Human nature is such that there are always some folks who put a negative spin on obviously good news. So as we head into the time of year when companies report their results for the second quarter, and with members of the benchmark S&P 500 Index projected to post their best earnings growth in two years, some are saying this is somehow a bad thing because “expectations are too high.” The implication is that there’s no way the economy is that strong, and investors are sure to be disappointed.

Consider the possibility that expectations are high for the right reasons. Based on bottom-up earnings projections compiled by Bloomberg Intelligence, S&P 500 earnings are forecast to grow 9.1% from a year earlier on revenue growth of 4.4%. It’s hard to describe those numbers as being a stretch in an environment of solid (if slowing) economic growth. The stock market isn’t the economy, of course, but nominal gross domestic product probably grew about 5.5% in the April though June period from a year earlier, so the revenue projections easily pass the macroeconomic smell test. Add to that the confluence of individual juggernauts that have propelled the broad market for several quarters with no sign of slowing, including Eli Lilly & Co., the maker of weight loss drugs, and Nvidia Corp., which still has the market for advanced chips cornered amid a boom in generative artificial intelligence.

But the single biggest reason for optimism may actually be the unloved stragglers.

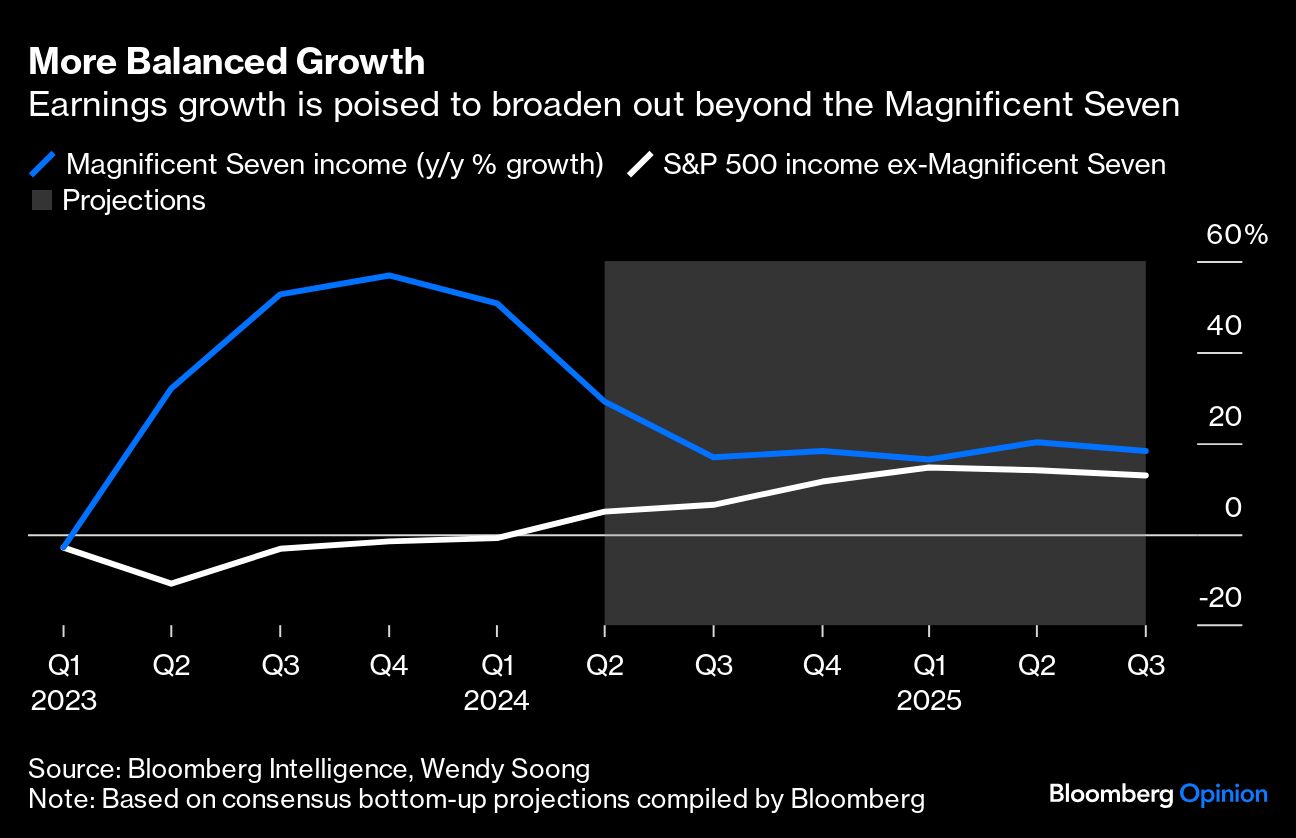

What’s been striking the last couple of years is how a few large firms — the so-called Magnificent Seven — have carried both S&P 500 earnings growth and stock performance. Bears bemoaned narrow earnings breadth as a sign of a market that looked good on the surface but was troubled under the hood. What we’re starting to see now, though, is a broadening of earnings growth to such areas as ground transportation and energy, which could help broaden the stock market’s performance as well. The Magnificent Seven are estimated to report earnings gains of around 29% from a year earlier (still fast, but a bit slower for them), while other stocks in the index are forecast to start growing profits again. Sounds like a balanced and reasonable earnings mix to me.

Morgan Stanley Investment Management senior portfolio manager Andrew Slimmon is one who says the market may be at a positive inflection point. Here’s Slimmon this week on Bloomberg Television’s “The Close”:

This lack of breadth recently means there are a lot of companies out there that have had very good fundamentals but have actually not done much recently because everyone’s so focused on AI. So I think the setup in the second quarter earnings is really good, because it’s an opportunity. I’m not saying run out and sell your AI stocks, but look at companies that are fundamentally doing well that have kind of not done much recently.

Earnings are famously a rigged game. Expectations are usually managed down by companies in the weeks before a season begins, so that companies don’t just meet, but exceed the new, lowered consensus. But DataTrek co-founder Nicholas Colas noted in a report this week that estimates have stayed unusually steady in the runup to this earnings season, which could be a bullish sign. “It means companies didn’t pester their analysts to cut estimates this quarter,” wrote Colas, who was a company analyst himself in the 1990s. “That’s exactly how it works.” In other words, companies are confident they can beat the bar that was set for them.

As sanguine as I am about earnings, index valuations certainly appear rich. At nearly 22 times blended forward earnings, the index is trading at multiples last experienced in 2021, driven to a significant degree by the big AI companies. If they disappoint the market, the punishment could be severe.

But we’ve been talking about this very same threat for about 18 months now. The fact is, great narratives like the AI story tend to unravel in unpredictable ways, and I doubt that this one’s undoing will start with mismanaged earnings expectations in the summer of 2024. If that were the case, the rumblings of trouble would have been here already. Even if one of the market’s superstars falters, there is always the prospect of Federal Reserve interest-rate cuts to underpin equities. No one knows for sure when the first cut is coming, but it’s bound to unleash at least a temporary wave of investor enthusiasm, no matter how much it’s claimed to be “priced in.”

All in all, that feels like a pretty decent backdrop for earnings season, and I’m not too worried about the supposedly high expectations. Sometimes it’s fine to simply take a positive outlook at face value.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin