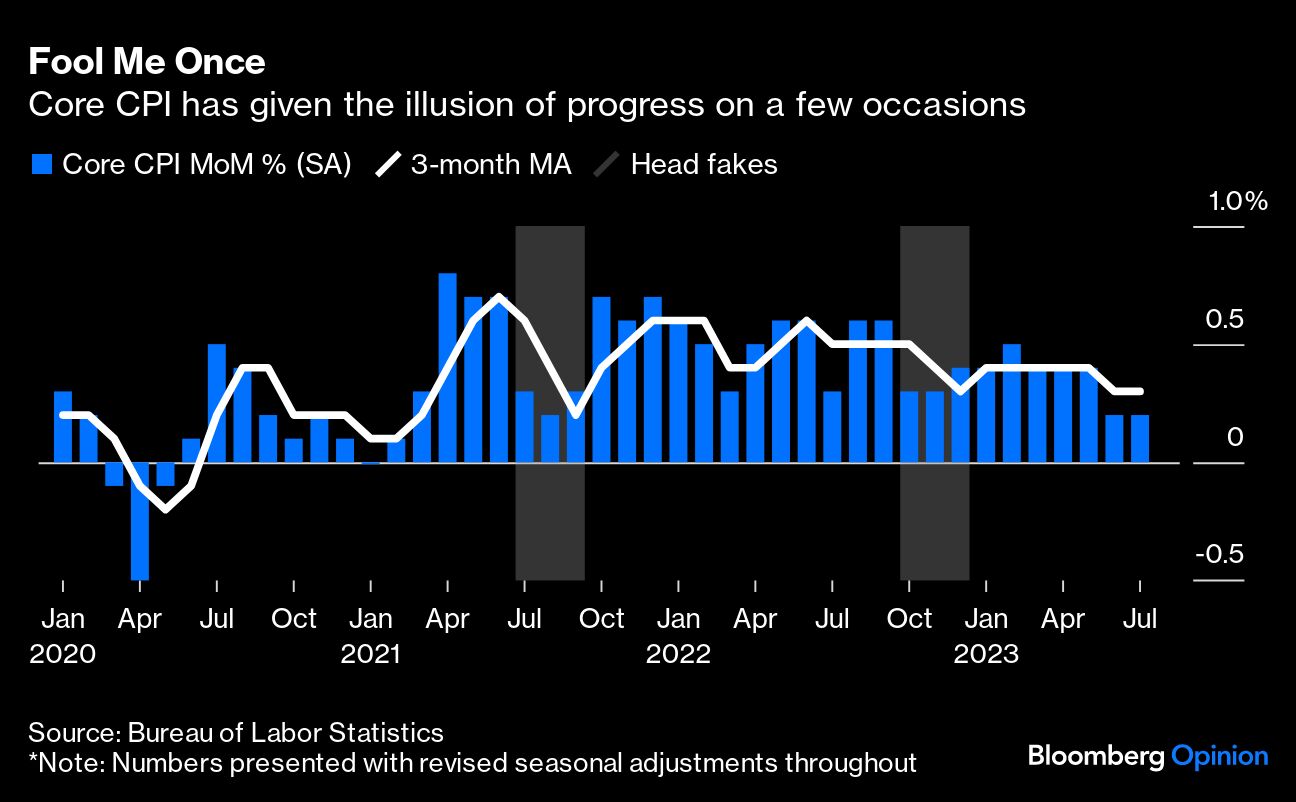

We’ve been burned twice before. In 2021, we saw it coming down and then it shot up. The end of 2022, we saw it coming down, that all got revised away. So I want to be very careful about saying we’ve kind of done the job in inflation until we see a couple of months continuing along this trajectory before I say we’re done doing anything.

Consider the events of 2021. By midyear, many influential voices at the Fed and on Wall Street were already invested in the thesis that the spike in inflation was driven by a narrow set of idiosyncratic factors. Then, in July and August, core inflation surprised economists to the downside, and some members of “team transitory” started to celebrate in what now looks like a classic case of confirmation bias. But by the time of the October report (published in November), the upside surprises to core inflation were back with a vengeance.

Then, as Waller alluded to, there were the quirks of late 2022. By the time of the December 2022 inflation report (published in January), inflation was starting to look as if it had been licked again. Based on the three-month annualized core consumer price index, inflation looked to have fallen all the way to about 3.1%. But about a month later, the revised December figure rose to 4.3% after the Bureau of Labor Statistics published its annual update of seasonal adjustment factors.

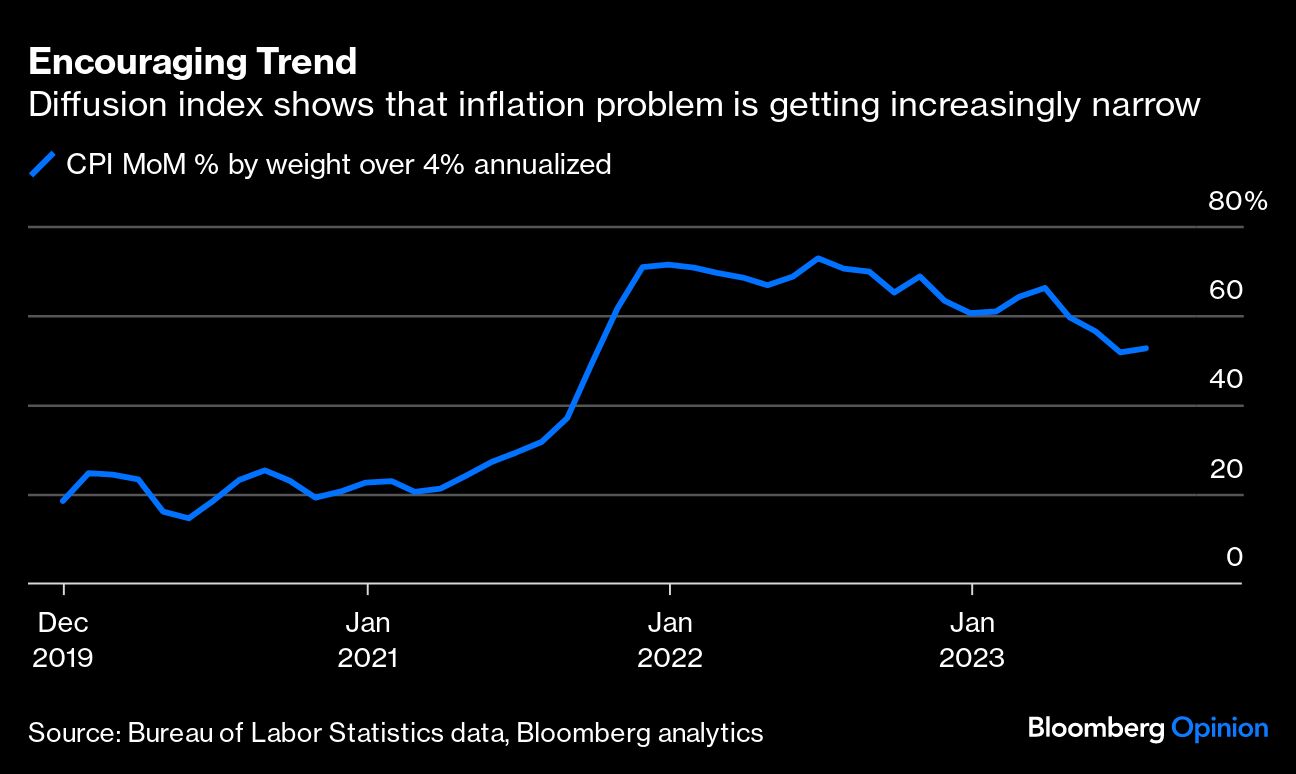

Granted, there are a few reasons to believe that this time is different and that the disinflation of mid-2023 is more durable. During the 2021 head fake, several notable “tells” suggested that inflation was actually worsening, not improving. The breadth of the problem — the number of categories experiencing unusually high inflation — was increasing even as team transitory was celebrating. Wage pressures were also growing notably. This time, the opposite appears to be true; the trend lines are clearly improving. As of July, just 53% of categories by weight were inflating at a greater-than-4% annualized rate, down from a peak of 73% in June 2022. Last month, average hourly earnings rose just 0.2%, the least since February 2022. The disinflation momentum feels somewhat self-sustaining.

Of course, that doesn’t mean that policymakers should take their eye off the ball. The current period may not fit the mold of previous head fakes, but it it does have one red flag: above-trend growth in gross domestic product. After GDP grew at a revised 2.1% annualized pace in the second quarter, the Bloomberg Economics US GDP Nowcast has it expanding at about a 3% pace in the third quarter. In the unusual times since the pandemic began, the relationship between inflation and economic strength has been hard to nail down with any certainty, but growth is clearly a factor that bears watching.

All told the Fed is probably on hold for the foreseeable future, as Waller himself suggested in his latest remarks. “We can just sit there, wait for the data, see if things continue,” he told Liesman on Tuesday. If growth weren’t running so hot, you’d worry that the Fed’s paranoia about another head fake put it at risk of overdoing it and blowing the opportunity for a “soft landing.” But the stunning strength of the economy has given policymakers a certain margin for error as they guard against the risk that flighty data might deceive them yet again.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.