South Florida has a reputation as a leading indicator of housing market trouble, so the Cassandras are understandably watching the region closely these days. Not only was it a canary in the coal mine of the 2000s real estate boom and bust, but its rents and home prices are coming off a pandemic-era sizzle that has, once again, severely pressured affordability. If the US enters a recession and unemployment rises, South Florida looks as vulnerable as anywhere in the country. But short of that, there are also a few reasons for cautious optimism.

Let’s get the ominous stuff out of the way first.

A quick look at multifamily rental data from CoStar shows that the Miami area (defined here as essentially Miami-Dade County) is on the verge of a jolt of new supply. About 32,700 multifamily rental units are under construction, equal to about 17.7% of current inventory, many of them at the top end of the market.

In Austin, Texas, for example, the pandemic run-up in prices stoked a significant supply response from developers that got going in earnest in 2021, and asking rents started to retreat about a year later. Miami rents have been resilient for longer, but the area’s new-construction schedule is running about 12 months behind Austin’s. In other words, it’s conceivable that the price impact from the building boom still looms.

The other reason for Miami's pessimism concerns the area’s history. South Florida has been subject to booms and busts since the original land boom of the 1920s, which collapsed late in the decade, foreshadowing the Great Depression. Try as they may, the area’s development officials haven’t totally managed to tame the speculative, extremely cyclical nature of the region’s economy.

It’s still heavily reliant on tourism, hype-driven businesses (see: Miami’s association with crypto) and momentum itself. So many Miami real estate speculators base their decision to invest on the observation that prices have climbed a lot and will continue to do so. Ending that cycle means populating the city center with hardier, serious businesses from a diverse set of industries. In 2022, the region landed its biggest fish yet in the arrival of billionaire Ken Griffin’s Citadel and Citadel Securities. But Miami will need many more Griffins to create a more mature local economy and real estate market.

Of course, there are a number of reasons to believe that history doesn’t have to repeat itself. Among wealthy new arrivals, it’s become an increasingly attractive lifestyle destination in a state with no income taxes and — for the rich coming from abroad — a key place to park cash offshore in dollars as a hedge against home-currency volatility. It also has a deeply embedded and hard to replicate immigrant community that attracts immigrants who speak Spanish, Portuguese and Haitian Creole at all points of the income spectrum. Even if they ultimately move to other US cities, Miami is a key weigh station en route to life in America.

Certainly, Miami still has relatively low median family incomes, which makes rent-to-income ratios look untenable, fueling a lot of the Miami “bubble” coverage. Yet that may be an oversimplication. “What you need to look at is the income of the households that are moving into the market as opposed to the households that are there,” Jay Lybik, CoStar’s National Director of Multifamily Analytics, told me by phone on Tuesday. Indeed, while the median family income is among the lowest in large cities, the trajectory suggests that Miami is making some headway toward closing that gap.

Lastly, rents and home prices benefit from the sense that supply is ultimately finite. For all the concerns about the near-term jolt in new apartment units, Miami developers will never be able to overbuild to the extent that others have in Texas and the rest of the Sun Belt because the land simply isn’t available to do so. Miami-Dade County is sandwiched between the Atlantic Ocean and the Everglades, making it — in some ways — somewhat more like San Francisco than Austin. My colleague Justin Fox has written about this phenomenon here.

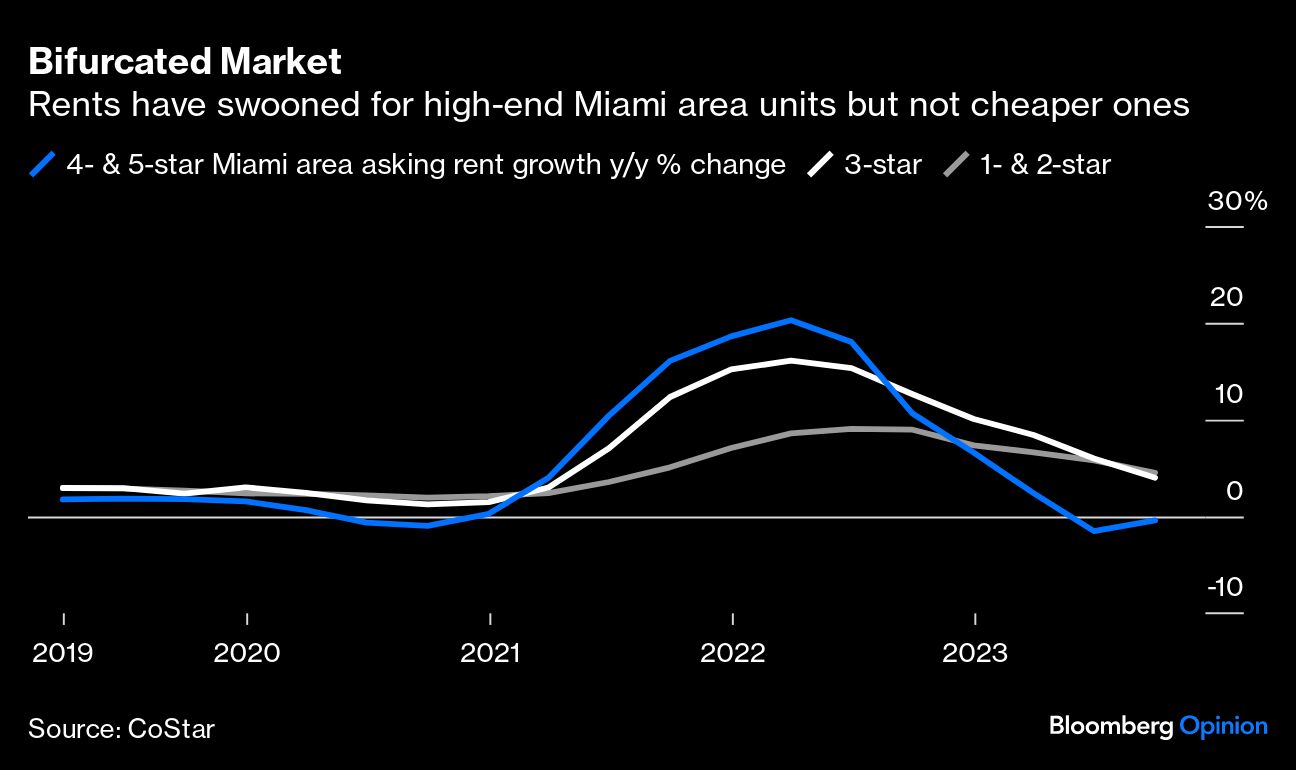

One possible outcome is that the Miami market could become increasingly bifurcated. In fact, that already appears to be happening. The high-end (four- and five-star) rental market — where much of the new construction is taking place — is already experiencing price declines, even as less expensive inventory has generally hung tough. For its part, CoStar projects Miami’s rent growth will remain extremely modest for the next several quarters before reaccelerating in 2024 — and that’s conditioned on a mild recession scenario. History suggests that the pessimists are right to have their guard up, but a lot probably needs to go wrong in the macroeconomy to bring another Miami crash to fruition.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Real Estate Topics >