Regulators and investors have always had a keen interest in the trades that corporates executives and board members make in their companies’ own shares. The government has to look out for the integrity of financial markets, of course, while investors are eager to ride insiders’ coattails. Unfortunately, it’s never been easy to read the insider tea leaves.

Case in point: A new paper by an influential research group finds that insider trades that are disclosed in an opaque fashion are often, suspiciously, among the most lucrative. When insiders disclose their trades to the Securities and Exchange Commission, they’re often — but not always — coded with a “P” (for purchases) or an “S” (for sales). Any armchair regulator can figure out that something’s fishy when S transactions accumulate just before a negative piece of news that moves the stock. Alas, it’s frequently more complicated than that.

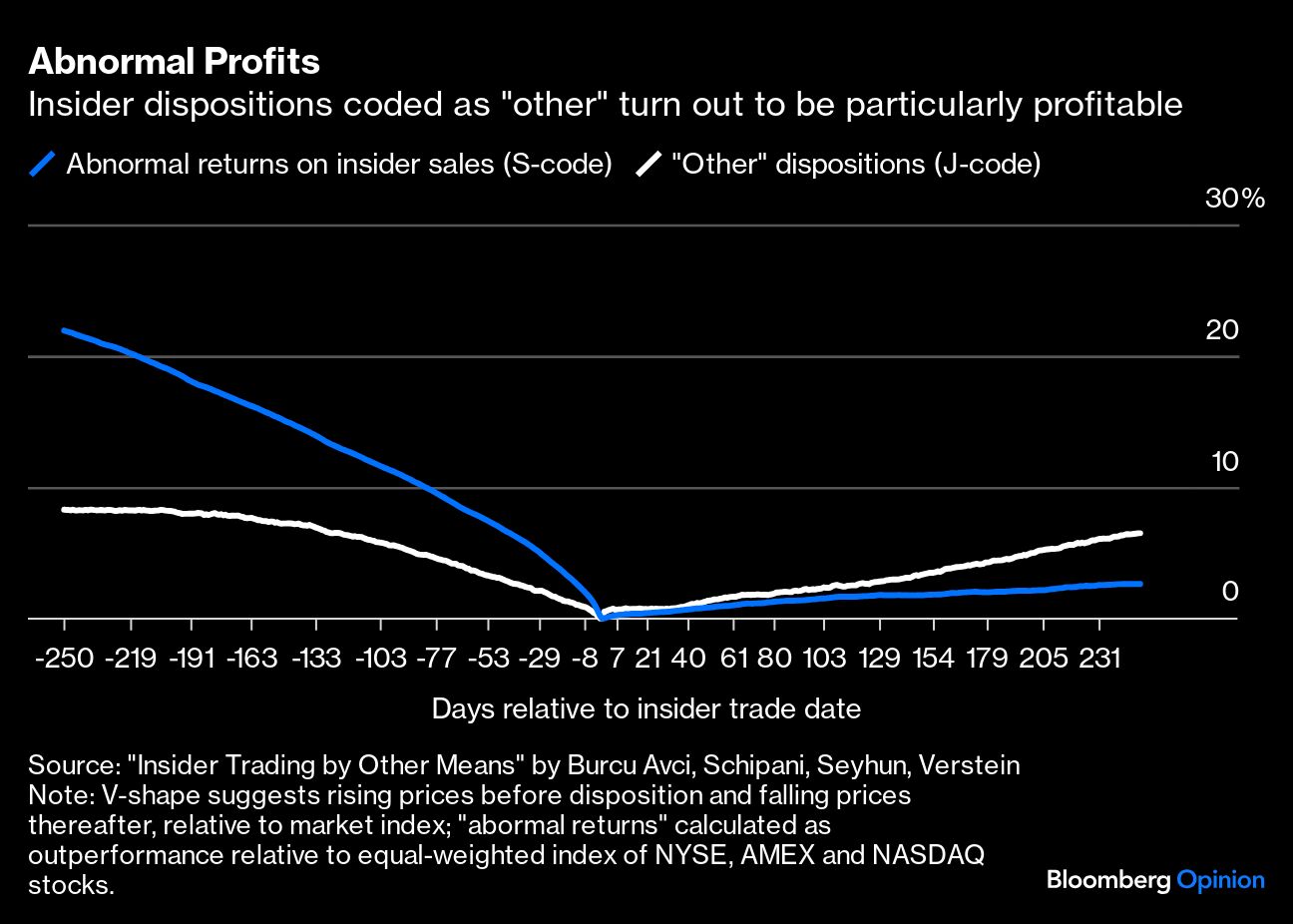

In fact, it turns out that the most profitable trading by insiders doesn’t involve S-coded trades at all, but is instead filed under the umbrella term of “other” dispositions (those with the J code) — a discovery that the researchers suspect is consistent with deliberate and widespread efforts to confuse people and avoid scrutiny.1 According to “Insider Trading by Other Means,” insider trading involving J-coded share dispositions meaningfully outperforms the market, and seems to be on few people’s radar. The J-coded trades amount to more than $3 trillion in the sample period and are “mentioned in essentially no criminal indictments, civil complaints, news articles or scholarly papers,” write authors Sureyya Burcu Avci, Cindy A. Schipani, H. Nejat Seyhun and Andrew Verstein. In essence, those profiting from inside information may have found a loophole in the trading disclosure rules that allows them to evade SEC scrutiny.

The key findings are summarized in the following graphic (replicated here courtesy of the authors). It shows what would happen if an investor tracked insiders’ sales and sold on the day of an “other” disposition, reinvesting the proceeds in the market index. The logic is that V-shaped graphics indicate that the shares were transacted near peak prices relative to the market index. The graphic also shows that the effect was significantly more dramatic for J-coded dispositions than for plain vanilla insider sales.

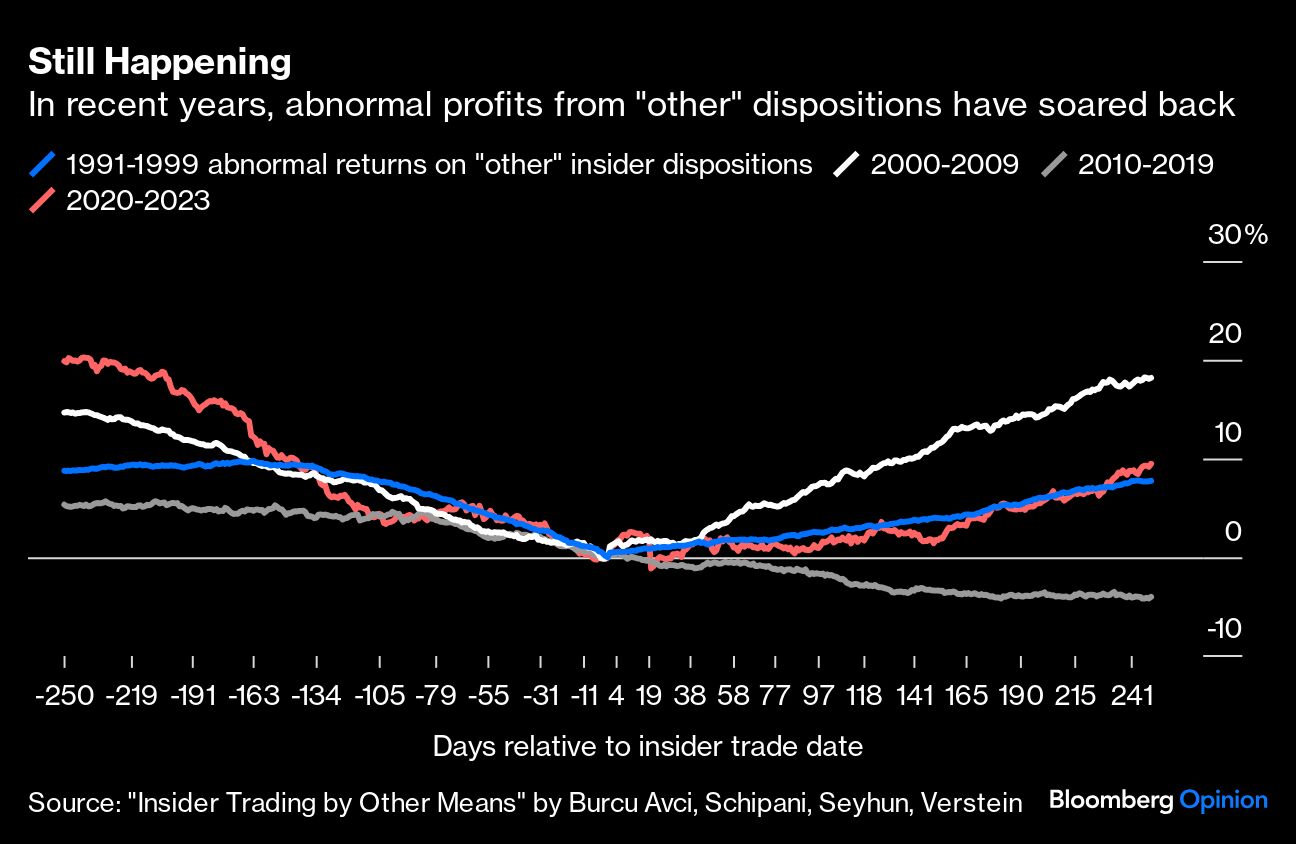

The paper covers a sample period from 1991-2023, but the data also show that the insider outperformance remained quite noteworthy in recent years.

So what does it all mean?