Lately, Federal Reserve officials have been paying greater attention to financial conditions – that is, to the influence that market phenomena such as stock prices, bond yields and housing prices have on economic activity, above and beyond the effect of the short-term interest rates that the central bank controls directly.

This is a welcome development for monetary policy — and for me personally.

Nearly 25 years ago, when I was chief US economist at Goldman Sachs, my colleague Jan Hatzius and I created a financial conditions index as a tool for assessing the economic outlook and the appropriateness of the Fed’s monetary policy stance. While its construction has evolved considerably since then, the conceptual framework remains intact. Over the years, many others developed comparable indexes. This summer, the Fed introduced a new one of its own.

Such indicators are crucial, because monetary policy does not operate exclusively through short-term interest rates, particularly in the US. A lot of financial intermediation happens outside the traditional banking system. Home purchases are financed mainly by long-term fixed-rate mortgages that are packaged into securities and sold to investors. Companies raise money in capital markets, too. So various market prices, from risky companies’ cost of borrowing to the dollar’s exchange rate, matter for the economic outlook.

Financial conditions wouldn’t merit much attention on their own if they always moved in lockstep with the Fed’s short-term interest-rate target. They don’t. The stock market can rally or fall independent of short-term rates. The dollar’s value can change depending on economic activity abroad and how that affects monetary policy elsewhere. Distress in the banking system can tighten financial conditions independently, as happened when a group of regional US lenders ran into trouble this spring.

In the US, the linkage between financial conditions and short-term interest rates was tight through the 1970s and early 1980s, in part because of the way the monetary policy was implemented. Prior to 1994, the Fed didn’t even announce interest-rate changes. Market participants inferred what had happened from the central bank’s open market operations and how this affected the level of the federal funds rate.

Since then, the relationship has loosened a lot. The role of the non-bank financial sector has grown, and monetary policy has become much more transparent, with public statements, news conferences and Fed forecasts. Markets shift based on what participants expect the Fed to do, so financial conditions move faster and well before the central bank acts. This shortens the lags between changes in monetary policy and the impact on real economic activity.

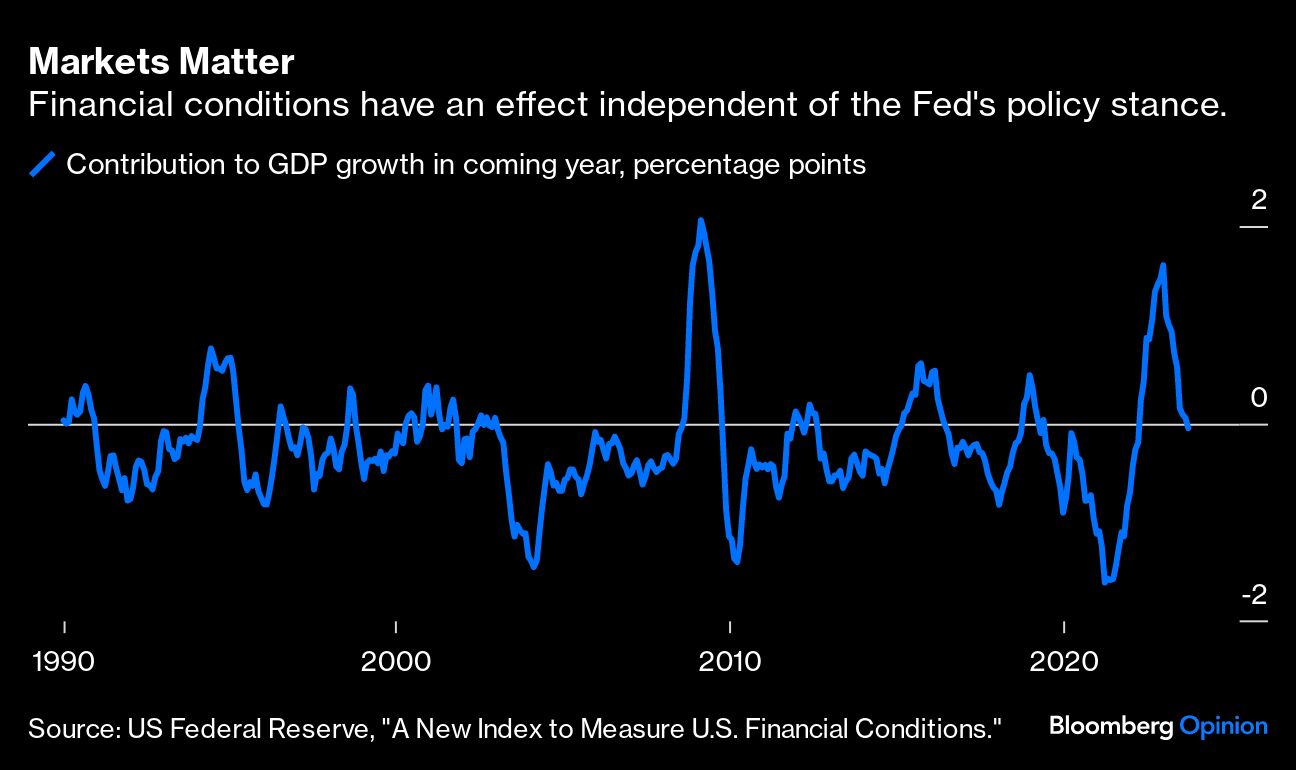

The shorter lags are visible in the Fed’s new financial conditions index. The version that uses a one-year lookback window hit its point of greatest restraint last December, long before the federal funds rate reached its current peak. In contrast, the index was around zero at the end of September, indicating that financial conditions were providing no added impetus, up or down, to economic activity.

That said, there are a few caveats. For one, changes in financial conditions still affect the economy with a considerable lag, which can differ depending on what’s changing. Mortgage rates, for example, affect housing activity relatively quickly, while equity prices and the dollar’s exchange rate take much longer to be fully felt.

Second, the drivers of changes in financial conditions matter. In the US, for example, long-term interest rates have increased. If this means only that bond investors are demanding more of a premium to lend for longer, then financial conditions have tightened, allowing the Fed to be less aggressive in raising short-term rates (as recent remarks by Dallas Fed President Lorie Logan and Chair Jay Powell have strongly implied). By contrast, if it means that inflation expectations have increased, or that the “neutral” federal funds rate has risen, then it justifies further tightening by the Fed.

Third, simple financial conditions indexes are necessarily incomplete. Sometimes they don’t fully capture economic shocks that make credit less available. Their accuracy then depends on the extent to which the omitted variables move in sync with those that are included. If they do, then the indexes should still provide a more reliable guide than just focusing on the path of short-term rates.

I’m glad to see financial conditions finally getting the attention that they deserve. They should be viewed not as all-encompassing but as one tool to help assess the stance of monetary policy and its likely evolution. To that end, they’re more valuable than mechanical guides such as the Taylor rule, which aren’t forward-looking and don’t consider how financial market developments influence the economic outlook and monetary policy.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Bill Dudley