The Federal Reserve will begin a review of its monetary policy framework later this year, including a potential reconsideration of the ways it communicates with the public. Of great interest is the fate of the dot plot, an anonymous collection of policymakers’ interest rate projections that generates considerable attention each quarter on Wall Street.

The dots have many detractors who think that they confuse more than they clarify, and an objectively amateurish release last week — which was marred by a failure to incorporate information into the projections from that morning’s inflation report — should only add to the controversy. But policymakers must focus on improving the dots and ignore those who suggest abandoning them.

Let’s start with what the dot plot tells us. Part of the broader Summary of Economic Projections published quarterly, the dots are an anonymized display of where Federal Reserve Board members and Federal Reserve Bank presidents see rates going. Upon its release, most of the focus turns to the median dot, in part because that’s what the rate-setting committee chooses to highlight in its presentation document. But the median projection is only a small part of the picture — as are the mean and the mode — since the contributors aren’t participants in a pure democracy.

At any given time, only 12 of the 19 contributors to the survey have a vote, and Chair Jerome Powell’s view matters in practice far more than everyone else’s. His inner circle includes the vice chair and the president of the Federal Reserve Bank of New York, so their views matter more, too.

In addition, market participants have to contend with questions around the timeliness of the projections. Last week, for instance, the Fed released a new edition of the dots about 5 ½ hours after a surprisingly good inflation report that should have at least some positive impact on the perceived path of prices and interest rates this year. Powell characterized the numbers as “a better inflation report than almost anybody expected,” yet he also suggested that few people bothered to change their forecasts to incorporate the new information.

For a group of public servants that each employ teams of Ph.D. economists, that is inexcusable. Financial markets move at the speed of light nowadays, and technology has made it possible to update forecasts with just a few clicks (or no clicks at all!), so they had plenty of time. The leaders of the most powerful institution in global markets must demand better than releasing stale information to the public.

The futures market, which had been expecting one cut in 2024 (and slightly better than even odds of another), fully priced in two cuts within minutes of the latest CPI release. Then the dot plot dropped, showing a median outlook of just one reduction this year.

The most plausible argument for not updating the projections after CPI is that policymakers wanted to wait for the release of the producer price index the following day. Together with CPI, PPI allows us to infer the monthly change in the personal consumption expenditures deflator, the Fed’s preferred gauge, with a higher degree of confidence. However, I refuse to accept that a stale forecast is better than a current-but-imperfect one.

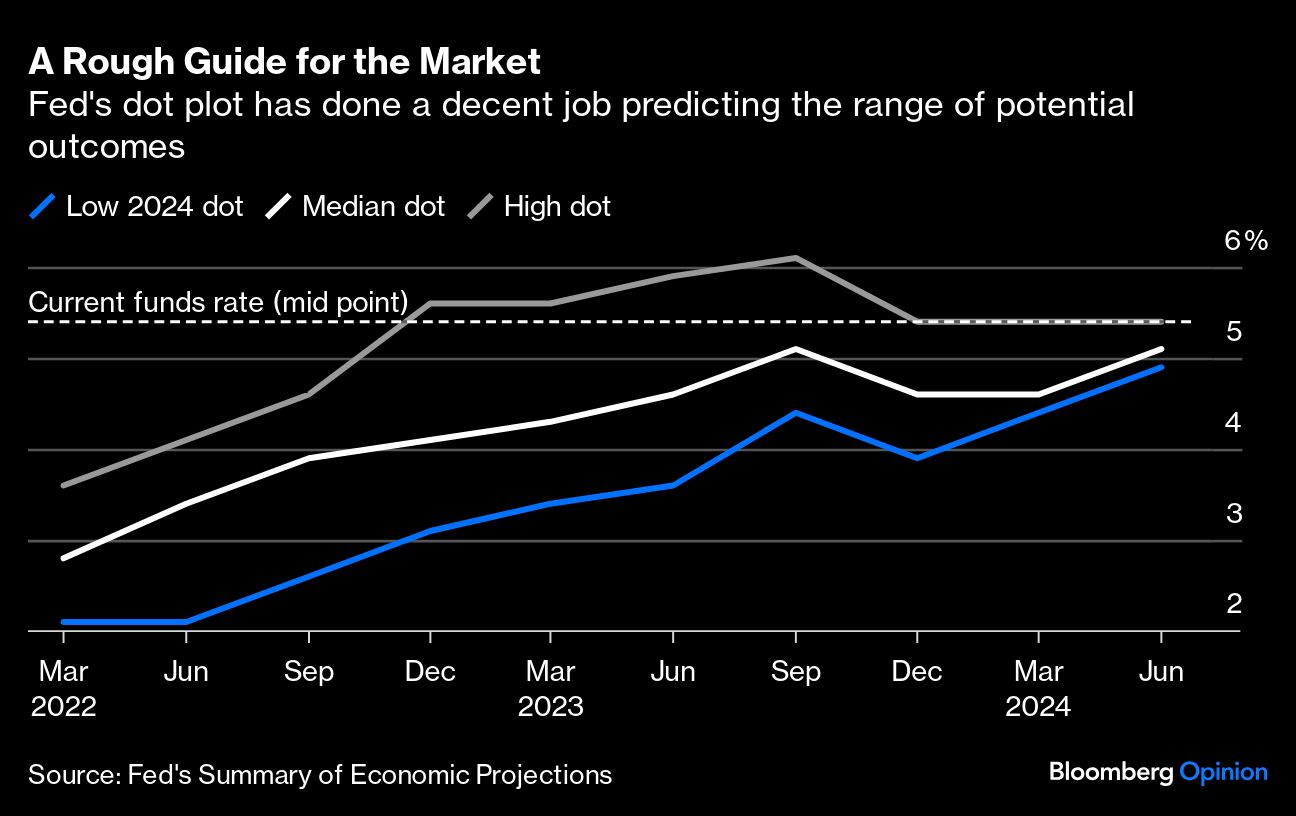

Still, the dots are useful in general, as is the rest of the Summary of Economic Projections. For starters, they provide helpful guiderails that keep inherently volatile markets from getting too far out-of-line. While it’s true that the median projections have been highly imperfect, the dispersion of the dots has underscored the extreme uncertainty of forecasting in recent years.

If you’d been following the evolving range, your expectations for 2024 rates would have been in the right ballpark since around December 2022. If you (incorrectly) treated the median estimate as a binding forecast, then you would of course feel misled. Read the correct way, the concept of the dot plot is consistent with the goals of broadly managing expectations without making explicit promises.

More transparency about which dot is which would make it all more useful. Lifting the veil of anonymity would allow the public to weight the dots and hold the bad forecasters accountable. It would also incentivize contributors to put their best foot forward, instead of putting out dated projections.

Understandably, some people worry that full transparency would risk occasionally embarrassing the chair: The realized policy path could diverge from the chair’s thinking, theoretically undermining his or her leadership. But so be it! If Americans have an autocratic chair (or, conversely, a weak leader with habitually off-base projections), they deserve to know.

This isn’t a new idea, of course. A 2016 Brookings Institution compilation (solicited from academicians and private-sector contributors) considered a range of SEP proposals, including radical transparency and banishing the dots altogether. (It’s worth revisiting that document now, as well as the excellent talk that Brookings hosted Friday to discuss the broader framework review).

But last week’s failure shows why more transparency could make a difference: If reputations are on the line, policymakers and their staffs are more likely to get their homework done on time.

If policymakers simply can’t get on board with radical transparency, the next best thing is to provide more transparency on their reaction functions. You can get a very rough idea of that now by pairing the median inflation with the median federal funds projection. The June SEP suggests, for instance, that rates will fall by 25 basis points to 5%-5.25% this year, conditional upon core personal consumption expenditures inflation running at 2.8% and unemployment hovering around 4%. That tells us something about how the Fed is thinking, even though we — and they — all know that their underlying assumptions might be off base.

Sadly, we don’t know which inflation projections go with which rate outlooks. Even without revealing identities, you could conceivably show the sets of assumptions that belong together. In an independent review of practices for the Bank of England, former Fed Chair Ben Bernanke recommended publication of monetary policy scenarios. As Bernanke wrote, that would allow the public to “draw sharper inferences about the reaction function and thus better anticipate future policy actions.” That could work, too.

What we don’t need is a wholesale scrapping of the Summary of Economic Projections. For decades, the Fed operated with extreme secrecy, effectively communicating through smoke signals as part of a modus operandi that engendered extreme suspicion and distrust. All told, the transparency revolution has clearly been a positive development for an American public that deserves to know how their central bank is thinking. Undoubtedly, policymakers often get things wrong; their communications sometimes miss the mark; and, even when everything seemingly goes right, Mr. Market sometimes does its own thing anyway. Still, the answer is to improve transparency, not back away from it.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin