Interest-rate cuts are still in the offing in the US, but you might not think so with the way bonds are selling off after Tuesday’s inflation report. The latest consumer price index reading indicated that core prices — excluding volatile food and energy — rose 0.4% in January from a month earlier, exceeding the median economist forecast. Yields on 10-year notes hit the highest level since November.

The report was very poorly timed. It comes not long after Federal Reserve Chair Jerome Powell said he needed to see more evidence of disinflation to start reducing policy rates, and Tuesday’s report sure didn’t look — at least on the surface — like the sort of evidence required. In reality, there’s a chance that the “January effect” and quirky housing statistics drove most of the miss. There’s still plenty of time for the data to evolve in a manner that makes the Fed comfortable cutting in May.

Let’s start with the excess seasonality.

There’s reason to believe that companies occasionally use the start of the year to raise prices. Just as we do in our personal lives, many business owners have been taking stock of the year that was. They’re looking back at 2023 — and the inflation experience of the past three years — and wondering if they can expand profit margins that may have narrowed due to wage and other cost pressures. Clearly, they’re aware that inflation is ebbing, but they may have decided to try to pass through one last price increase.

Goldman Sachs Group Inc. — one of the few firms to correctly forecast the 0.4% increase in core prices — called this the “January effect” in a note on Monday. Here’s an excerpt from the note from Manuel Abecasis and Spencer Hill:

We expect a temporary boost to core CPI from start-of-year price increases that we have termed the “January effect.” Given last year’s elevated inflation, firms are likely to implement larger price increases as they reset their prices than they normally would when inflation was lower, leading the seasonal factors to underestimate inflation at the start of the year when price resetting is more common.

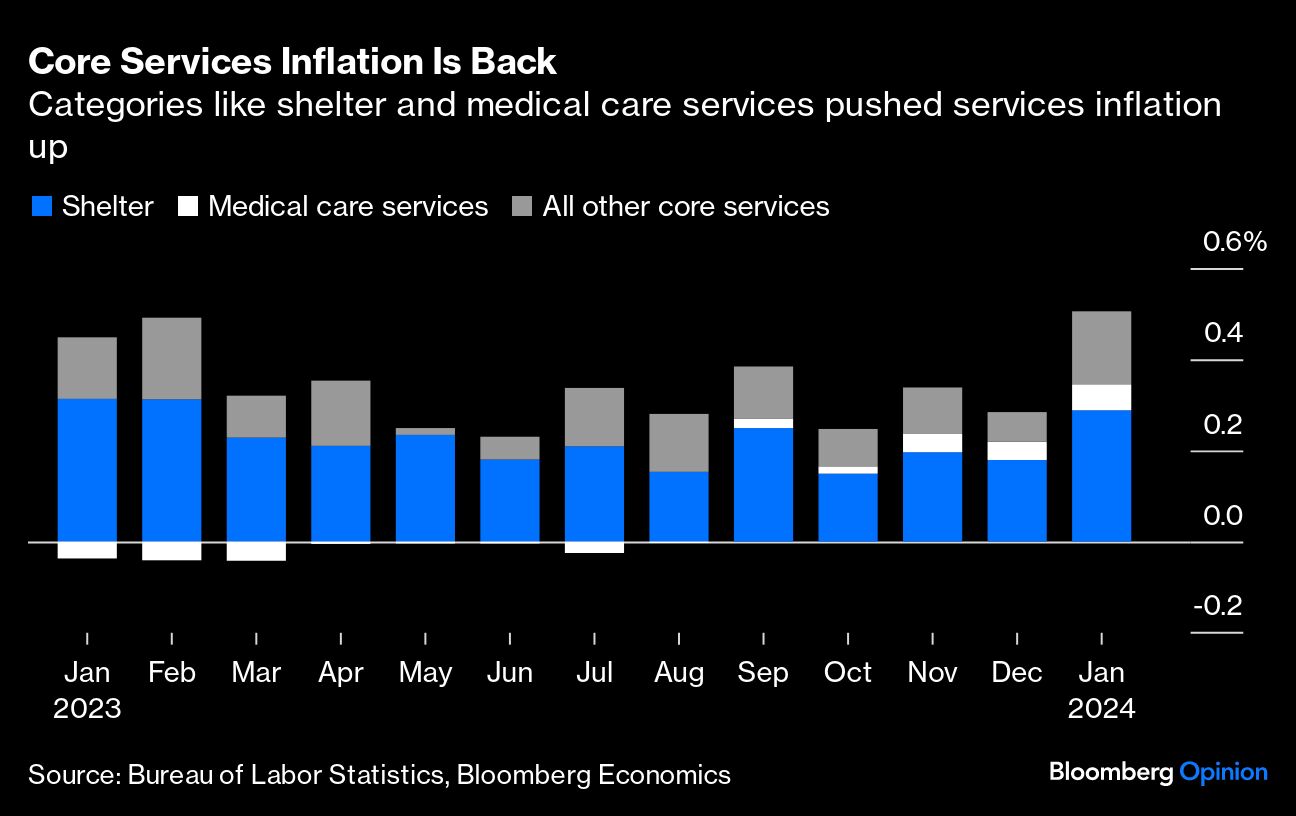

In theory, the Bureau of Labor Statistics’ seasonal adjustment process should compensate for these monthly patterns, but the pandemic economy has wreaked havoc on seasonal adjustments and there’s still a lot more “catch up” price hiking going on today than was common before inflation surged in 2021. That might help explain some of the surprise month-on-month jumps in categories including medical care services (which constitutes 6.5% of the CPI basket) and miscellaneous personal service categories such as hair cuts and dry cleaning. If it abates soon, we’ll know it was a head fake.

The other major factor was shelter, but there’s a silver lining there, too. In its inflation indexes, the government attempts to measure the housing costs of everyone. In practice, the CPI housing basket moves much more slowly than market rents and home prices, because most people’s rents reset very infrequently. Market-based rent inflation has cooled dramatically since early 2022, so it’s still quite reasonable to expect that the CPI “rent of primary residence” category will as well.

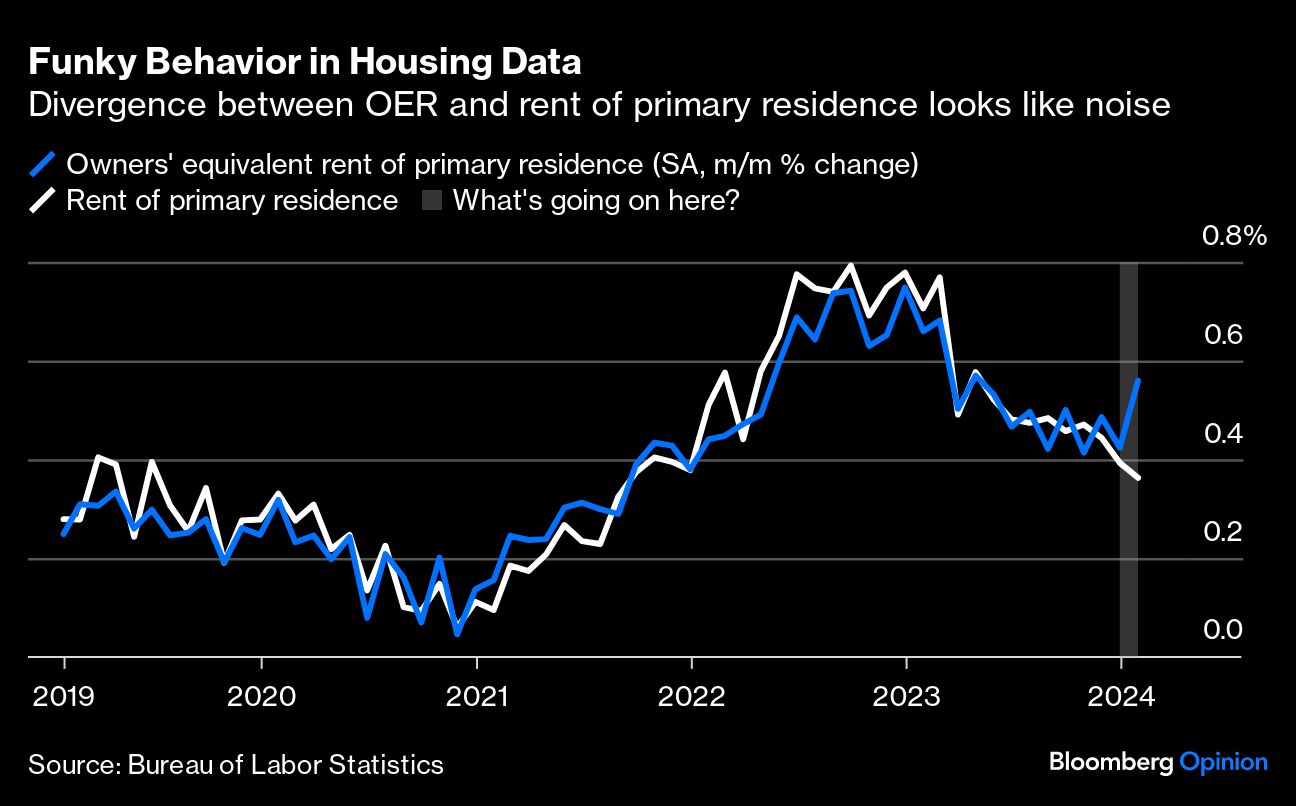

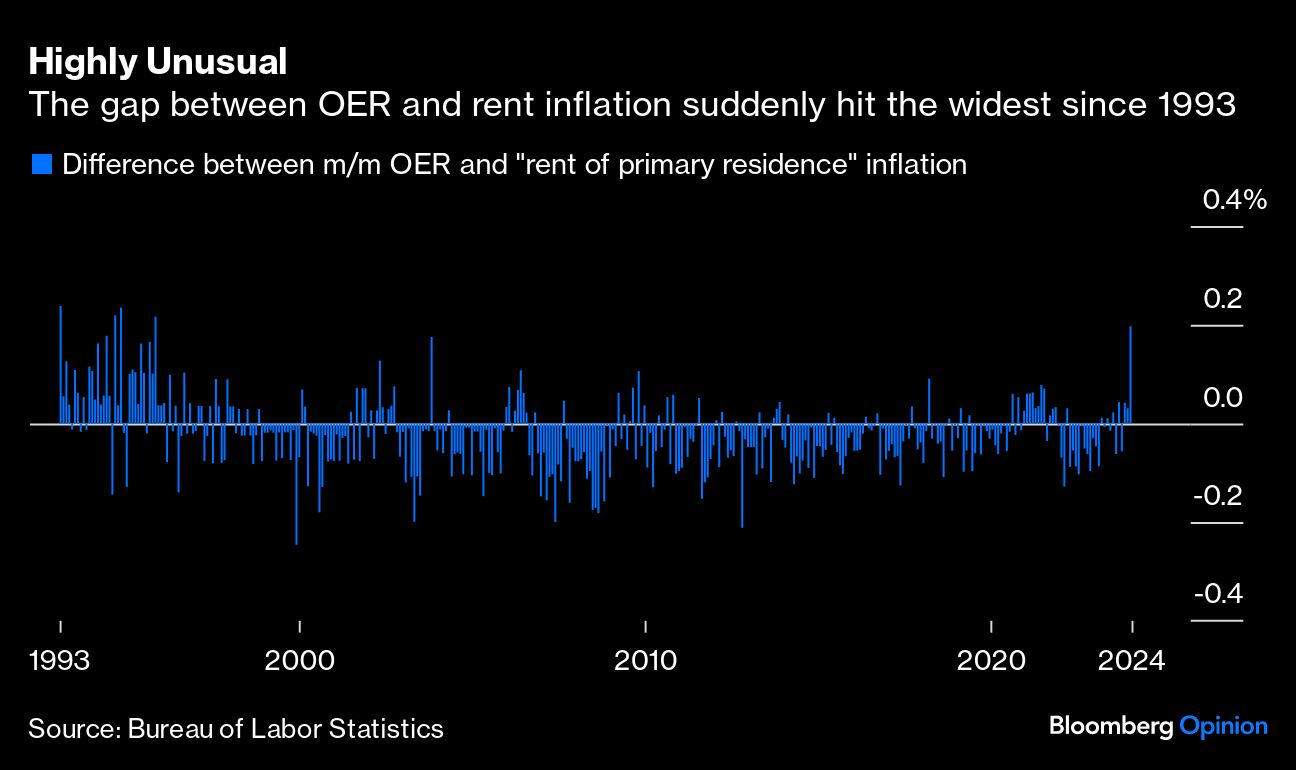

Homeowners’ cost of shelter is a whole other methodological challenge, and BLS attempts to proxy it through a concept called owners’ equivalent rent. It’s mostly based on rents of comparable homes and moves very slowly — so fundamentally very similar to “rent of primary residence.” The key difference is that the BLS also surveys homeowners about how much they think their homes are worth, using this information to help weight OER. What’s highly unusual, though, is that OER inflated much more quickly in the latest reading than the “rent of primary residence” category. I don’t have a great explanation for why this happened, and I’m willing to bet that it’s mostly noise and very little signal.

Long story short: these data points work in mysterious ways on a month-to-month basis, but it’s still relatively clear that more housing disinflation is coming.

Zooming out, it’s possible that none of this will matter. The Fed tends to focus on the personal consumption expenditures deflator when setting policy, and the most concerning categories in January’s CPI — housing and medical services — hit PCE differently. Adjusting the CPI figures for the weighting and conceptual differences in PCE, Morgan Stanley economists led by Ellen Zentner expect core PCE was a more manageable 0.29%. We’ll get further clarity on that on Friday when the BLS releases its producer price index, which helps inform some categories in PCE.

The problem is that the bond market was priced for a run of flawless data that was never going to materialize. At one point earlier this year, futures markets were implying about six rate cuts in 2024. In practice, month-to-month inflation data is filled with quirks, and it was almost inevitable that a few reports would give policymakers pause. I still think that the Fed will get enough evidence from forthcoming inflation reports to start cutting rates at its May meeting. But even then, the inherent volatility of the data means it may well be a slow easing cycle.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Volatility/Downside Protection Topics >