The deflationistas have been working themselves into a tizzy since Walmart Inc. Chief Executive Officer Doug McMillon warned of a period of declining prices at the big-box retailer in the months to come. But as a purveyor of goods, McMillon is talking about something very different — and actually quite normal — from what Cathie Wood and other deflation alarmists seem to have in mind. In fact, a period of falling goods prices might be just what policymakers need to slay too-high inflation once and for all.

First, consider the context. Here’s what McMillon said in his quarterly conference call with analysts on Thursday:

In the US, we may be managing through a period of deflation in the months to come. And while that would put more unit pressure on us, we welcome it because it’s better for our customers.

As he later clarified, he was mostly talking about Walmart’s “general merchandise” — so non-grocery stuff — and that’s nothing entirely new.

In the two decades before the Covid-19 pandemic, it was relatively normal for manufactured consumer products to decline in price or, similarly, for consumers to pay steady prices for ever-improving items (a sharper television, a more advanced mobile phone, etc.). Indeed, a quick search of Walmart’s earnings transcripts reveals plenty of instances of management discussing “deflation” in the past 20 years.

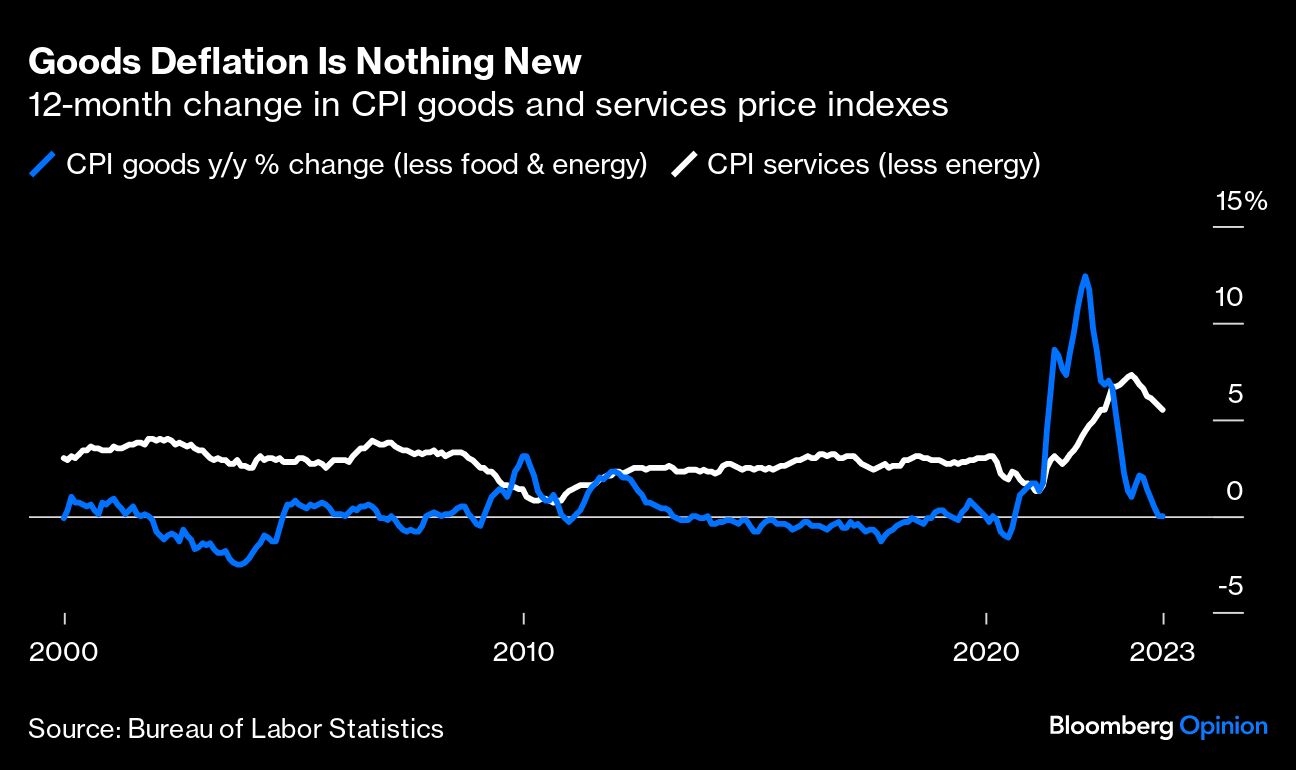

That stands to reason since Walmart is in some ways a proxy for the overall goods economy. From 2000-2019, core goods inflation measured by the consumer price index averaged 0%, and there were 118 months of year-over-year deflation. You might attribute that to a variety of factors, but globalization was the big one.

That’s precisely how the US has managed to sustain overall inflation near the Federal Reserve’s 2% target in a world in which the heavily weighted non-energy services categories have tended to inflate at about 2.5%-3% year-over-year.

There’s a reason the D-word strikes such fear into the hearts of markets and economists. Falling prices may lead consumers to expect better deals in the future, so they could delay purchases and slow economic activity — witness Japan’s long struggle to shake off its deflationary malaise. Even though central banks claim to want price stability, most advanced economies actually aim for a small bit of inflation. That’s generally considered the best way to keep the economy humming along and maintain a margin of distance from the specter of backsliding prices. Nobody should be rooting for deflation in the US, and it’s highly unlikely to happen anytime soon.

As Morgan Stanley Chief US Economist Ellen Zentner put it on Bloomberg Television Thursday, Walmart’s price dynamics may in part reflect its customer base. She said lower-income consumers are facing the greatest financial stress (their credit-card and auto delinquency rates are rising) and businesses have been cutting prices to adjust accordingly. But responding to a question from Bloomberg’s Lisa Abramowicz, she also downplayed concerns that the Walmart pricing comments were a reason for broader economic concern:

Good sectors I’m not worried about at all. Goods prices in the US have been in deflation for a decade leading up to Covid. That’s normal, right? We were importing a lot of deflation. But that’s externally determined. I would be very, very concerned about a deflation scenario in the US for services, for domestically-determined prices. For us to get to that broadly, you’re talking about an extraordinary downturn on the magnitude of the financial crisis in 2008 that would get that kind of price declines — declines in the level of prices. Instead, I think deceleration is in train.

McMillon’s comments may well say something concerning for Walmart shareholders. The stock slipped 8.1% on Thursday despite better-than-projected earnings, a slide largely attributed to management’s cautious outlook. But their macroeconomic implications aren’t particularly alarming.

The deflation that ARK Investment Management’s Wood has been warning of has a different flavor. She recently pointed to the weak trends in commodities, airlines and autos to underline her forecast for widespread price declines, which she expects will be triggered by new technologies including artificial intelligence, electric vehicles, robotics, genomic sequencing and blockchain. I suspect that forecast is highly unlikely, and every mainstream economist surveyed by Bloomberg seems to agree with me.

If anything, the main risk to the price outlook seems to be goods inflation, not deflation. If billionaire investors such as Ken Griffin and Bill Ackman are right then we’re facing a period of deglobalization, the consequence of which could be goods prices that increase persistently in a way that we’re just not used to.

In part, Griffin and Ackman have argued that rising geopolitical tensions and the pandemic experience will lead developed economies to produce more domestically, even if it means higher prices. Holding services inflation constant at 2000-2019 levels, that would mean higher overall inflation and marginally higher interest rates for the foreseeable future. (Personally, I’m much more optimistic than Griffin and Ackman that nations will choose peace and global commerce over war and inflation, but the hedge fund titans have described plausible risk scenarios that everyone must consider.)

On the other hand, a bit of goods deflation is nothing to fear in the near term, and it certainly isn’t a sign of an economic downturn. If anything, it may be a key part of our path back to some semblance of price stability — and a precondition for lower interest rates down the road.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.