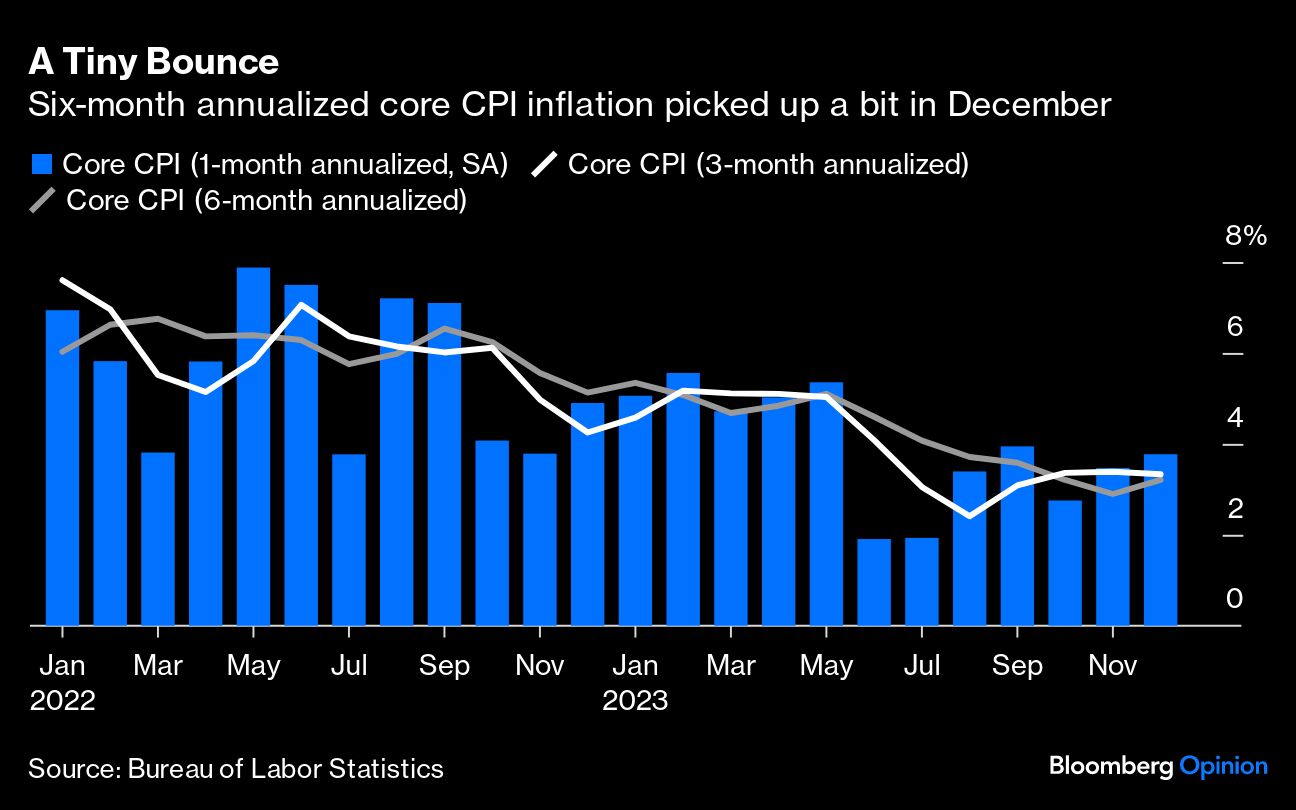

The Federal Reserve is likely to cut policy rates this year less than the market expects, and the latest inflation report shows why. The consumer price index rose 0.3% in December from a month earlier, pushing the six-month annualized rate up to 3.2%, from a previous 2.9%. Although it was basically a fine report, it wasn’t pristine — and the market is priced for pristine.

As of the time of writing, futures trading suggests that the Fed will make roughly six 25 basis-point cuts in 2024. Come on! Fed policymakers — who hate to surprise markets — have done little to prime investors for such an easing cycle, so there’s almost no chance that they will start at the meeting later this month. Federal Reserve Bank of Cleveland President Loretta Mester told Bloomberg’s Michael McKee on Bloomberg TV Thursday that “March is probably too early.” After that, the Fed’s rate-setting committee only has six meetings left in the year, and the market is effectively saying the committee will cut at all of them.

That seems unlikely. When policymakers start cutting, they’re going to do so gingerly and watch developments in the data as they do. Here’s how Mester described her cautious approach in Thursday’s interview:

It’s really going to be dependent on how the economy evolves. I think March is probably too early in my estimation for a rate decline because I think we need to see some more evidence. I think the December CPI report just shows there’s more work to do, and that work is going to take restrictive monetary policy.

Even after policymakers start cutting, the odds are reasonably elevated that something will give them pause at some point, prompting them to go on hold for a while. That “something” could be a bona fide reacceleration of inflation (unlikely, in my view) or a hiccup in the data (quite likely). Hiccups happen all the time in macroeconomic data due to the inherent volatility of prices, measurement challenges and other factors.

The most recent report is a perfect example. For all the encouraging signs, shelter, medical care services and auto insurance all exerted upward pressure on the monthly number. These are probably hiccups. Official shelter inflation lags market-based measures, and there are excellent reasons to believe it’s heading lower in the months ahead. Motor vehicle insurance hikes partially reflect the lagged effect of past inflation in autos and parts (i.e., the higher “replacement” costs that insurers pass on to policyholders). And medical care services are measured differently in the CPI than the personal consumption expenditures price index — which the Fed technically focuses on.

But the Fed’s risk-management approach means they won’t be focusing on the good and explaining away the bad. Even if the Fed starts cutting in May, the odds are reasonably high that a few inflation reports between then and December bother them enough to warrant a breather along the way. If I had to guess, these will be short-lived breathers, but the Alan Greenspan Fed of the 1990s shows there’s precedent for policymakers delivering a few surgical cuts but leaving rates elevated for years. I expect three rate reductions in 2024, consistent with what the median policymaker laid out in December’s Summary of Economic Projections. That would imply cuts starting in May and proceeding at a pace of every other meeting.

The other element in all of this, of course, is the labor market. The only reason for policymakers to “rush” rate cuts is if they come to be concerned about the other side of their dual mandate of price stability and maximum employment. At the moment, the data doesn’t give them much reason to be worried. Initial jobless claims fell to 202,000 in the week ended Jan. 6, leaving the four-week moving average at about 207,800 — a level that’s still perfectly consistent with a resilient labor market. Separate data this month showed that the unemployment rate sits at about 3.7%, still close to the lowest levels in decades.

If any of that changes, policymakers could deliver rate cuts with more urgency. But everything we know today suggests that the Fed will move slowly to reduce policy rates in 2024. All told, the inflation data still looks decent — even encouraging. But with markets priced for bolder adjectives — pristine, impeccable, flawless — bonds could yet be in for some volatility in the year ahead.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin