To have a shot at taming inflation, the Federal Reserve is intent on tightening financial conditions across the economy. But they haven’t made much of a dent in corporate America yet.

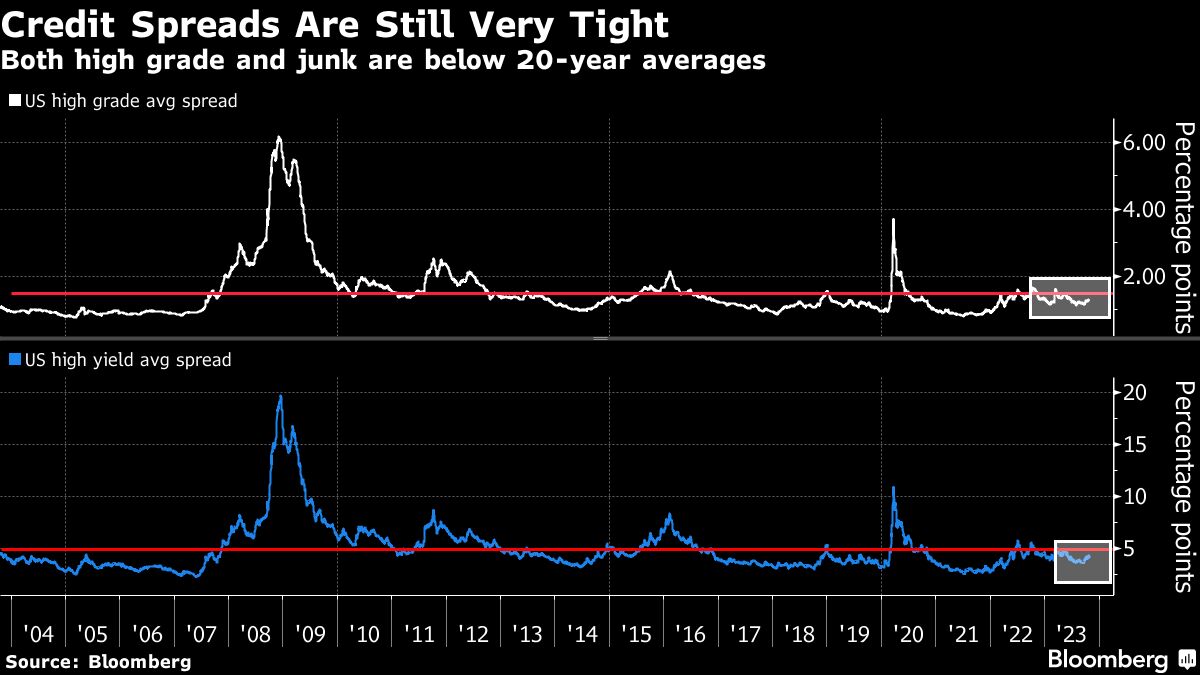

The extra yield investors demand for risk in the US investment-grade and high-yield bond markets has remained below their 20-year averages and well under levels seen during historical times of stress in the economy. Borrowing remains robust, one measure of credit quality is improving at a record rate and recent earnings reports for some of the nation’s most indebted companies have come in stronger than expected.

How that’s all happening after the Fed increased its benchmark rate at the fastest pace in four decades — and to the highest level in 22 years — is nothing short of remarkable. And it once again raises the question if policymakers have hiked interest rates to what they deem a “sufficiently restrictive” level, or held them there for long enough.

“If you had told me two years ago that the Fed would hike by this much in a short time, I would have said that they would leave dead bodies littered across the corporate credit landscape,” said former Fed Governor Jeremy Stein, who’s now a professor at Harvard University. “I really don’t have any good story to explain why things have instead been so resilient.”

Since interest-rate hikes can take awhile to impact the real economy, Fed officials watch financial conditions closely as real-time gauges for how their policy is working. So far, that’s really just affected Treasury yields — which are trading around the highest levels since the financial crisis — while equity and oil prices have remained largely resilient.

The ebullience of credit conditions gets to the heart of the debate on Wall Street right now. Will the Fed have to increase rates more, or can it simply hold around current levels and give policy time to seep into strong household and corporate balance sheets?

“There’s a lot of uncertainty around lags,” Fed Chair Jerome Powell said at an event earlier this month. “One of the reasons why we have slowed down significantly this year is to give monetary policy time to work.”

Powell and his colleagues are expected to hold rates steady for a second consecutive gathering when they meet this week, and investors will parse for clues as to whether another hike may still be in store. Some Fed officials contend they aren’t done hiking yet given the recent strength of economic data — hiring remains robust, consumer spending is still supporting growth and inflation is well above target.

Policymakers appear willing to wait and see if the lagging effects of tightening begin to curb credit conditions and the economy more broadly. But the longer they keep rates steady, the more it might convince investors that they’re done altogether, which risks easing financial conditions further and stoking growth.

“The bite is coming. It is going to require a bit more patience on the part of the Fed,” said Conrad DeQuadros, senior economic advisor at Brean Capital LLC, which is calling for a recession next year. “Corporate spreads are extremely tight and I think they are going to go wider if we are right on the economic outlook in 2024.”

For now, credit hasn’t wavered. The resiliency of the economy — and particularly the American consumer — is still propping up earnings for big corporate issuers like AT&T Inc. and Amazon.com Inc. Defaults have largely been well telegraphed among companies that were already struggling, and the riskiest credit in the triple-C rated bucket is outperforming the rest of the market this year.

“Spreads are contained because defaults are low and balance sheets are healthy,” said Tim Leary, senior portfolio manager at RBC Global Asset Management. He also noted the strength of the US consumer and how credit quality, especially in high yield, has improved in the past five to 10 years.

Investment-grade borrowers have issued more than $1 trillion so far this year, roughly in line with last year’s pace, while high-yield sales have already eclipsed 2022’s volume. There were 12 high-grade issuers in the market Monday, marking the busiest day for issuance in nearly two months.

Perhaps even more startling is how much corporate balance sheets have improved. The amount of debt upgraded from triple B — the lowest rating tier of investment grade — has set a record this year, with $134 billion of debt boosted into the single-A index, according to Barclays Plc.

“We expect a continuation of the BBB to single-A transition, as inflation and monetary policy tightening has yet to crack the consumer and, therefore, company balance sheets,” strategists led by Dominique Toublan said in a recent note. “This has delayed the widely expected growth slowdown and has put wind in the sails of corporate earnings, which should support more upgrades in the near term.”

To be sure, there are some scattered signs of emerging stress in credit — a slew of regional banks collapsed earlier this year, while more recently, defaults are ticking up, consumers are falling behind on auto loans and blue-chip company fundamentals are weakening. Small businesses are increasingly pessimistic about the outlook for credit conditions, and consumer delinquencies, while low, are on the rise.

It’s a tightrope for the Fed to walk. Officials now talk about two-sided risks — one being raising the rate too high and tipping the economy into recession, versus not doing enough and letting inflation linger.

“They do not want the market to ease in their face,” said Robert Tipp, chief investment strategist for PGIM Fixed Income. “You are around an okay level of rates, maybe you have more work to do, maybe you don’t. You need more time to watch and wait.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.