Since 2012, Puerto Rico has offered investors — primarily mainland Americans — one of the most attractive deals in the world: move to the commonwealth and pay no taxes on interest, dividends or capital gains, all while living on a balmy and culturally vibrant Caribbean island without having to surrender US citizenship. But a decade on, a sweeping Internal Revenue Service investigation has turned up evidence of abuse; struggling Puerto Ricans are growing increasingly frustrated with the obvious favoritism; and you still have to squint to find evidence of trickle-down benefits for the broad economy.

All told, it’s time to consider changes to the program, including less generous terms and more accountability.

Consider how the island got here. Puerto Rico, as a US territory, has a “special” (many would say second-class) relationship with the US mainland. Many of its residents do not have to pay federal income tax. For better or worse, that gives Puerto Rican politicians unique latitude to noodle with tax policy.

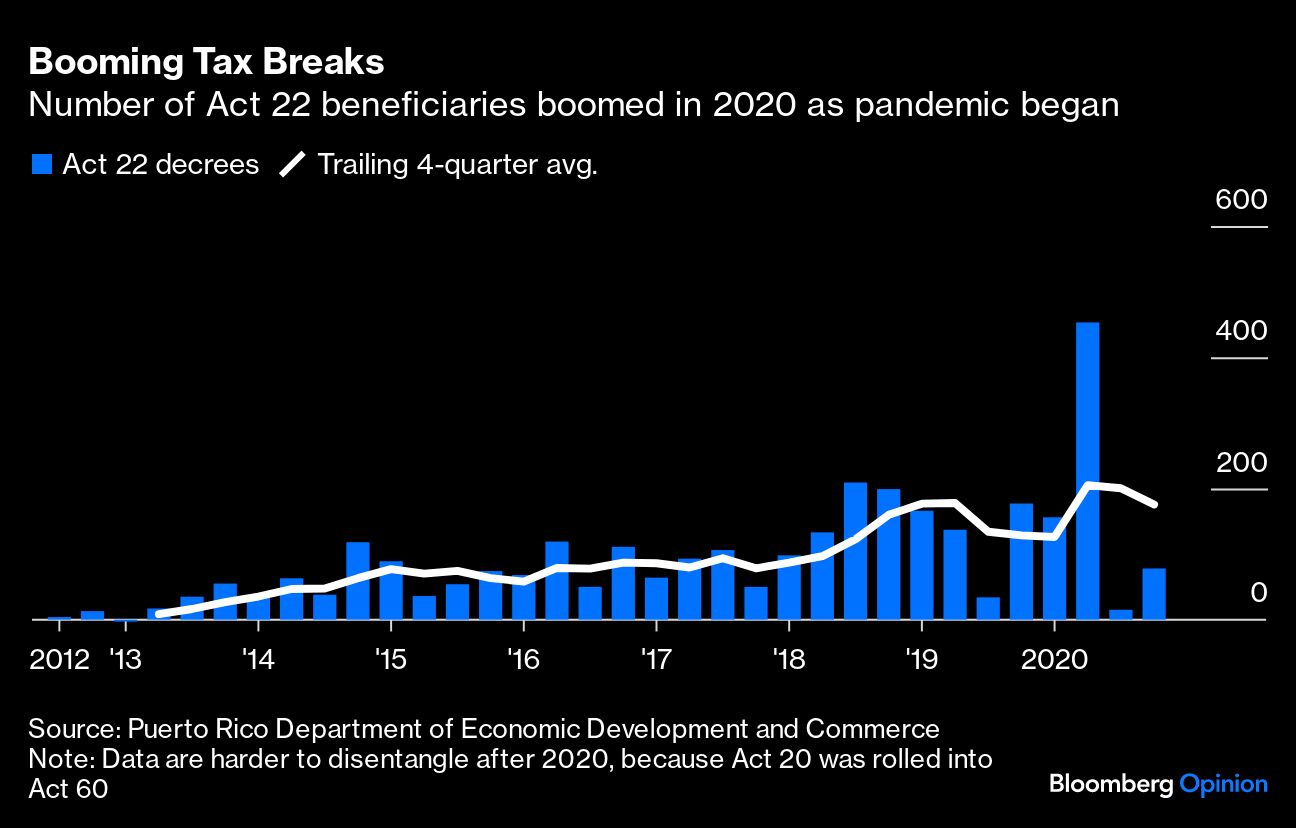

Amid a rapidly shrinking population, an explosion of public debt and a sputtering economy, the passive-income program (Act 22) was rolled out as part of a broader series of tax incentives theoretically intended to spur economic activity. A related program of the same vintage (Act 20) extended a 4% corporate income tax rate to export services firms (i.e., marketing and consulting businesses), while a third (Act 273) brought attractive incentives to banking and financial services firms.

All told, the programs — now combined under the umbrella of Act 60 — have attracted thousands of beneficiaries and fanned the growth of wealthy enclaves, including Dorado Beach, a San Juan area suburb. The presence of the investors — including some particularly loud crypto types — has been a charged and recurring subplot that has continued to bubble up even as the island confronted bankruptcy and Hurricane Maria in 2017; widespread street protests and the resignation of Governor Ricardo Rossello in 2019; and the 2022 arrest of former Governor Wanda Vazquez on corruption charges.

When the Covid-19 pandemic hit in 2020, the migration caught a second wind, helped by the work-from-anywhere revolution and the risk-asset boom that made investors think extra hard about how to maximize their winnings. Crypto and meme stock traders seemed to be making fast money, and many were eager to keep as much of it as possible.

Puerto Rico’s incentives aren’t an entirely free ride. Grantees of the passive-income benefits have to buy a property in Puerto Rico and make annual donations to charities of $10,000. As part of a series of changes in 2020, they also now have to pay $5,000 annual filing fees to the Puerto Rico Department of Economic Development and Commerce as part of their annual reports. So what’s the big issue?

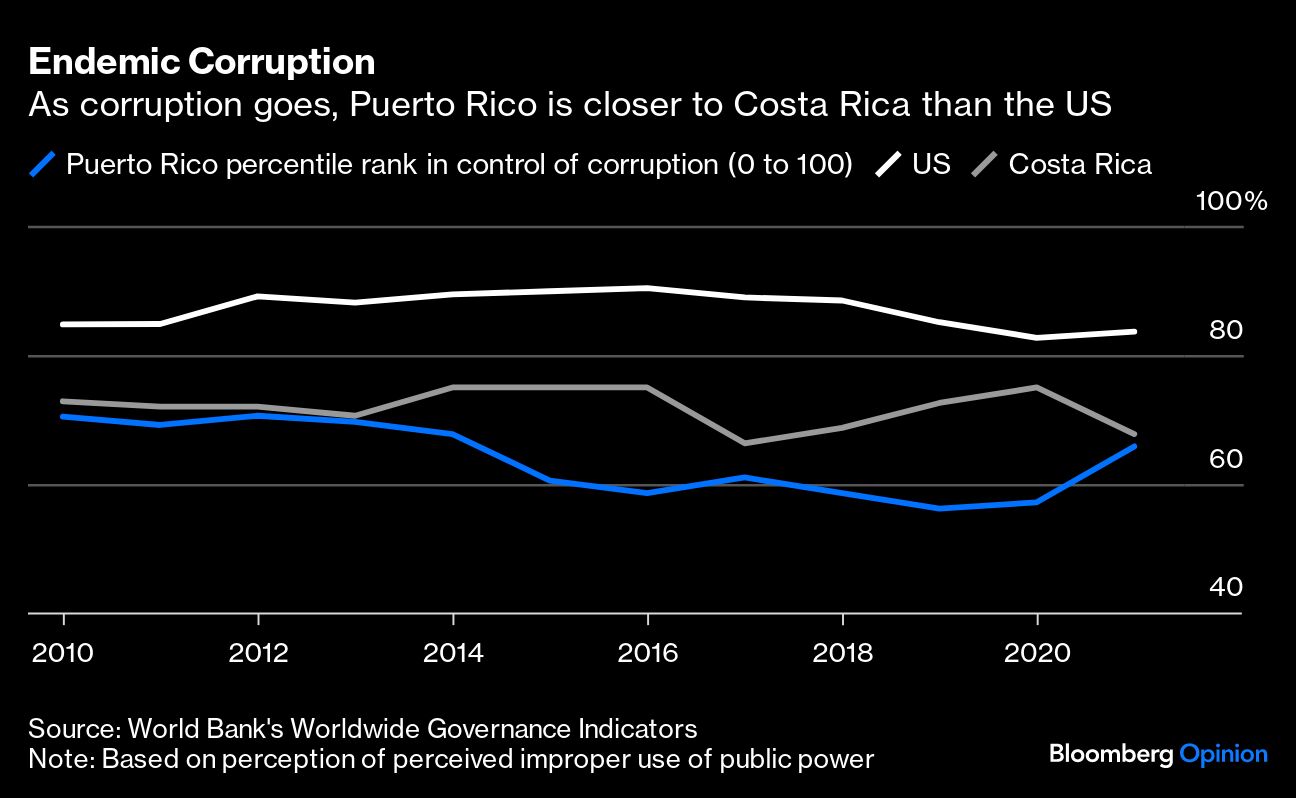

First, it’s clear that the program still has a “bad apple” problem. While most participants abide by the law, the IRS recently identified some 100 “high-income individuals” claiming benefits without meeting the requirements, and it plans to move into criminal investigations for many of them. Bloomberg News reported in July that US prosecutors and IRS agents were studying how much time beneficiaries truly spent in Puerto Rico. Investigators were also looking into the cottage industry that’s developed around the tax incentives, including promoters, attorneys and accountants. While those cases remain the exception, it’s worrisome to think that Puerto Rico — an island that has struggled mightily with corruption to the detriment of its economy and public finances — may be importing deep-pocketed bad actors.

Second, the program has engendered a deep sense of unfairness among a population that — for good reason — often feels left behind by their leaders in both the commonwealth and federal government. At 42%, its poverty rate is twice that of the poorest state (Mississippi), and it has the worst income inequality in the US as measured by the Gini coefficient. Meanwhile, Puerto Ricans pay an ultra-high 11.5% sales and use tax on most goods and services, a regressive policy that bites the poorest households the hardest. Against that backdrop, there’s a certain tone-deafness to a policy that gives extraordinary tax benefits to the passive incomes of some of the island’s richest residents.

Third, the program is forgoing government revenue on an island that, after its bankruptcy, desperately still needs to demonstrate that it’s on a sustainable fiscal trajectory. According to the latest Puerto Rico Tax Expenditures Report, the fiscal cost of Act 22 in forgone revenue is in the billions of dollars since its inception. Proponents would say — quite correctly — that it’s odd to think about it like that, because these people wouldn’t be on the island if not for the program. Still, there’s clearly scope to raise capital gains taxes on future Act 22 participants (prospectively, without spawning an exodus of the current beneficiaries) while still remaining extremely competitive and incentivizing the wealthy to bring their capital to the island.

If the economic benefits were clear, all of that may be worth forgiving, but the evidence of trickle-down good fortune remains relatively scant.

Indeed, it’s hard to separate the program’s modest impact from the mass of confounding factors in the Puerto Rico economy over the past decade, including Hurricane Maria and the federally funded recovery. One pre-Maria study from Jose Caraballo-Cueto, a University of Puerto Rico at Rio Piedras economist, found that the trio of 2012 tax incentives may have created about 34,740 more jobs than would have been the case without them — about 3.3% of total employment in base year 2012.

Of course, research and basic logic suggest that a clear minority of those jobs are related to the passive-income incentive specifically. More logically, the lion’s share have come from the less controversial export-services incentive rolled out at the same time, which — in addition to creating jobs — doesn’t discriminate against existing Puerto Rico residents. Simply put, it strains the imagination to believe that Act 22 itself has done much more than mint a few thousand service jobs such as cooks, gardeners, cleaning crews and, at the higher end of the income spectrum, some accountants and lawyers.

Meanwhile, critics argue that the new arrivals are pushing up the cost of living and gentrifying parts of the island to the detriment of the working class. While those arguments are sometimes hyperbolic — how could several thousand people drive up the cost of housing islandwide for a population of around 3 million? — it’s relatively clear that they’ve contributed to a luxury boom in their enclaves of Dorado and Condado. And so any future analysis of the program’s economic impact needs to consider a broad spectrum of economic indicators, not just job creation or total output.

Several proposals have emerged to start to rectify the situation. First, US Representatives Nydia Velazquez, Alexandria Ocasio-Cortez, Ritchie Torres and Raul Grijalva have asked the Government Accountability Office to assess the tax breaks under Act 60 in their entirety, as NBC News’ Nicole Acevedo wrote in an excellent article about the situation this month. Conducting more research will be an essential step in deepening an understanding of the issue before taking action.

On the island, Governor Pedro Pierluisi last month floated a proposal that would extend many benefits of Act 22 to all Puerto Ricans, but it’s likely to get shot down by the fiscal babysitters that Congress installed as part of the commonwealth’s bankruptcy. The only merit of the proposal is that it would correct a fundamental inequity in the tax code. But in addition to being dead on arrival and sending the wrong message about fiscal responsibility, the proposal wouldn’t make a big difference in regular Puerto Ricans’ finances because many Puerto Rican households simply don’t have much in capital gains or investment income.

Ultimately, the most prudent solution — given the available income — is to seriously consider raising the capital gains rate. Caraballo-Cueto, the University of Puerto Rico economist, has suggested raising the capital gains tax rate to 5% (conditioned on job-creation and local-investment requirements). That would still be an attractive rate when compared with the 20% federal long-term capital gains tax for top earners in the US mainland, and it could be implemented prospectively to avoid any negative economic fallout — such as existing beneficiaries leaving en masse.

At the same time, Puerto Rico must prove that it can more effectively police the program to weed out the bad actors. While that won’t solve the commonwealth’s deeper economic problems, it will at least help ensure that the island receives some fiscal benefit from a program that has rubbed salt in the wounds of the island’s working-class residents.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.