Thursday’s wildly encouraging consumer price index report shows that the Federal Reserve should be cutting policy rates at its meeting later this month. Unfortunately, they’ll probably keep us waiting until September.

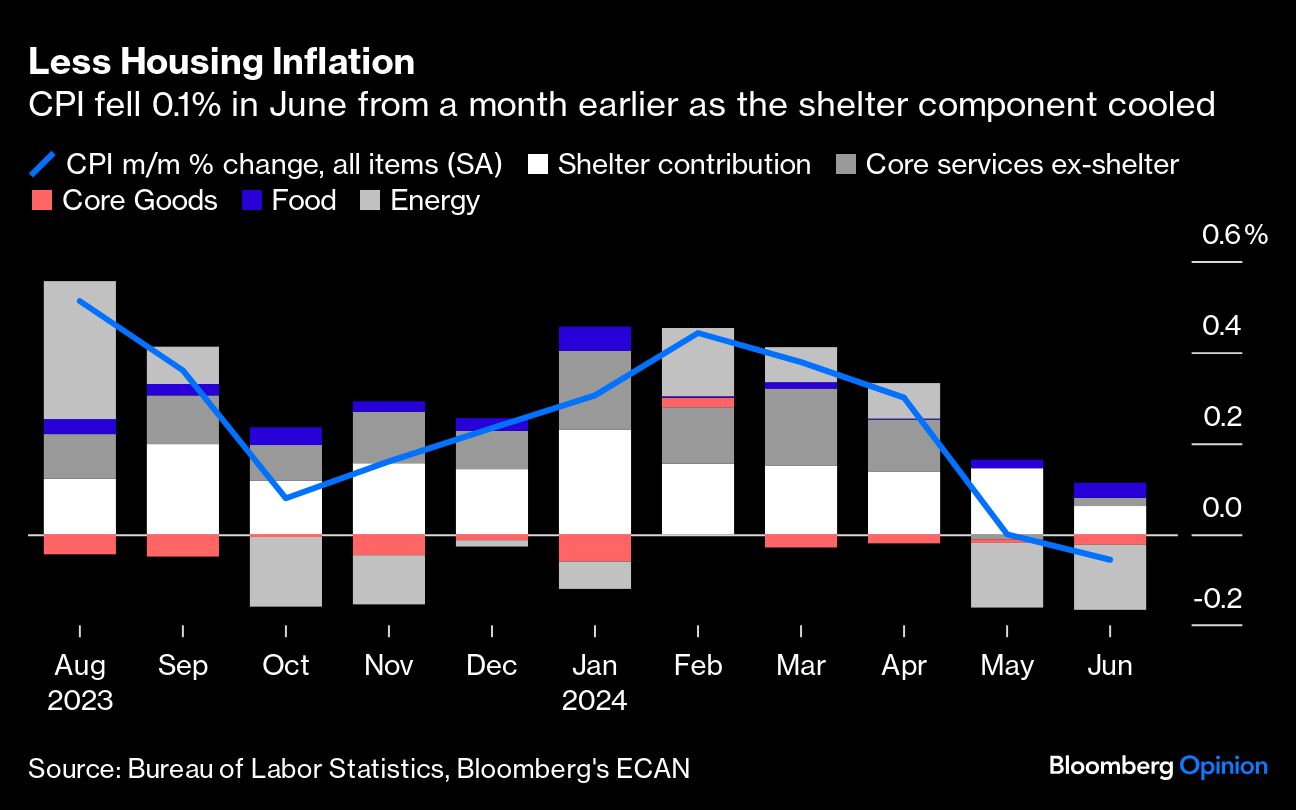

On the inflation front, just about everything seems to be going right. CPI fell 0.1% in June from the previous month and was up just 3% from the same period a year earlier. Primary rents and owners equivalent rent — the heavily weighted and inertial housing categories that have bedeviled the Fed for two years — are finally cooling on what looks to be a sustainable basis. And used car prices are still falling like stones.

The right move is to start lowering policy rates at the next decision on July 31. The Fed has a dual mandate to promote maximum employment and stable prices, and recent developments leave real interest rates tight at a time when unemployment is creeping higher and job growth is slowing. Labor market trouble can snowball quickly and unpredictably once it begins.

A rule developed by my Bloomberg Opinion colleague Claudia Sahm shows that historically, the economy is already in a recession once the three-month average of the unemployment rate rises at least a half percentage point above its low in the past 12 months. At present, it’s up 0.43 percentage point. The argument for cutting now is simple: High inflation appears to be vanquished, so why take risks with the employment side of the Fed’s mandate?

Still, I’m pretty confident that policymakers will wait anyway, as are traders. Fed funds futures now imply just an 8.5% probability of a cut in July but 90% odds of a reduction in September. Fed Chair Jerome Powell probably has a couple of reasons for waiting, but I’d like to offer some counterpoints to each.

First, policymakers feel that they’ve been headfaked by the data before and don’t want to jump to conclusions. As Powell put it in testimony this week before lawmakers, he’s looking for “greater confidence” that inflation is moving sustainably toward the central bank’s 2% goal. Powell’s right that risks remain, but policymaking is full of tradeoffs and it’s worth sacrificing a modicum of “confidence” to protect American jobs.

Personally, I think there are good reasons to expect the volatility in the inflation data to decline. The shelter category is the single-biggest reason that the CPI has remained relatively high recently. It’s a strange and glacial category for which we generally have a lot of visibility through high-frequency housing market data. Now that it’s begun to cool in the CPI, there’s good reason to believe that it will continue to be a moderating force. Overall, the inflation data has now been encouraging for three straight months and most of the past year, with the notable exception of the rocky first quarter. The January-March data now clearly looks more like noise than signal.

Communication is the second reason policymakers may give for delaying rate cuts until September. It’s conventional wisdom that policymakers must never surprise the markets lest they contribute to volatility. Fed officials have been talking about “higher for longer” rates for so long that they’ll likely want to spend the next policy meeting signaling a change in posture. They’ll probably do so by altering the language in the policy statement on July 31; with Powell’s remarks at his press conference; a parade of speeches from Fed governors and reserve bank presidents; and perhaps a major dovish Powell speech next month in Jackson Hole, Wyoming.

Policymakers give markets too little credit. Investors simply don’t need this months-long ritual to understand that circumstances have changed, and the time has come to start a rate cut cycle. Putting American jobs at risk in the name of preserving this bizarre tradition would just be wrong.

I will happily acknowledge that a September cut probably isn’t the end of the world. As much as I worry about the labor market, recent upticks in unemployment have come largely from entrants and reentrants, not layoffs, so I don’t think we’re quite on the cusp of a vicious cycle. An imminent recession certainly isn’t my base-case assumption. This is an economy unlike any other, and even Claudia Sahm has acknowledged that her rule “could go wrong this time.” Lastly, markets are forward-looking, and the 10-year Treasury yield (a benchmark for mortgages and other household and corporate borrowing) was down 10 basis points on Thursday alone at the time of writing — a form of easing in and of itself.

But there are always hidden vulnerabilities when you have the policy rate at a two-decade high, and the real question for policymakers is: Why risk it? The proverbial soft landing is here for the taking right now, so why not land the plane and cement this Fed’s spot in the history books?

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin