Stocks and bonds are moving in lockstep once again, triggering more agita about what it all means. Before we get carried away anew with declarations about how “the investing world is forever changing,” it’s worth remembering how fluid the relationship has proved over the past couple of years — and how another twist is always just around the corner.

To review: 10-year Treasury notes were negatively — or minimally — correlated with the S&P 500 Index for most of the 21st century, and the investing public had generally accepted that some mix of stocks and bonds was the optimal way to manage risk. Then last year, correlations surged into meaningfully positive territory (both went down simultaneously), tanking the storied 60/40 portfolio (60% stocks, 40% bonds) and leading many observers to question the conventional wisdom about portfolio construction.

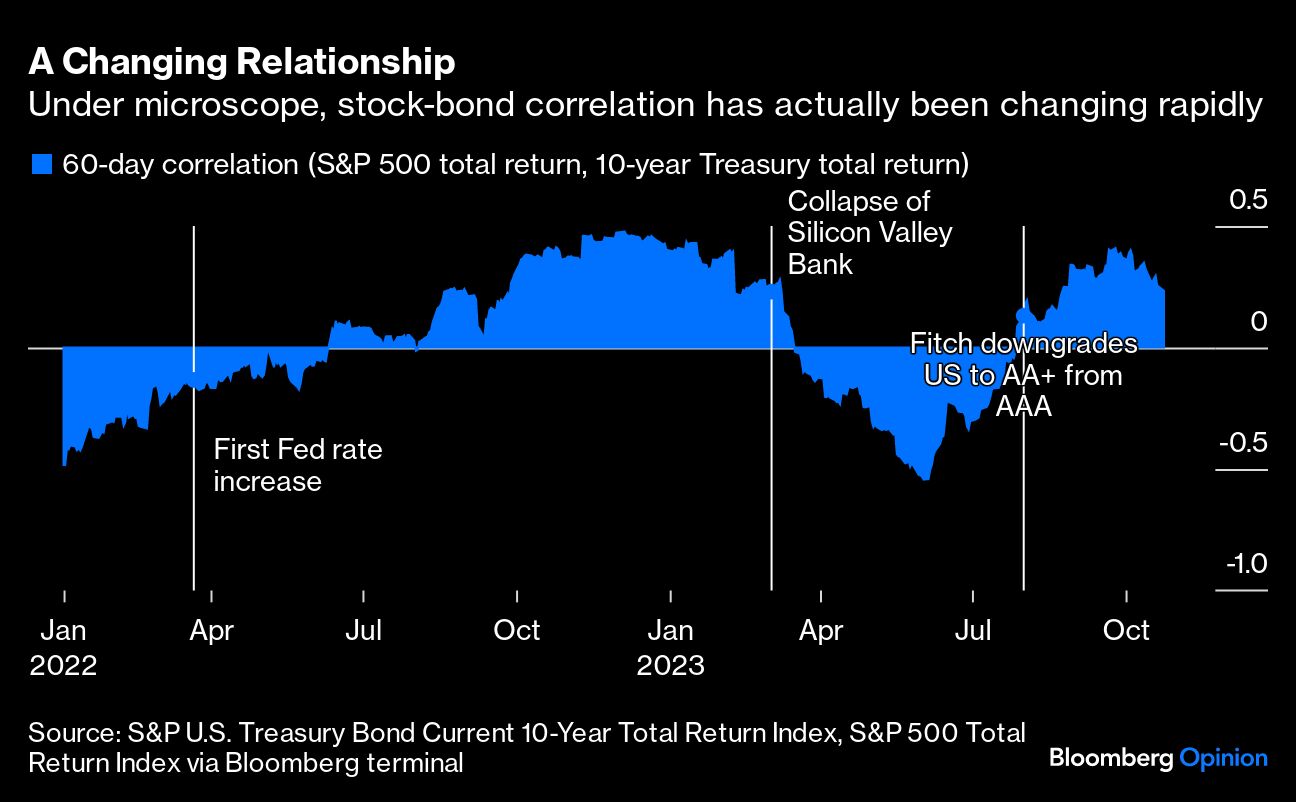

Studies of stock-bond correlations often use slow-moving multi-year look-back windows to analyze the relationship between the two asset classes. Here I’ve used rolling 60-day periods to put the data under a microscope, revealing that the relationship has been ever-evolving of late and is not as sticky as it seems. Consider this timeline:

- In early 2022, faced with the worst inflation in 40 years, Fed policymakers started strongly telegraphing plans for policy rate increases, triggering a decline in stocks and bonds alike that lasted for about nine months from peak to trough. Short-term correlations surged.

- In early March 2023, markets began to focus on the potential economic fallout of the regional bank crisis. Risk assets tanked, but bond speculators thought central banks might start cutting interest rates to rescue the economy from the recession that they thought would follow. Correlations went sharply negative.

- After the regional bank jitters faded without a recession, markets quickly hurried to price out the emergency rate cuts they’d dreamed up, but another story had taken hold in the stock market: the promise of artificial intelligence. Between April and July, risk appetite surged, and speculation about higher interest rates faded as a driver of equities. Correlations stayed negative.

- Finally, around the start of August, Fitch Ratings downgraded the US to AA+ from AAA just as a new inflation narrative was taking hold in markets: Interest rates may have to stay relatively high for the foreseeable future because of the threat of persistent supply shocks and higher deficits, among other theories. Investors’ focus on AI also faded in the absence of concrete new developments to fuel the narrative. Correlations went positive again.

Unsurprisingly, investors and commentators have begun another round of chin-stroking over the implications — this time including Federal Reserve Chair Jerome Powell and Federal Reserve Bank of Dallas President Lorie Logan. What’s going on here and where will it leave us?

One interpretation is: We shouldn’t be overly eager to declare that a sea change has occurred. First, correlations don’t have to be negative to provide diversification benefits; they just have to stay well below 1. Second, if you don’t like what you see, just wait awhile longer and the relationship could change yet again. The recent past tells us little about the near future (and may well mislead us about where we are heading).

There is, however, a chance that this whole thing could feed into a vicious cycle, and that’s the threat that Chair Powell seemed to allude to in his recent remarks on the subject at the Economic Club of New York. Here’s how Powell put it in an on-stage interview with Bloomberg Television’s David Westin (emphasis mine):

Another one you hear very often is the changing correlation between bonds and equities. If we’re going forward – if we’re going forward – into a world of more supply shocks rather than demand shocks that could make bonds a less attractive hedge to equities and therefore you need to be paid more to own bonds, and therefore the term premium goes up.

Moments later, he also considered the possibility that the shift “could be” a long-term phenomenon, but subsequently cautioned: “I don’t think we know.”

The logic here is a bit circular, but I make sense of it thusly: Bond-stock correlations initially turned positive because bond prices fell sharply, but now that correlations are positive — and investors generally see that as detracting from diversification efforts — bonds may fall even more. Such a change in investor psychology doesn’t happen overnight, but bond-stock correlations have been positive more often than not over the past year, and the longer that endures, the more likely it is to become entrenched in investor psychology.

In other words, when bond markets are already under pressure — often due to inflation expectations or, relatedly, federal budget and debt supply concerns — correlation dynamics exacerbate the fallout. My Bloomberg colleague Steve Hou, a senior quantitative researcher, found in his doctoral study that while increases in Treasury bond supply boost bond risk premia, positively correlated stock and bond markets make the situation worse because bonds lose their value as hedges and investors demand greater compensation to own them. “Your borrowing needs are going up at the same time that your lender is getting stingier,” Hou told me Tuesday.

But correlation isn’t increasing in a vacuum — it is a consequence of inflation.

Correlation was generally positive in the three decades through the end of the 20th century, and it went negative only when inflation receded as a driver of market narratives. For most of the 2000s and 2010s, central bankers were able to keep policy rates low and stable, and bonds were frequently treated as “flight-to-safety” assets, rallying in the face of growth concerns that dragged equity markets lower. If you expect inflation expectations to stay elevated for the foreseeable future, then, sure, you should prepare for bonds to move frequently in tandem with equities.

For all the uncertainty about the past couple of years, there’s still room to believe that we’re heading for a more positive outcome.

Reported inflation has been consistently moderating for the past year, and forecasts now project that year-over-year inflation — as measured by the core personal consumption expenditures deflator — probably moderated to about 3.7% in September. If you think (as I mostly do) that inflation is a fading aberration, then you must also think the same of the positive stock-bond relationship — and, thus, the consternation about the place of bonds in portfolios is overdone. Remember, bonds will continue to act as diversifiers so long as the positive correlation doesn’t get too close to 1.

Whatever the case, markets are likely to deliver at least a few more twists and turns before the great correlation debate is finally settled. That’s the one clear lesson of the past year and change.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin