Everyone knows you’re not supposed to bet on a bubble, but what about a potential bubble?

As the S&P 500 Index climbed above 5,000 on Friday, many of us found ourselves wondering what exactly we should call this market: a bubble or a durable new bull? Are we reliving 1995 — when, coincidentally, a previous “soft landing” economy pushed the Dow Jones Industrial Average above 5,000 en route to a 25% annualized return over the rest of the decade — or 1999, when the by-then-flimsy stock market edifice was on the verge of collapse? As is too often the case, it’s hard to know.

The 1990s parallels, of course, seem to pop up everywhere. Just as internet stocks were booming then, the 2023-24 market has been marked by breathless enthusiasm for the potential of artificial intelligence as well as wildly disparate guesses about how the technology will translate into future cash flows. Now, as then, market concentration is high and rising, and one stock encapsulates all of the market’s secular growth dreams and bubble nightmares (today: Nvidia Corp.; then: Cisco Systems Inc.).

Here’s how Newedge Wealth LLC senior portfolio manager Ben Emons framed the 1990s analogy in a note on Wednesday:

The market flocked in 1995 to hot tech stocks like Cisco which is often compared to [Nvidia, or NVDA]. The company was admired for its software and hardware that allow far-flung, otherwise incompatible computer networks to talk with each other and to connect to the Internet.

Cisco skyrocketed and kept burning, and that carried the Dow Jones higher by breaking out of its trading channel once the 5000 level was breached... But if NVDA is like Cisco 1995, then its 41% gain YTD means that we’re just getting started. Cisco clocked over 100% in 1995, after clocking over 100% annualized returns since its IPO in 1987. NVDA is in the exact same momentum stage. Dow 5000 heralded the soft-landing economy where it was about one superstar tech stock contributing significantly to concentration in the indices.

The 17th century Dutch tulip mania is established market lore, and many witnessed the Beanie Babies bubble (or saw the movie). But in practice, the line between durable growth and asset bubbles is often too thin to decipher with a high degree of confidence.

When the Dow hit 5,000 in November 1995, some people were already saying that the market had become too rich. Over the next 13 months, that sentiment only mounted, leading up to Fed Chairman Alan Greenspan’s famous “irrational exuberance” speech in December 1996. But Dow 5,000 wasn’t a top, and neither were Greenspan’s remarks. From the day of the speech to the March 2000 peak of the bull market, the Dow would deliver a 23% compound annual growth rate, the S&P 500 would register an even higher one at 27%, and Cisco would post a 93% annual return. When, exactly, did the rally become a “bubble”? And what does it say about 2024?

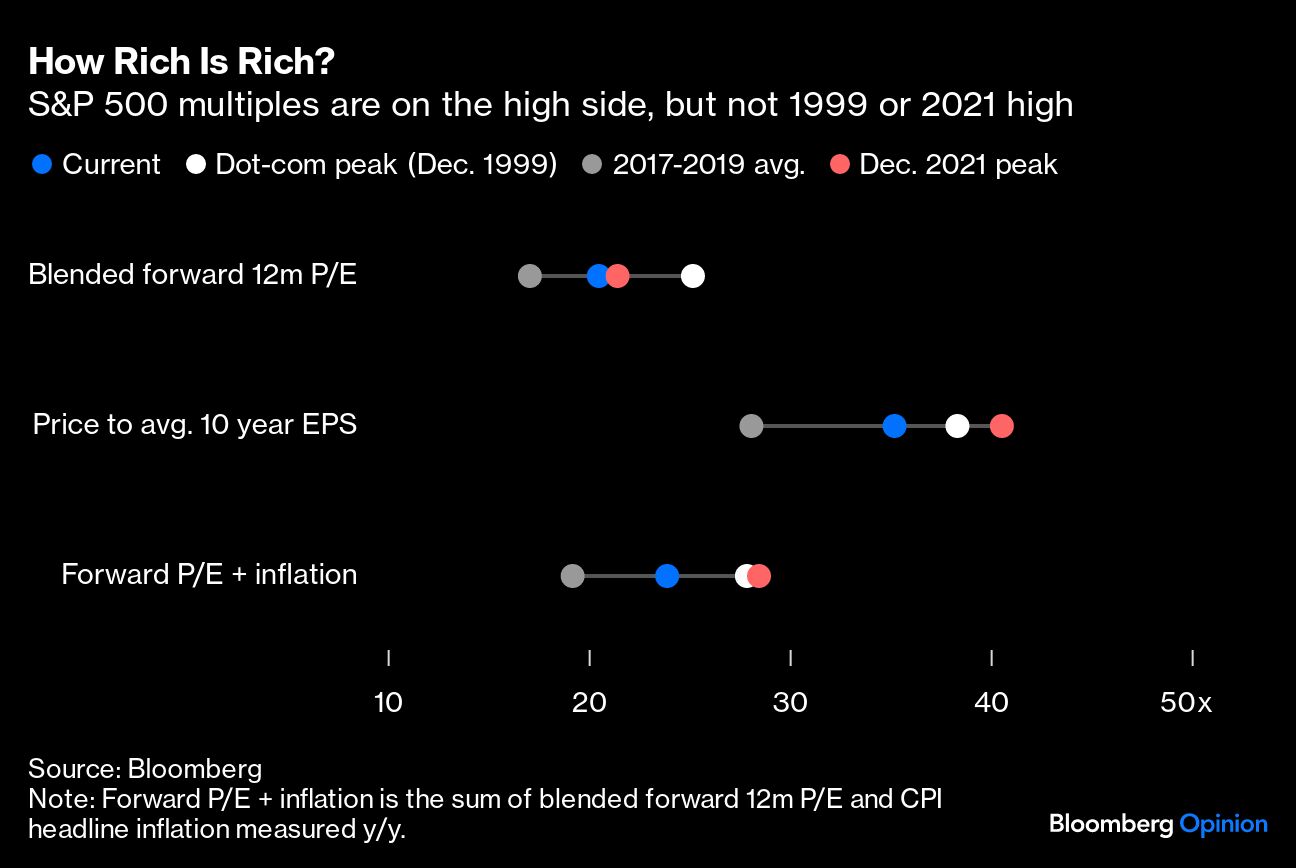

Consider the question of valuations themselves. The usual suite of ratios paints a picture of a somewhat rich market. Multiples are clearly elevated, but not nearly as much as they were in 1999 or 2021.

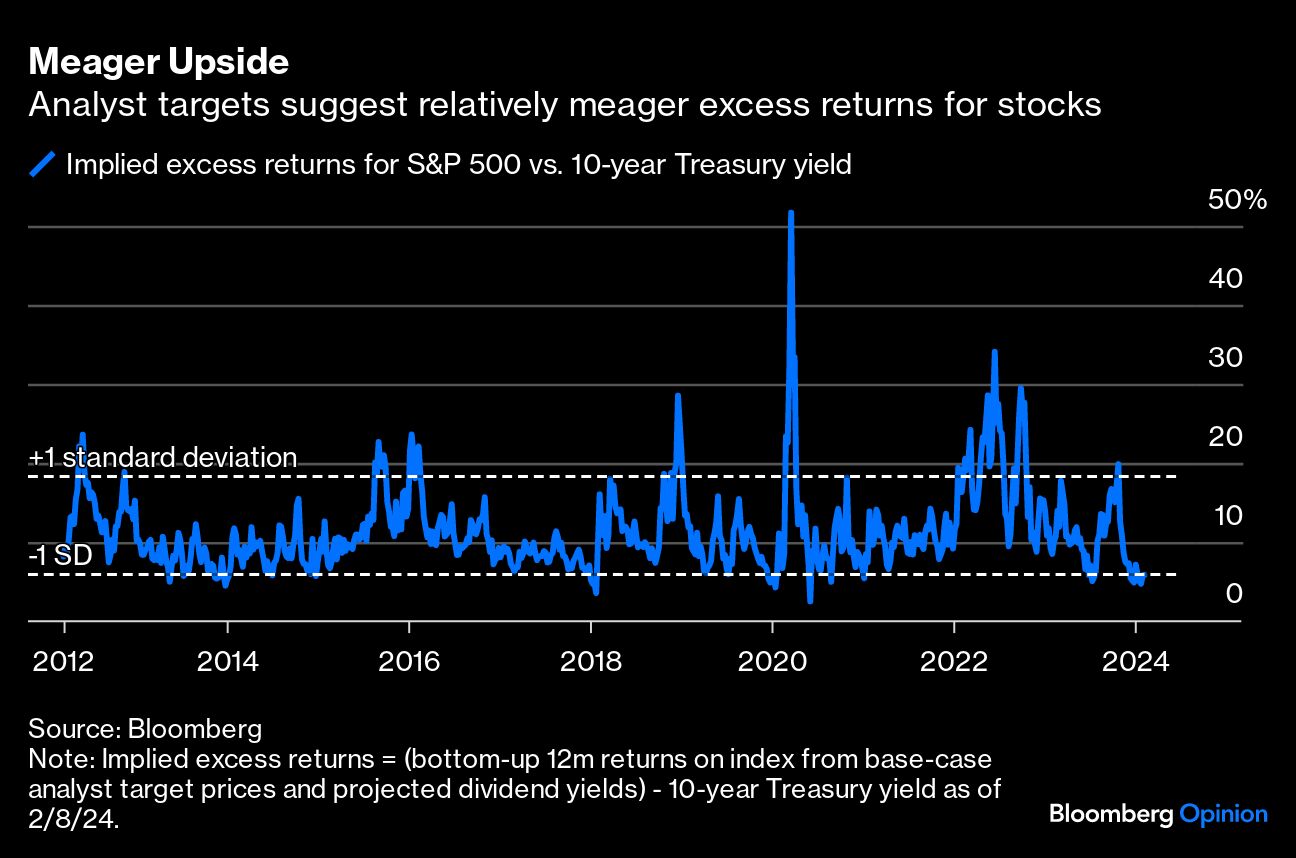

Another way to assess the market is through the prism of sell-side price targets. Many observers (including this one) take such targets with a grain of salt, but there’s something to be said for the work of analysts who put in the legwork to understand a company’s prospects. At the moment, bottom-up sell-side forecasters think the S&P 500 is heading for 5,420 over the next 12 months, an 8.4% implied upside from Thursday’s close. Combine that with the sell side’s projected dividend yield, and it implies a 10% return over the next 12 months — 5.9 percentage points more than the yield on a 10-year Treasury note.

How does that compare with bottom-up projections of upside over time? Admittedly, it’s on the stingy side. The implied excess return on stocks over bonds is about a standard deviation below the average in the time series. But the upside has been this paltry at other moments in the recent past (July 2023; January 2021; September 2020) and the market didn’t implode. In general, those situations rectified themselves in unremarkable ways (a minor short-term correction in July 2023, upward analyst revisions in 2021, and a bit of both in September 2020.) That return also assumes that Nvidia shares will fall about 3% in the next 12 months (based on the consensus Wall Street target, which could get revised sharply after Nvidia reports earnings this month). Incorporate a bullish price target for Nvidia and, all else being equal, it’s easy to envision above-average expected returns for the index. Take a bearish view on Nvidia and the upside narrows sharply. In other words, it’s true that the market is a bit rich and that there’s a lot riding on a single stock, but there are many ways this might pan out.

Of course, there are some short-term fixes to help investors worried about market concentration and high valuations sleep better at night. As I wrote earlier this week in a column about the Magnificent Seven, one of them is owning the equal-weighted version of the S&P 500, which behaves less like a momentum strategy, has relatively average valuations at the moment and has outperformed the market-cap weighted index in times of stress (including the 2000s). In a world without perfect foresight, it’s always wise to manage risk, but avoiding it altogether is a risk unto itself.

No one can say for sure if the market is going to repeat the Dow 5,000 history, and the answer may depend on macro forces that are impossible to foresee. The point is simply that, while there’s obviously peril in knowingly riding a bubble, there’s also a steep price to be paid for skipping out on a growth story that ultimately turns out to be the real deal. We can never underestimate our ability to confuse one for the other.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin