Billionaire Stan Druckenmiller isn’t letting up on his criticism of US Treasury Secretary Janet Yellen. Druckenmiller says Yellen committed an epic mistake by failing to meaningfully term out America’s debt when rates were ultra-low — a missed opportunity he’s characterized as “the biggest blunder in the history of the Treasury.”

On top of some obvious partisan overtones, that characterization seems to treat the world’s largest budget like a hedge fund. It’s also wildly unfair.

Here’s Druckenmiller in his own words (from a recently on-stage interview with fellow billionaire Paul Tudor Jones):

...when rates were practically zero, every Tom, Dick and Harry — and Mary — in the United States refinanced their mortgage, they extended. Corporations extended. Unfortunately, we had one entity that did not, and that was US Treasury. And Janet Yellen — I guess because political myopia, whatever — was issuing 2 years at 15 basis points when she could have issued 10 years at 70 basis points or 30 years at 180 basis points. I literally think if you go back to Alexander Hamilton it was the biggest blunder in the history of the Treasury, and I have no idea why she has not been called out on this. She has no right to still be in that job after that.

Let’s start with the facts. Yellen never had a chance to issue 10-year notes at 70 basis points; that was Treasury Secretary Steven Mnuchin during the end of the Trump administration. Druckenmiller — the family office operator who, for context, has long supported Republican candidates for president — should surely know that. His decision to gloss over the detail suggests there’s more than an ounce of partisan spin behind his analysis.

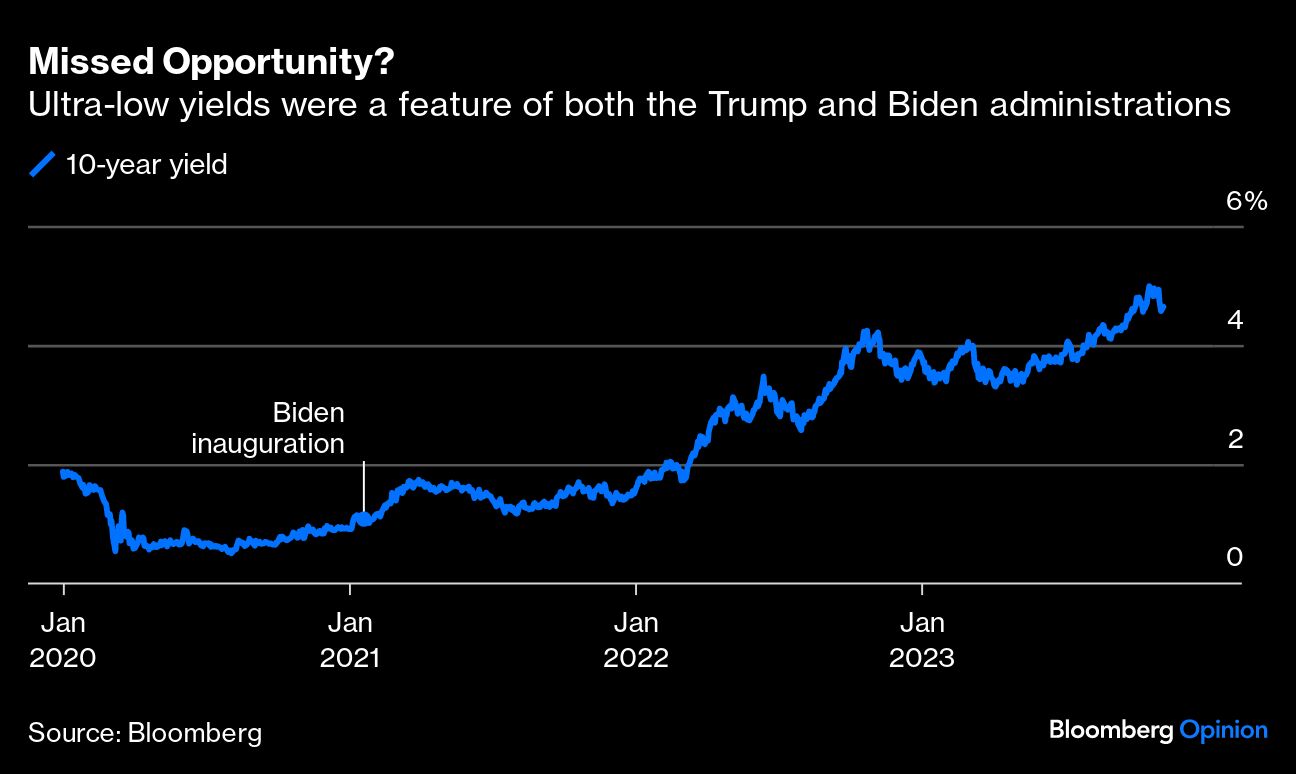

Nevertheless, let’s take the broader point at face value. In Yellen’s first year on the job, 10-year yields did average around 1.48%, an amazing bargain when compared with the 4.62% 10-year yields (or 5.39% 1-month yields) that prevail at the time of writing. So why weren’t Yellen and Mnuchin — who has a trader’s mentality much like Druckenmiller — more opportunistic? Why didn’t Treasury behave more like a hedge fund or like those 14 million mortgagors who refinanced in the seven quarters between the start of the Covid-19 pandemic and the end of 2021?

Simply put, Treasury is not a household nor a hedge fund — as Mnuchin surely learned on the job. It is far less nimble and infinitely more important, overseeing the issuance of securities that then serve as a global benchmark off which trillions of dollars of debt instruments are priced. In support of its efforts to fund the government at the lowest cost to taxpayers, it aims to offer securities “through regular and predictable issuance.” It also tends to believe — as supported by decades of history — that short-term borrowing is cheaper than longer-term borrowing.

For all their simplicity, these principles have served the Treasury Department well over the decades. From time to time, it can tweak its offerings, but it’s a laborious process that requires conducting research and signaling its intentions to the marketplace. Mnuchin did talk often about extending the maturity of the debt, as Bleakley Advisory Group LLC Chief Investment Officer Peter Boockvar catalogued in Monday’s edition of his Boock Report. But aside from the reintroduction of the 20-year bond in 2020, Mnuchin hardly did anything revolutionary. In Boockvar’s words: “All this talk, all the studying and not much was done.”

Why? Because there are major consequences to consider when you dramatically change the way the government funds itself. Treasury’s every move is hyper-analyzed by speculators and glitchy algorithms, and decisions about how much debt to issue — and at what maturities — can cause unintended market meltdowns, undermining the government’s goal of minimizing costs.

Consider the lessons of August 2023. On Aug. 2, the US Treasury boosted its note and bond sales at its so-called quarterly refunding auctions, a tweak that was only slightly larger than dealers had been expecting at the time. The plan came just a day after Fitch Ratings had cut the government’s AAA credit rating, and the unfortunate timing helped contribute to a toxic narrative about the deteriorating US budget deficit and a perceived glut of forthcoming debt. Taken together, the downgrade and bond-auction boost helped catalyze a three-month rout in longer-term securities that will cost US taxpayers.

Back in 2020 and 2021, there were plenty of reasons for Treasury officials to be cautious about just such a tantrum. The government’s focus was on maintaining access to inexpensive funding to address the massive pandemic health crisis. And while plenty of people (including former Treasury Secretary Robert Rubin) suggested an opportunistic approach, it was far from an obvious move at the time. There was widespread uncertainty about how much longer the pandemic would last, and few predicted that the worst inflation in 40 years would force the Federal Reserve to push policy rates to 5.25%-5.5%.

Obviously, given a crystal ball that foretold the trajectory of inflation, Treasury would have sold more longer-term bonds, but wagering on much higher short rates was a risky and out-of-consensus bet. Even in the latter part of 2021, the median economist surveyed by Bloomberg still thought policy rates would be at 1.5% at the end of 2023. Yellen could have acted like a trader and bet big against consensus, but that would have run astray of the Treasury Department’s risk management principles.

Here’s how James Clark, the Treasury Department’s deputy assistant secretary for federal finance during the Obama administration, put it in a February 2021 opinion column around the start of Yellen’s tenure:

Decisions to issue - or stop issuing - certain securities based upon a political appointee’s assessment of the level of interest rates is certain to open a pandora’s box. If that were to happen, the significant liquidity premium earned over the years through the Treasury’s “regular and predictable” approach to debt management would quickly evaporate, leading to higher relative borrowing costs across all of the Treasury’s debt issuances.

Monday morning quarterbacking is a great and entertaining hobby, of course, and I’m sure Druckenmiller is scoring some points in political circles. (He recently turned up on a list of donors to former New Jersey Governor Chris Christie.) Obviously, there’s a lot that Yellen would change if she had a time machine that could take her back to 2021 — and the mix of debt securities sold at auction is just the start. Surely, she’d also want to dial back the amount of inflationary stimulus pumped into the economy (that’s another column entirely.) But in the long run, we’re still well-served by leaders who manage government funding in the most boring and predictable way possible. The US is not a hedge fund, and it should never be run like one.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.