The Federal Reserve’s internal debate about the “neutral” real rate of interest is heating up.

The neutral rate, or r-star, is the inflation-adjusted policy stance that neither stimulates nor restrains the economy. The rate is impossible to observe in real time, yet policymakers have been subtly revising up their estimates of what they think it might be. And some observers are making sensational claims about the significance of the moves.

Undoubtedly, it’s a big deal for monetary policy wonks but probably not for everyone else.

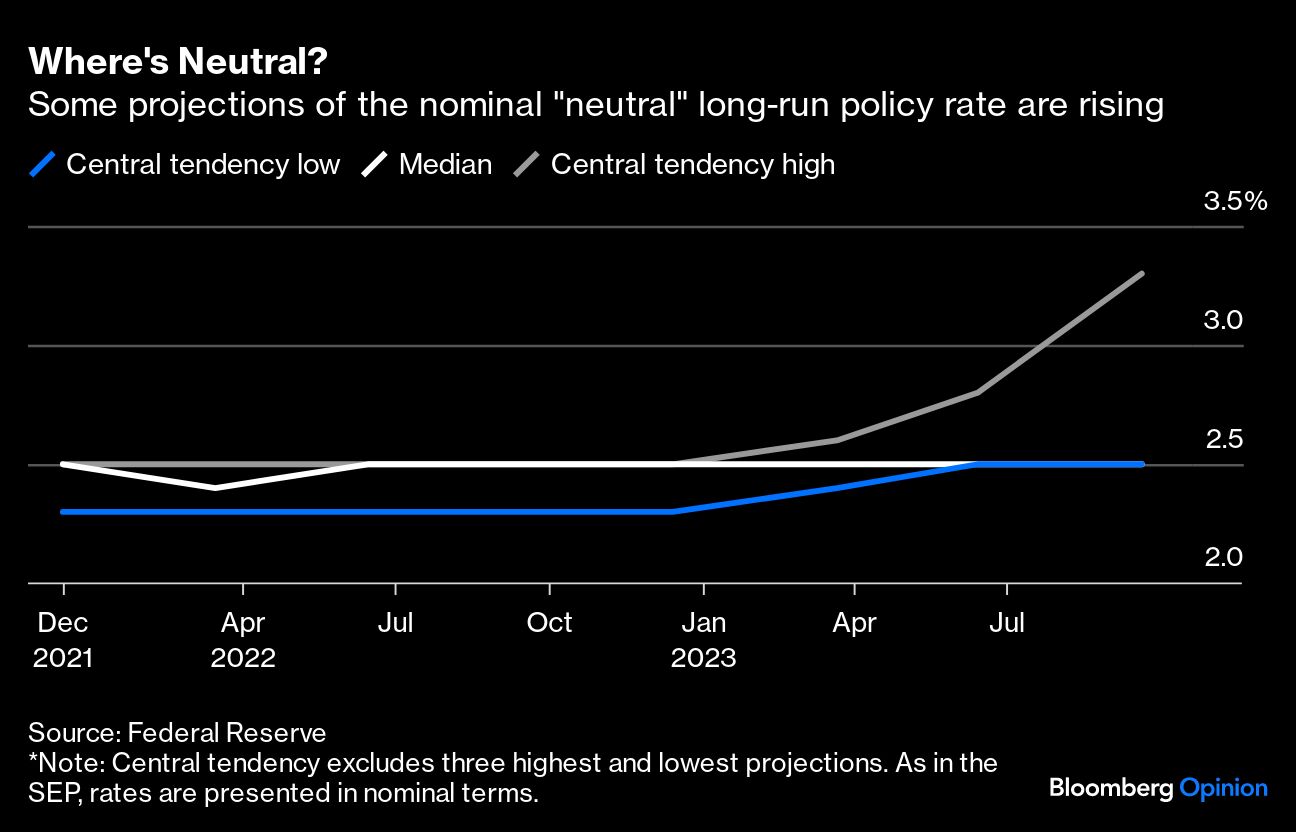

Consider the tea leaves from Wednesday’s monetary policy decision, in which the Fed’s rate-setting committee decided to hold the target range for the federal funds rate steady at 5.25% to 5.5%. As part of the data dump, policymakers updated their Summary of Economic Projections, showing that they thought interest rates would have to stay higher than previously expected in 2024 and 2025. Even more inflammatory, some policymakers revised higher their estimates of long-run rates. Although the median forecast remained unchanged at 2.5% (or 0.5% adjusted for the 2% inflation target), the central tendency now suggests that long-term neutral is about 2.5% to 3.3% in nominal terms, up from 2.5% to 2.8% in June projections and 2.3% to 2.5% at the end of last year.1

If central bankers start to make policy based on those estimates, then bond, stock and mortgage markets will have to pay close attention. But I suspect that we’re relatively far from that moment.

First, Fed Chair Jerome Powell — the most important person on the committee by far — doesn’t seem to place much stock in estimates of neutral. In speeches going back to 2018, he has spelled out his cautiousness when dealing with the macroeconomic “star variables” (including r-star and its close relative, u-star, the natural rate of unemployment). He believes, as Alan Greenspan did during the 1990s, that the path to effective policymaking — and, ideally, a “soft landing” — is to follow the data, not the models. He came back to this theme yet again in his August speech in Jackson Hole and at Wednesday’s press conference.

Asked about neutral by CNBC’s Steve Liesman on Wednesday, Powell responded (emphasis mine):

Ultimately you only know when you get there and by the way the economy reacts. And again that’s another reason why we’re moving carefully now because there are lags here. It may of course be that the neutral rate has risen. You do see people — you don’t see the median moving, but you do see people raising their estimates of the neutral rate.

In other words, Powell is attuned to the debate, but he plans to make policy based on the empirical evidence. At the same time, he’s cognizant that today’s neutral may not be the same as the long-run rate. It’s a moving variable. So while the current economy may require more medicine to bring inflation back to target, that may not necessarily mean that policy rates, bond yields and mortgage rates need necessarily be higher forever, as some bond-market alarmists seem to suggest. Here’s Powell on that latter point:

It’s certainly plausible that the neutral rate is higher than the longer run rate. Remember, what we write down in the SEP is the longer-run rate. It is certainly possible that the neutral rate at this moment is higher than that, and that’s part of the explanation for why the economy has been more resilient than expected.

The Fed’s Summary of Economic Projections doesn’t put names next to its various projections, so it wasn’t immediately clear which Fed policymakers were revising up their estimates. But New York Fed President John Williams — the highly influential policymaker who is among the leading academic voices on r-star — almost certainly isn’t one of them. Earlier this year, a talk by Williams put neutral at around 0.5% in real terms and suggested it could fall going forward.

Some market commentators have suggested that the apparent drift higher in r-star estimates may be behind rising longer-term bond yields, and that may be so. But I suspect that the recent upheaval in 10-year Treasury notes has mostly just rectified a fundamental mispricing that prevailed earlier in the year, when many investors had mistakenly convinced themselves that a recession was imminent and that the Fed would have to slash interest rates in response. Now, economic resilience and effective jawboning have finally convinced the market that policymakers mean what they say — and the adjustment has been somewhat jarring. But given the level of the fed funds rate, long-run rates are not historically high.

It’s understandable, of course, that policymakers are questioning old assumptions in this unusual economy. Output and the labor market have proved stunningly resilient in the face of 525 basis points in policy tightening. Not only is the economy not in a recession, but it’s arguably been running above its potential, a state of affairs that isn’t supposed to be consistent with the fight against inflation. That alone may explain subtle drift in expectations of neutral.

But many strange things have already transpired in this economy. Who thought that the consumer price index would fall from 9.1% to 3.7%, with unemployment still at just 3.8%? So it’s hard to discount the possibility that disinflation will continue apace and that nominal interest rates will ultimately return to around 2.5%, maybe even sooner than expected. In the fog of the inflation war, it’s just impossible to know. So while there’s likely to be much more chin-stroking about “neutral” in the months to come, the rest of us can safely keep our focus on the largely encouraging empirical data, because that’s what Powell will be doing.

1The central tendency excludes the three highest and lowest projections.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin