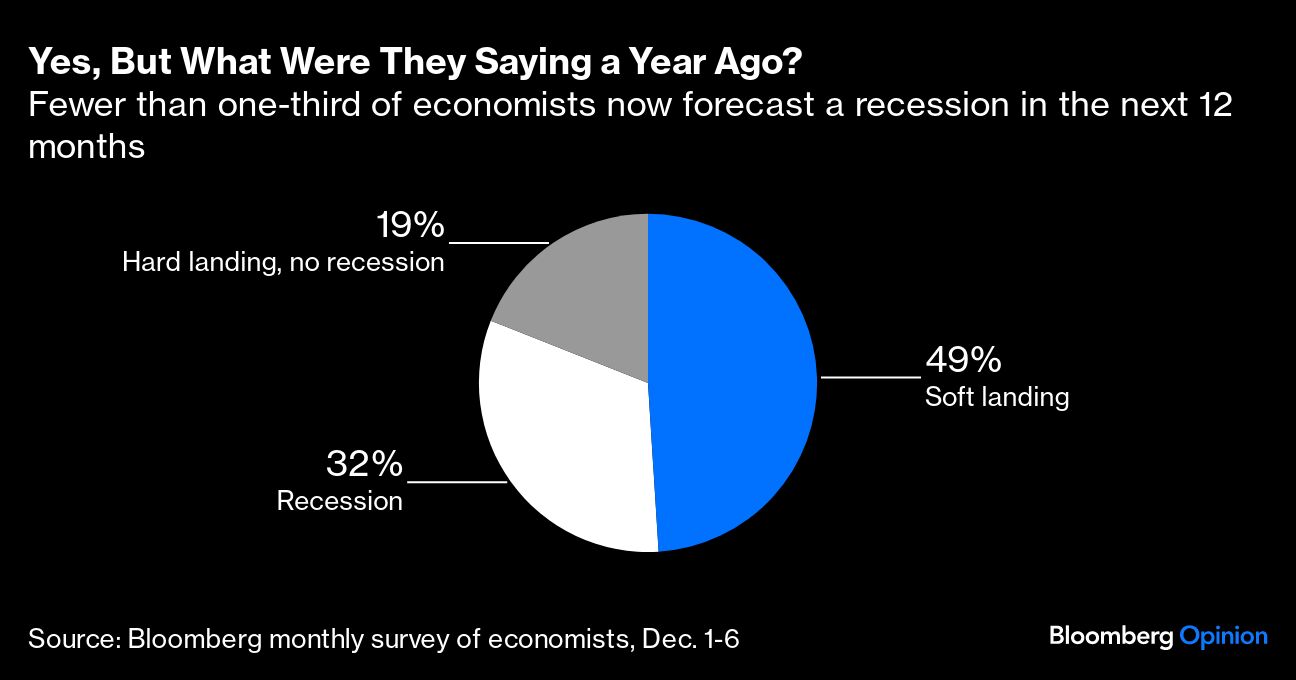

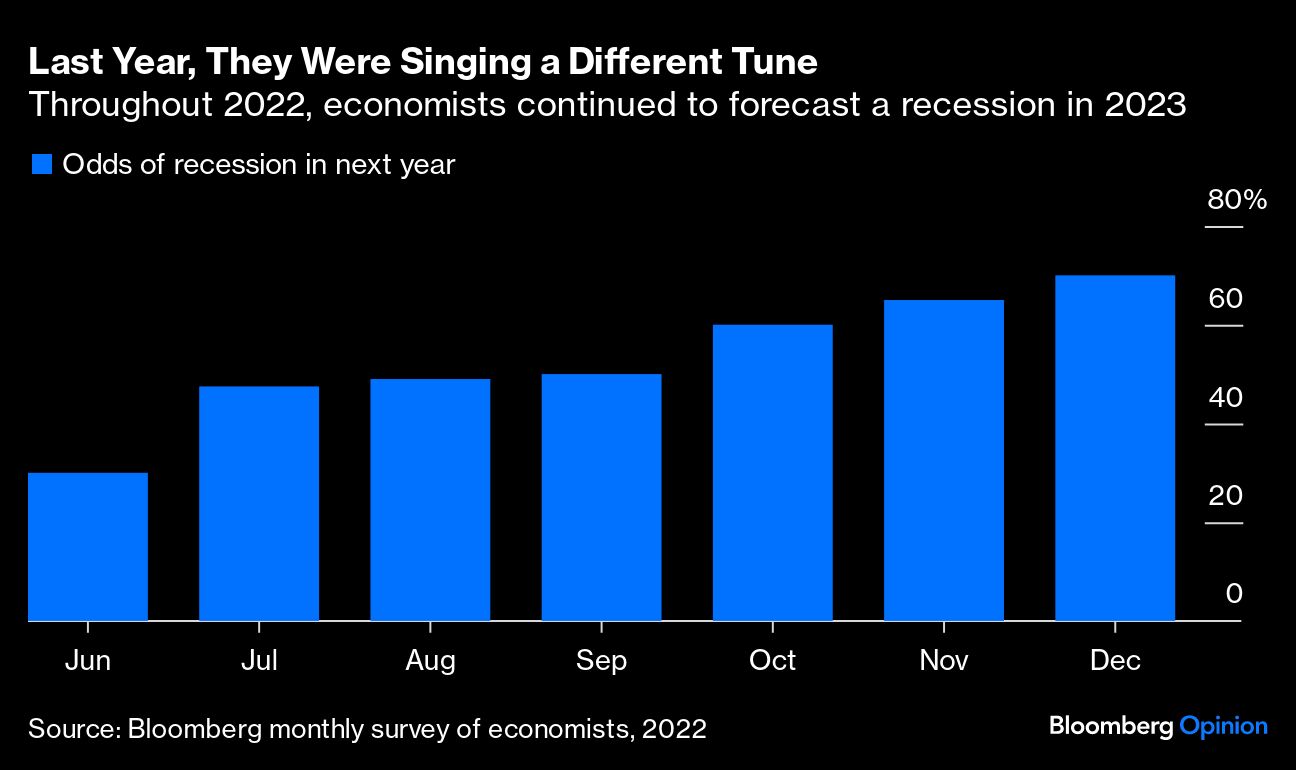

Last year at this time, 85% of economists in one poll predicted a recession this year — and that was an optimistic take compared to the 100% probability of a recession forecast two months earlier. Meanwhile US Federal Reserve Chair Jerome Powell, drawing upon the work of his highly able staff, expressed fear in March that bringing down the rate of inflation would cost millions of American jobs.

And yet none of this has happened. Both inflation and unemployment are headed in the right direction, and most economists expect the US to avoid a recession in 2024. Economists have yet to figure out why things went so well, but it is already clear that a reckoning is due.

As Treasury Secretary Janet Yellen said last week: “So many economists were saying there’s no way for inflation to get back to normal without it entailing a period of high unemployment, [or] a recession. And a year ago, I think many economists were saying a recession was inevitable. I’ve never felt there was a solid intellectual basis for making such a prediction.”

Many of those economists may have been relying on the work of … Janet Yellen. Her own (highly regarded) macro research focuses on nominal price and wage stickiness and output-inflation trade-offs, predicting that if there is a significant fall in aggregate demand, employment should also fall, giving rise to a recession. She is also co-author (with many distinguished colleagues) of a well-known paper arguing that there is an output/inflation trade-off even at high rates of inflation.

Economist Christina Romer (often with co-authors) has provided some of the most persuasive evidence that negative monetary policy shocks induce recessions in output and employment. Her work has been especially influential — worthy of a Nobel Prize, in my opinion — because it does not rely on a complicated mathematical model of the economy, and it had been accepted on a bipartisan basis. Paul Krugman has been predicting for most of this year that the recent disinflation would not cause a recession, and he deserves credit for getting this right. Yet he is less keen to tell us that for many years he trumpeted the predictive virtues of old-style Keynesian macroeconomics, using models that predict disinflation will lead to a loss in output and employment.

Krugman has lately further explained his position — complete with unironic headline — suggesting that the untangling of broken supply chains had helped lower the rate of inflation. That point, too, is correct. He didn’t mention that there also has been a massive negative shock to aggregate demand: High rates of M2 growth became slightly negative rates of M2 growth. Fiscal policy peaked and then retreated. The Fed raised interest rates from near-zero levels to the range of 5%, and fairly rapidly. It also sent every possible signal that it was going to be tight with monetary conditions.

And yet a recession did not come.

There is a reason that so many economists had been predicting a recession — and it is not because they are out of touch, or repeating talking points from Donald Trump’s presidential campaign. They predicted a recession because that is what experts such as Yellen, Krugman, Romer and many others had been teaching for decades. I do not myself presume to have any immunity from the general confusion here, as all along I thought there was a reasonable chance of a recession.

Lawrence Summers turned out to be wrong in predicting that disinflation would have huge costs in terms of employment and output, and now he is catching grief for this on social media. Yet at least he was drawing upon a consistent model. The problem is that the real world is not as consistent as model builders might like.

The solution here is not to sweep past doctrine under the rug; it’s to be more forthright. Macroeconomists very often don’t know what is going on, and that holds true for all the different styles and flavors of macro.

The one theory that might at least partly explain recent events — that of a credible disinflation based on rational expectations — had fallen out of favor with economists, most of all the Keynesians. This approach still is receiving very little credit, even though it has the Nobel prizes of Robert E. Lucas and Thomas Sargent to support it.

Most of all, it’s important to acknowledge how politicized macroeconomics has become. There are a bunch of economists going around right now saying they were right about how the US would avoid a recession this year. A deeper look, however, reveals a much longer and less favorable story.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.