Small businesses1 account for close to half of US private sector employment, so there’s always considerable focus on their prospects, especially during periods of rising interest rates and contracting credit. Smaller firms have fewer financing options than larger peers, and they’re much more exposed to variable-rate loans, making them something of a canary in the coal mine. No doubt, the recent run-up in interest rates makes 2024 a year to watch, but America’s smallest employers mostly seem to be tolerating the headwinds and can continue to tread water for awhile longer — just not indefinitely.

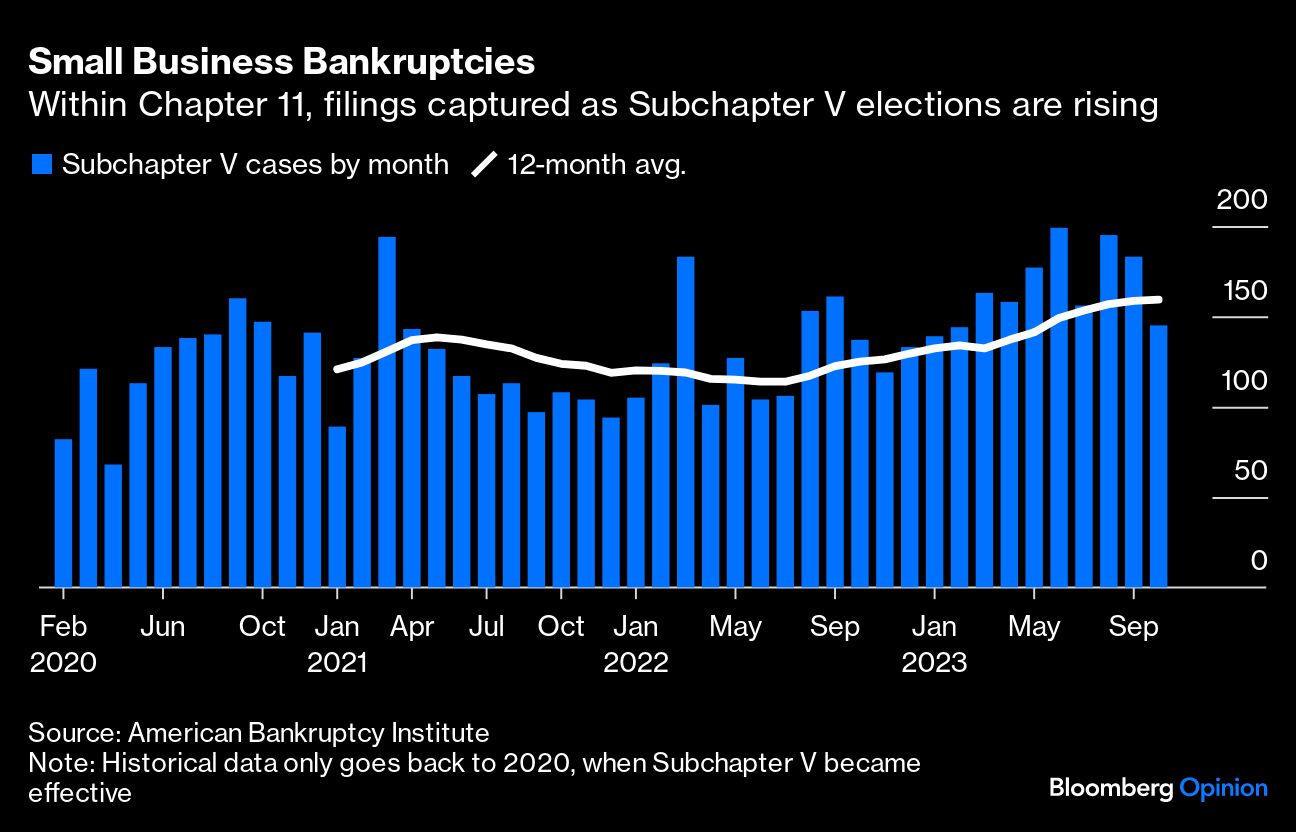

Consider what’s happened so far this year. Small business bankruptcies within Chapter 11 (specifically, Subchapter V elections) rose consistently in the first nine months of the year, giving the appearance of a deterioration in firm finances.

But business failures were uniquely low during the COVID-19 pandemic thanks to extraordinary federal support. Some businesses survived that would otherwise have gone under even in the absence of the Covid disruptions. So it’s conceivable that part of the move up in bankruptcy activity is simply a reversion to “normal” levels from artificially compressed levels in 2021-2022. That doesn’t mean that small businesses are bulletproof, of course, especially after the recent run-up in borrowing costs.

Here’s how Goldman Sachs Group Inc.’s Sienna Mori summarized the situation in a note to clients on Oct. 24 (emphasis mine):

Given the high sensitivity of small businesses to floating rate debt and the low odds of any relief in funding costs or policy support (à la PPP in 2020), we expect the pace of bankruptcies will also continue to revert to historical norms. That said, we think a spike is unlikely, barring a full-blown recession or a more material tightening in lending conditions.

Given that view, Mori contended that there was a “limited risk” of an acceleration in defaults so severe that it would turn into a macroeconomic shock in and of itself. That’s just one shop’s view, but it’s supported by other recent data on the health of America’s smallest companies.

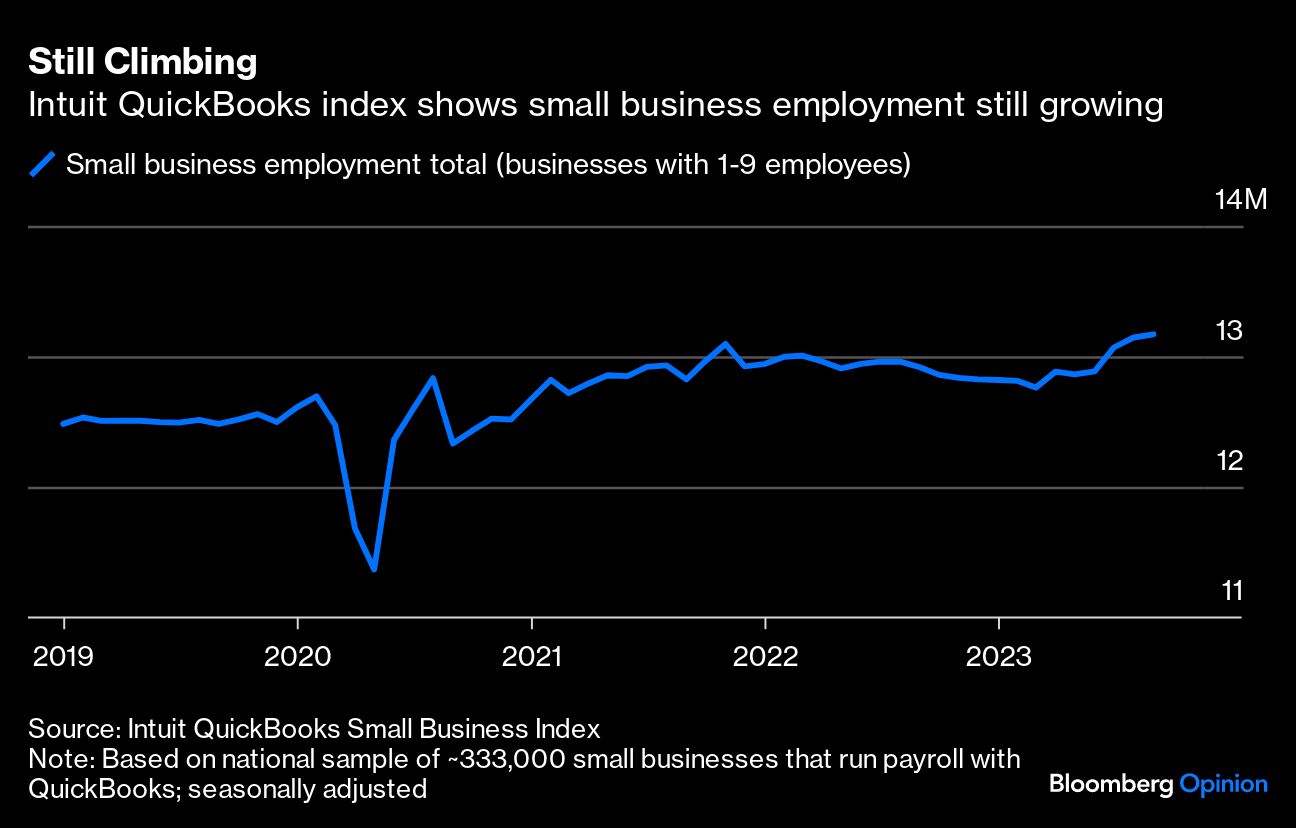

For starters, small businesses continue to hire. The Intuit QuickBooks Small Business Index (which measures employment at very small businesses with 1-9 employees) put employment at a seasonally adjusted 13.2 million in September, up about 1.3% from a year earlier. That’s a bit weaker than the overall trend in US payroll growth tracked by the Bureau of Labor Statistics (up about 2.1% in the past year), but it’s nothing to sneeze at. Small business hiring has been buoyed by leisure and hospitality, as well as the education and health services category.

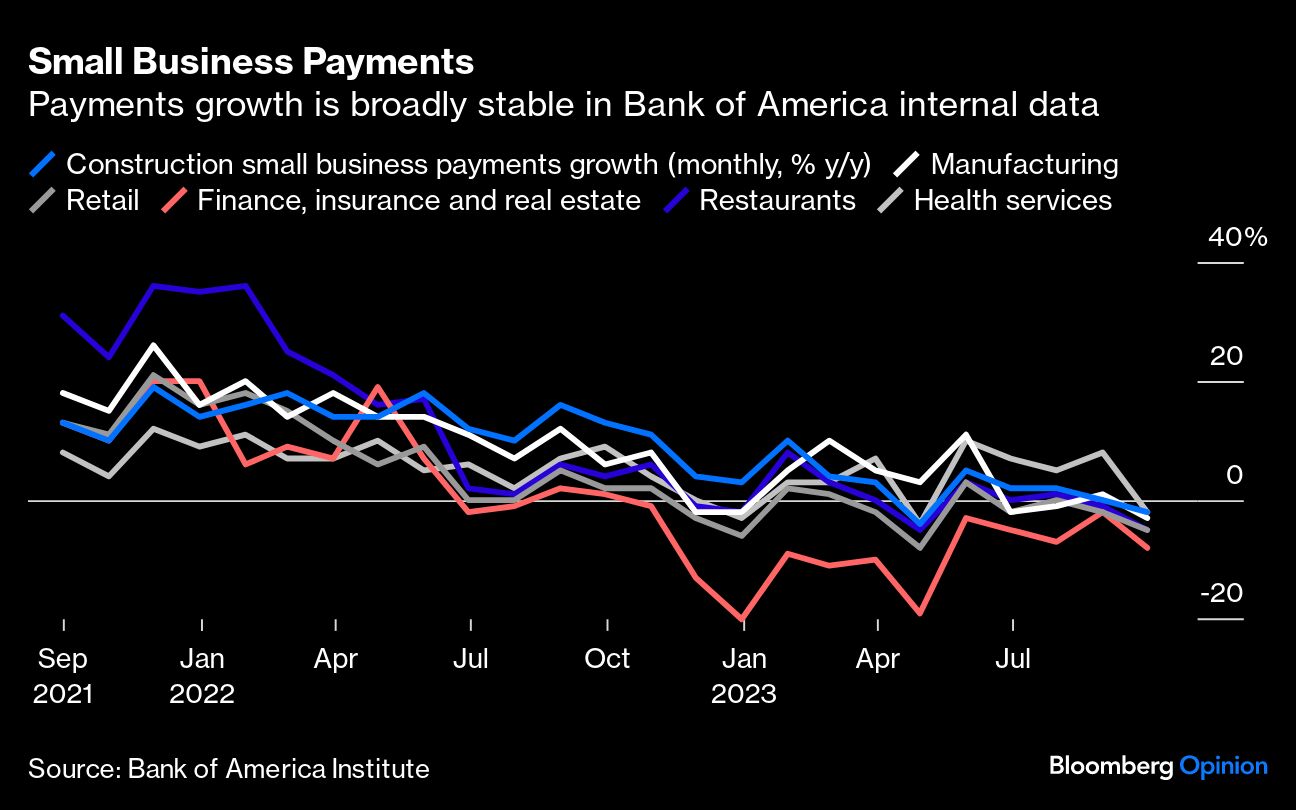

Smaller firms are still spending money as well. Another report this month from Bank of America Institute used proprietary data to show that payments per small business client have been mostly steady in recent months (notwithstanding a 4% year-over-year drop in September, which the report’s authors attributed largely to a calendar effect.)

Here’s the takeaway from Bank of America Institute economists Anna Zhou and Taylor Bowley:

...small business spending growth has moderated from the elevated rates in 2022 but has remained broadly stable over the last few months... Within sectors, we continue to see relative strength in payments spending growth for health services.

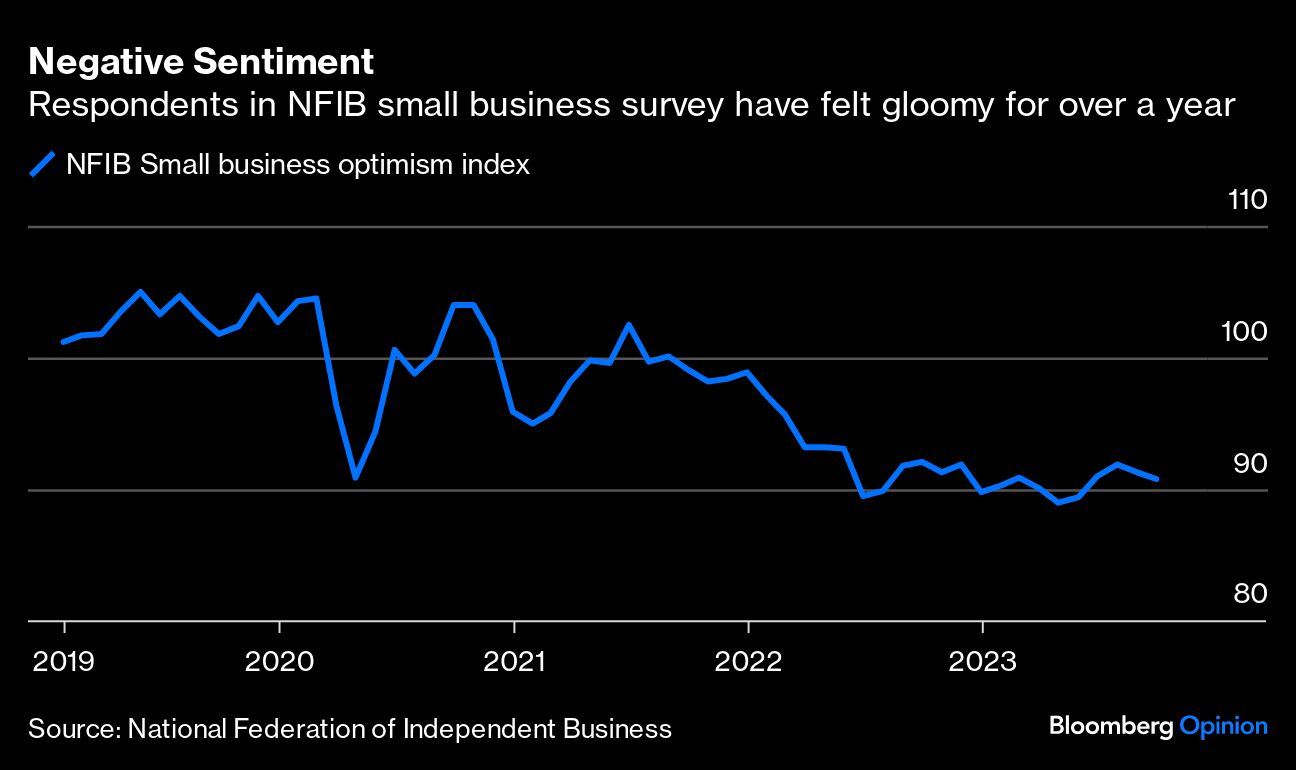

I’m not saying everything is perfectly honky dory. A National Federation of Independent Business survey showed small-business optimism fell a half point in September, extending a period of generalized negativity in the index that’s endured for about 16 months. Sooner or later, negative sentiment can become a self-fulfilling prophecy. But the 2022-2023 economy has showed that consumers and business owners alike haven’t always acted the way they describe feeling. That may be particularly true in the NFIB survey, which has a well-known Republican skew to its sample — and may tell us as much about the state of US politics as the economy.

One final note of caution: The small-business bankruptcy environment is going through some major changes independent of the business cycle. Traditionally, small businesses that struggled or failed have tended to simply close up shop and walk away. If they engaged with the bankruptcy code at all, it was often to pursue liquidation rather than a complex and costly reorganization process to try to salvage the business.

In 2019 (and effective in 2020), an act of Congress created Subchapter V within Chapter 11, which made it cheaper and less technically onerous for small firms to reorganize. That could ultimately lead to more small-business activity in the bankruptcy data, and the advocates of the changes think that’s a good thing. “Part of the growth you’re seeing is just a growing comfort with this,” David Cox, a managing partner of Cox Law Group, told me on Thursday.

During the early days of the pandemic, the Subchapter V option was extended to firms with liabilities of as much as $7.5 million — up from the original $2.7 million limit — and the higher cap is set to potentially sunset next year. So in addition, there’s been speculation that some firms could bring forward filings to avail themselves of the program before they lose the chance. Here, speaking in an interview with me, is American Bankruptcy Institute President Soneet Kapila on that thesis:

It’s a little early for that. But I think as the new year roles around and we’re heading toward the latter part of the first quarter, that attribute may carry more weight because of the uncertainty of whether the debt limit will be preserved or not.

All told, then, recession watchers should be careful about jumping to conclusions over the rise in small-business bankruptcy activity. Smaller firms’ exposure to variable-rate debt may well make them a leading indicator for the American economy, but so far they’re mostly sending a message of resilience. And that may well mean that the US economy can continue to stay afloat as well.

1Different organizations define small businesses different, and here I'm using the Small Business Administration's definition of having fewer than 500 employees. Some of the data herein refers to very small businesses, and I tried to address the different criteria where it comes up.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin