Federal Reserve Chair Jerome Powell faces a communications conundrum at the central bank’s policy meeting this week. Luckily for him, he could just let the Summary of Economic Projections do most of the talking — and avoid unnecessary misunderstandings.

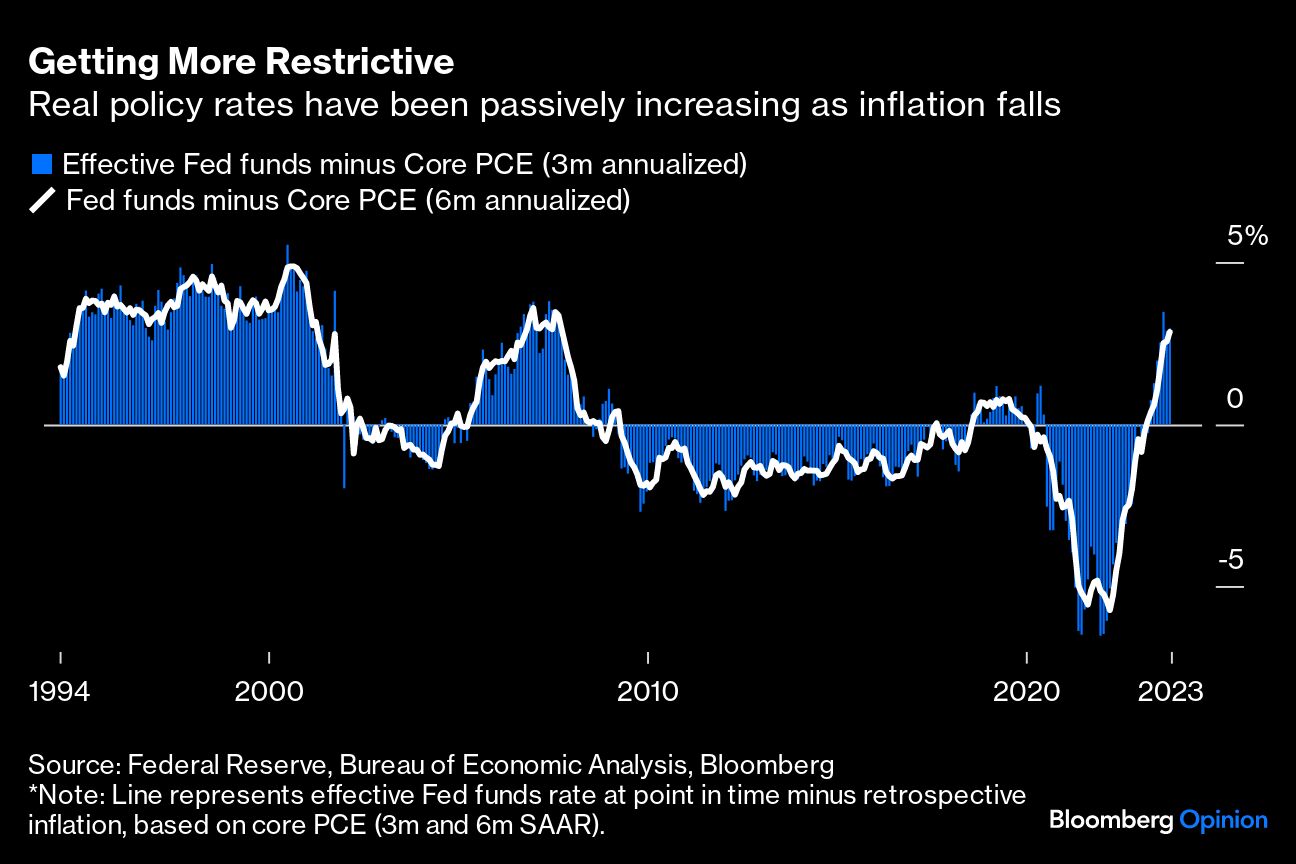

At issue is how to convey where the Fed is heading next. Central bankers tend to think about monetary policy in terms of inflation-adjusted (or “real”) policy rates. At present, those are at their tightest since at least 2007, and they may passively tighten further if inflation continues to fall. Against that backdrop, policymakers will probably want to surgically cut rates next year to prevent policy from becoming too restrictive and causing unnecessary harm to the economy. In other words, the Fed will probably want to cut rates without immediately easing policy — a tricky message to convey to markets and the public.

Last month, Fed Governor Christopher Waller tried to explain this, and it didn’t exactly go swimmingly. “It’s just consistent with every policy rule I know from my academic life and as a policymaker,” Waller told an audience at the American Enterprise Institute in Washington, responding to a question from the Wall Street Journal’s Nick Timiraos. “If inflation goes down, you would lower the policy rate.” Waller was basically describing the principles of Central Banking 101 — not unveiling a new forecast — but the market seemingly heard: “A cycle of cuts is coming!” Yields on two-year notes plunged 15 basis points on the day and 35 basis points over four sessions.

If the Fed is trying to avoid unnecessary market swings and keep financial conditions reasonably tight until the inflation war has been incontrovertibly won, it wasn’t Waller’s most effective public appearance. However, I’m not sure what he could have done differently, short of punting on the question entirely. So should Powell just bob and weave when the same question comes his way at the central bank’s post-policy decision press conference on Wednesday? The best approach — and the most intellectually honest one — is simply to point markets and journalists to policymakers’ forecasts in the Summary of Economic Projections (or SEP), which are set to be freshened up on the day of the decision.

The SEP, of course, aggregates the anonymized forecasts of all Federal Reserve Board members and Federal Reserve Bank presidents. Four times a year, they update their outlooks for real gross domestic product, unemployment, inflation and the federal funds rate. While all the data is useful, I’ll be focused not on the individual projections in isolation, but what they say about each other — and how the Fed would react under different scenarios.

The inflation forecasts should reflect increasing optimism about the central bank’s ability to return to its 2% target in a timely manner. Based on annualized three-month and six-month core personal consumption expenditures inflation, price gains are already running at around a 2.4%-2.5% clip. But policymakers have been so humbled by the experience of the 2021-2023 inflation rollercoaster that they’re likely to err on the side of “following the data” and not try to make policy based on a forecast.

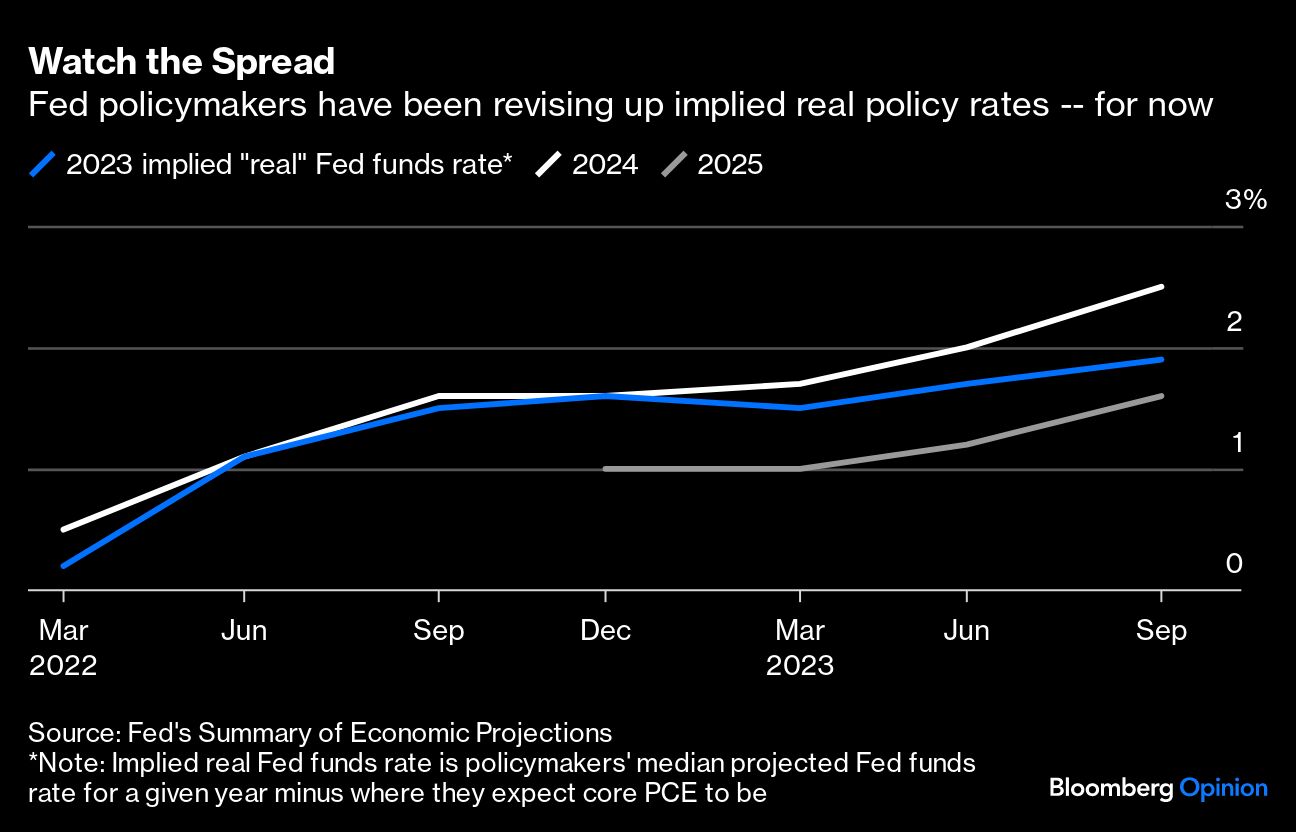

They do, however, have a pretty clear sense of how they’d react given certain scenarios. When policymakers last updated the SEP, the median respondent thought that rates would probably end 2024 at 5.1% conditional upon 2.6% core PCE inflation. I’ll be looking closely at how policy makers are thinking about that spread.

Needless to say, it’s critical to understand how policymakers are thinking about what constitutes “sufficiently restrictive” policy. At present, the figures suggest that policymakers would like to see rates remain about 2.5 percentage points above their best estimate of inflation next year, putting the non-recessionary floor on nominal policy rates at about 4.5%. But remember, as recently as March, they thought a spread of about 1.7 percentage points would do the trick in 2024. It’s possible their assessment may have changed again.

Certainly, none of this is quite as straightforward as my arithmetic here suggests. For starters, there’s considerable debate about how best to measure real policy rates. Nominal interest rates are prospective and inflation statistics are retrospective, so many people rightly say you should instead focus on forward-looking estimates of the price trajectory, including those implied by surveys or markets. But that approach has its drawbacks as well, since future inflation is inherently unknowable.

Moreover, the perception of what constitutes a “restrictive” real policy rate is itself fluid over time and a matter of considerable debate. Most economists believe that the so-called neutral rate — which is neither restrictive nor accommodative — has trended downward over recent decades. According to the SEP, the median Fed policymaker seems to think it’s hovering around 0.5 percentage point, but that estimate could conceivably change. Indeed, some private sector economists have already been revising their estimate of neutral higher, and it will be instructive to see whether policymakers move in that direction as well. Powell made clear in remarks Dec. 1 that he considers the Fed to be “well into restrictive territory.”

On the surface, the Fed isn’t likely to do much on Wednesday: Economists firmly believe — as do I — that policymakers will hold rates steady in a target range 5.25% to 5.5%. The market’s attention will be on the signals that they send about the future, especially as traders try to gauge the timing for rate cuts next year. Powell and his colleagues gain little by explicitly talking about this and risking further misunderstandings. Instead, the Fed chair would do well to let the projections in the SEP speak for themselves.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin