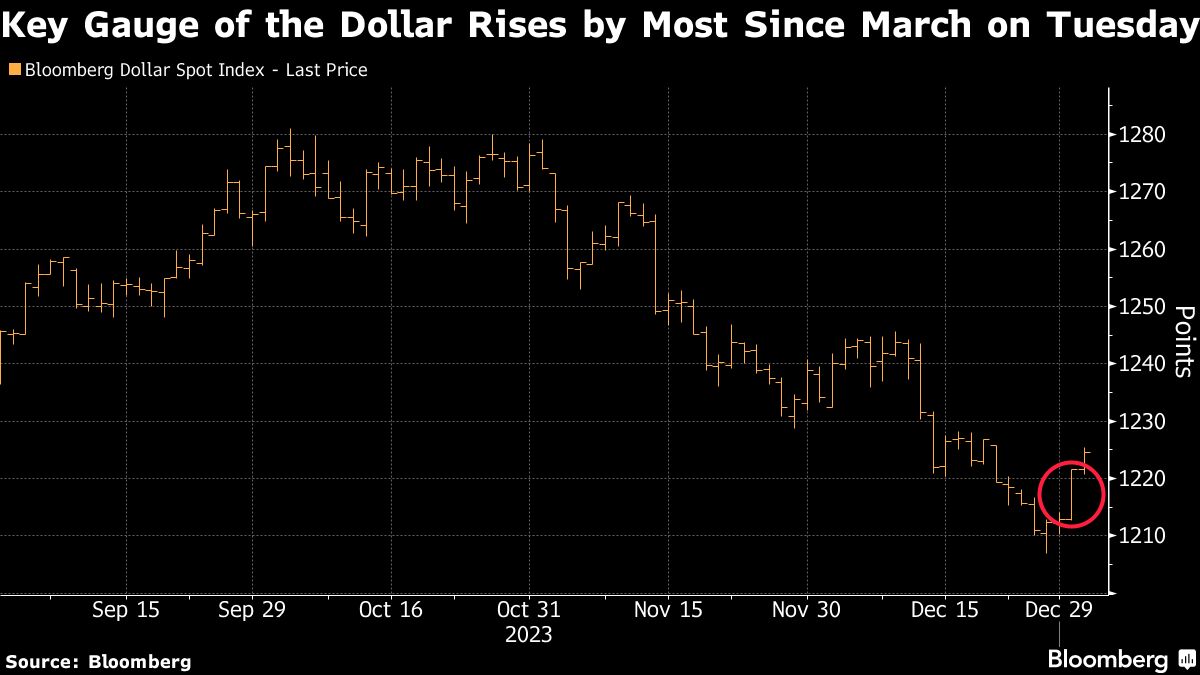

The dollar kicked off the new year with its biggest daily jump since March as traders pared back bets on the scale of the Federal Reserve’s 2024 interest-rate reductions.

The Bloomberg Dollar Spot Index closed higher by more than 0.7% on Tuesday, its biggest one-day advance since the wake of the regional banking turmoil more than nine months ago. The greenback advanced another 0.3% on Wednesday, with the Japanese yen, Australian dollar and Swiss franc losing the most among peers in the developed world.

Such a euphoric start to 2024 comes after a rocky path last year, when the dollar’s performance was largely driven by speculation surrounding when — and by how much — major central banks would cut their key policy rates. The currency fell 2.7% last year, the worst annual performance since the pandemic in 2020.

“The Fed expectations are still all over the map,” Brad Bechtel, global head of foreign exchange at Jefferies. “We have to see how it plays out the next few days.”

Traders are looking ahead to Wednesday’s release of minutes from the Federal Reserve meeting in December when officials signaled an end to their aggressive campaign of interest-rate increases. An array of labor-market data due later this week is forecast to highlight a US labor market that remains resilient while gradually cooling.