Sometimes Mr. Market just wakes up on the right side of the bed.

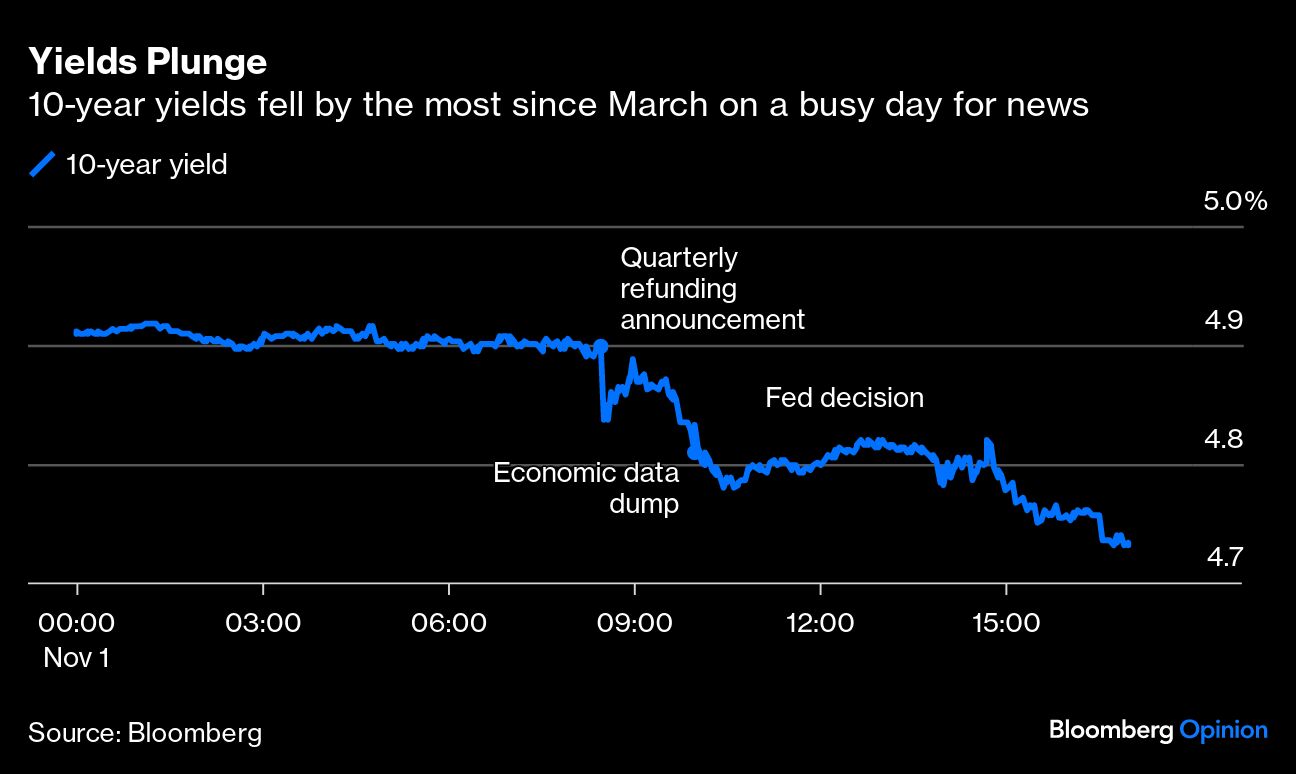

Yields on 10-year Treasury notes plummeted 20 basis points on Wednesday, the most since the banking crisis in March. For all the macroeconomic news of the day, it was hard to pinpoint exactly what changed so meaningfully from one trading session to the next. But the rally suggested that we may be seeing a meaningful shift in sentiment after an abysmal three months, with the potential for it to fuel a virtuous cycle.

Consider the developments:

- 8:30 a.m. EST: The Treasury said it was selling $112 billion of longer-term securities at auctions next week; firms surveyed by Bloomberg had expected $114 billion. Bond yields fell about 7 basis points intraday on easing supply concerns, and were down about 10 basis points from the previous close.

- 10 a.m.: A slew of economic data gave credence to the view that the economy could be slowing (a “good thing” if you want lower interest rates.) Among them, the Institute for Supply Management’s manufacturing gauge posted its biggest monthly decrease in more than a year and trailed all economist estimates. Bond yields fell another 3 basis points.

- 2 p.m.: The Federal Reserve held policy rates steady at 5.25%-5.5%, as was widely expected, and Chair Jerome Powell came off as modestly less hawkish than some investors anticipated — all while keeping his options open for further rate increases and an extended period of elevated rates. Bond yields fell about 7 basis points more.

If I had to pinpoint a single catalyst, I’d say the Treasury announcement got the market off on the right foot. Three months back, a worse-than-anticipated refunding announcement helped set in motion the August-October selloff. This time, markets took solace in the more-modest-than-expected increase in bond supply. But a few billion here or there is of little significance to the massive Treasury market, and none of the other developments were game changers either. Instead, with yields at 4.93% on Tuesday, the market had been effectively braced for more terrible news — and mediocre news was good enough to set off a riotous celebration.

Remember how we got here in the first place. From the end of July through Tuesday, 10-year bond yields surged 97 basis points for equally ambiguous reasons. Investors have blamed factors including the ballooning deficit, increasingly hawkish monetary policy expectations and retreating foreign demand for US debt.

But the math never quite added up. The US budget problems didn’t materialize yesterday (and couldn’t explain such a large bond move in any case); monetary policy expectations haven’t shifted that much in the space of three months; and foreign demand dynamics are as slow-moving as a tanker. The real problem — at least as I see it — was the violent collision of all of those bearish stories. Bond yields temporarily reflected an “everything is going wrong at once” premium.

Academic studies of deficits and interest rates across countries have found that each percentage point increase in the deficit-to-GDP ratio tends to push yields higher by about 30-60 basis points, according to a survey of the literature by Emanuele Baldacci and Manmohan S. Kumar in their International Monetary Fund working paper. Based on that, the fiscal 2023 increase in the budget deficit to 6.3% from 5.4% would explain only part of the July-October selloff, even if you assumed the shortfall was relatively long-lasting.

Meanwhile, investors have been seriously considering the possibility that Fed policymakers may keep rates elevated well into the future. In the Federal Reserve Bank of New York’s September Survey of Primary Dealers, the median respondent expected rates to average 3% over a 10-year period, up from about 2.83% at the end of 2022 — a change of about 17 basis points in 2023. Combine that with the shifting fiscal concerns and it still wouldn’t fully account for the rout.

A lot of it, evidently, was driven by the sense of panic that comes when everything seems to be going wrong at once: Concern about the Treasury's refunding plans, coupled with a Fitch Ratings downgrade to the US in early August, aggravated by famous investors — notably, Bill Ackman — publicly stoking the selloff.

In normal times, US bond investors exhibit a special ability to completely ignore gaping budget deficits. They only start to pay attention when sentiment is already grim — at which time deficits are like gasoline on the fire. The closest historical parallel I can identify is the early part of the Reagan Administration, when inflation and interest rates were still high and Reagan’s spending and tax cuts seemed to arrive at just the wrong time.

Eventually, the pendulum tends to swing back in the other direction, though. And there’s good reason to believe we’re at that point now on the fiscal front. Here’s how Morgan Stanley analysts including Ariana Salvatore and Michael Zezas summarized the outlook in their recent report, “Figuring Out Fiscal Policy” (emphasis mine):

Fiscal expansion is often cited as a reason for positive US growth surprises & government bond yield increases in 2023. Yet, we assess that expansion has peaked, at least until after the 2024 election. Hence, investors focused on upside catalysts for growth & yields should look elsewhere... Recent drivers of the nearly 1% of GDP growth in the federal deficit, most notably deferred tax revenues and the ramp in spending from key bills, will soon be in the rearview. Further, barring a recession that incentivizes a Congressional response, we think legislative action that expands deficits is unlikely until at least after the 2024 election.

I don’t want to come off as a deficit apologist, and I hope that the recent bond selloff triggers some serious soul-searching among politicians in Washington. But I now doubt that the current deficit narrative will continue to punish this bond market any more than it already has. So much negativity has already been priced in over the past several months, and now there’s even a chance for some near-term deficit relief. At the same time, Fed policymakers appear to be sending some modestly encouraging signs about interest rates, with Chair Powell hinting that bond yields may be doing some of his work for him.

With all of that, the panic premium is likely to keep fading. That’s why there may be reason to trust the hard-to-explain bond rally that took hold on Wednesday. If we’re lucky, it could even have more room to run.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin