On Wall Street, there’s always a lot of excitement around the latest inflation report. Tuesday’s better-than-expected number was an extreme example — bond yields plummeted and stocks surged. But at the Federal Reserve, policymakers tend to focus on multi-month trends, which are sending extremely mixed signals. And billionaire Ken Griffin, for his part, thinks we should take an even longer view.

Let’s start with the good news. Tuesday’s report showed the core consumer price index rose just 0.2% in October from a month earlier, which annualized to about 2.8% — within spitting distance of the Fed’s 2% target.1 The median economist surveyed by Bloomberg had thought the number would come in around 0.3%, and 11 of 65 respondents predicted a jump of 0.4% (more on why later.) As a result of that positioning, the reported set off a 20 basis-point yield drop on two-year notes, the biggest one-day move since March.

The guts of the report were also encouraging:

-

Shelter, a massive and inertial category, rose just 0.3% from the previous month, reversing an alarming spike in September.

-

Core services excluding housing — a bespoke cut of the overall data that Fed Chair Jerome Powell has said he watches closely — rose just 0.2%, also slowing from September.

-

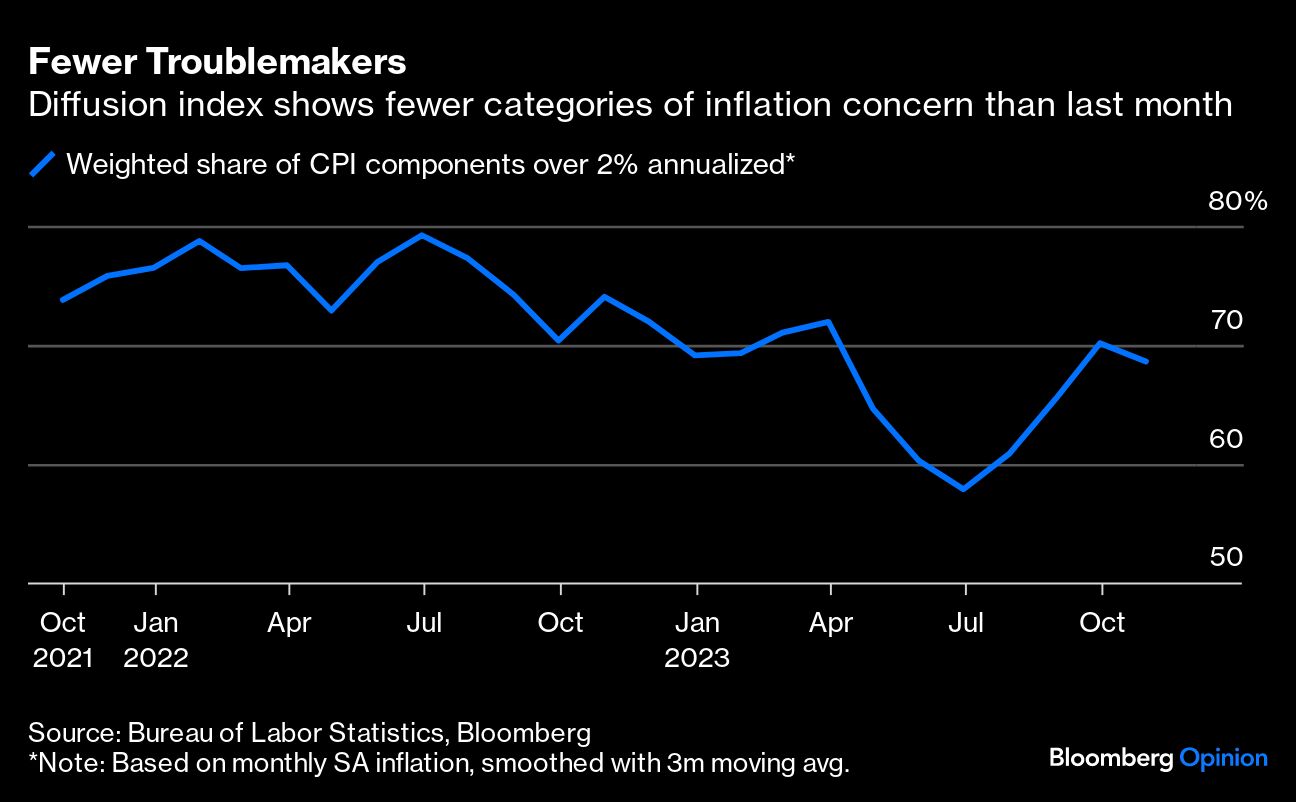

And the weighted share of CPI components running above a 2% annualized pace fell to about 69% from 70% (although it was still up significantly from the recent low of 58% after the June report.)

So what does the latest news do for the long-term trend?

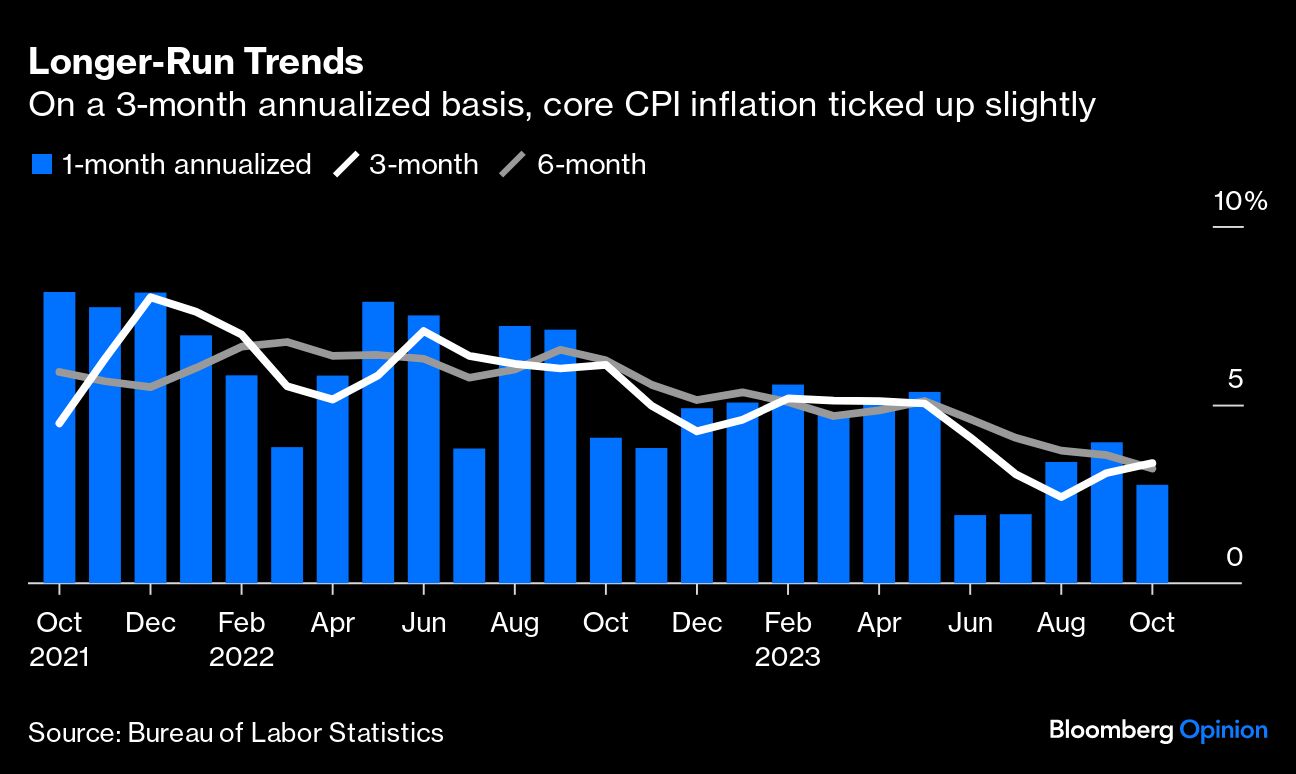

As the chart below shows, the three-month annualized rate of core inflation ticked up a bit, and it’s still too high for policy makers to feel comfortable that they’ve tamed inflation. Of course, the outcome was better than the alternative; under a counterfactual scenario in which the 0.4% core CPI inflation forecasts had come true, the three-month annualized pace would have moved up more, to 4.1%, and progress on the six-month rate would have essentially stalled. In conjunction with other data on the real economy, it’s possible that would have helped build the case for further rate increases as soon as December or early 2024. Instead, those rate increases are delayed, though not necessarily canceled.

Policymakers focus on moving averages for a variety of reasons. Seasonal adjustment factors get revised (which can retroactively change the interpretation of a given a report); the index contains a number of imputed categories that behave in quirky ways (recent movements in owners' equivalent rent and health insurance are key examples); and month-to-month data are just inherently noisy.

This month, the Bureau of Labor Statistics’ health insurance category — one of those methodologically odd ones — was widely expected to show price increases after 12 straight months of declines. Health insurance prices are very hard to measure, so the government essentially backs into an estimate once a year and then spreads it out over the ensuing 12 periods (a methodology that, by the way, isn’t shared by the personal consumption expenditures index, the Fed’s preferred inflation gauge.) Since that effect was foreseeable, many analysts thought it might combine with inflation in other categories to help fuel a larger jump overall. In the end, health insurance jumped, but there were more than enough offsets — good news for sure, but also a reminder of how these numbers are funky and imperfect and should be taken with many grains of salt.

Next, there’s the longer-term outlook for inflation and bonds. Griffin, the Citadel founder, thinks the forces of de-globalization and the end of the “peace dividend” could mean higher baseline inflation for decades. Griffin, not unlike other prominent investors including Bill Ackman, warned last week that the pandemic experience together with rising geopolitical tension may lead countries to produce more domestically, fueling higher baseline inflation, possibly for “decades.”

Here’s how he put it at the Bloomberg New Economy Forum last week in Singapore:

Regretfully, the peace dividend is clearly at the end of the road. No matter what one may dream to be reality, reality is there’s two wars in the world right here, right now, one of which is in Europe. So there’s no doubt that the NATO countries are going to have to increase defense budgets over the years ahead. That’s going to come at a point in time where governments around the world are already struggling with the sizes of their deficits.

On globalization, he added:

...now we’re talking about deglobalization, we’re talking about rearchitechting supply chains. And some of this is rooted in the behavior that we saw in the pandemic. We saw countries hoarding personal safety equipment. We saw the tension around the distribution of vaccines around the world. Countries are much more sensitive to what do we want to have created domestically so that we’re not relying upon global trade.

I’m not saying I have a lot of confidence in this gloomy outlook. Nevertheless, Griffin describes a plausible risk scenario in an uncertain world. That narrative has been a driving force behind markets recently, and nothing in Tuesday’s report will tell us whether Griffin is right or not. If Tuesday’s inflation report shows us anything for sure, it’s that forecasting is hard, even when looking a month out, never mind a few decades.

As recently as yesterday, Fed funds futures implied about a 1-in-4 chance that the central bank would go higher and limited odds of an interest rate cut before June or so. Today, markets priced out an additional hike and show better than even odds of a reduction by May.

Griffin reiterated some of his earlier views on the peace dividend during an interview with Bloomberg's Sonali Basak on Tuesday, and also weighed in on the Fed. He allowed for the possibility of rate cuts next year under a scenario in which near-term inflation continues to moderate and unemployment ticks up, but, he said, the Fed must be careful about the signals it sends in the process.

“The key from my perspective is the Fed needs to stay on message that they're going to put the inflation genie back in the bottle,” he said. “And if they cut too soon, I think they risk losing credibility around their commitment to a 2% inflation target.”

Let’s be clear: In a market that’s been rocked by a lot of bad inflation news, this number could have been much worse, and less bad than expected is worth celebrating — albeit very briefly. It slashes the likelihood of a Fed rate increase in the months ahead without taking further tightening off the table down the road. But for all its positive qualities, Tuesday’s report won’t resolve most of the big outstanding questions governing global markets. Taking the long view, the inflation outlook is still roughly as hazy as it was yesterday.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin