The US stock market has given us plenty of real and perceived calendar anomalies to think about. There’s the observed tendency for stocks to experience a “Santa Claus rally” (during the last five trading days of the year and the first two of the next) and the weekend effect (where stocks have a habit of slumping on Mondays). Yet perhaps no period is as feared as September. Famously, it’s the month in which the South Sea Bubble burst in 1720, stocks collapsed as Britain left the gold standard in 1931 and the S&P 500 Index tanked in 2008 on news of the Lehman Brothers bankruptcy.

There’s no question that there’s something to the September anomaly. But beyond the most extreme anecdotes, the question is whether it should matter to the 99.9% of us not running quantitative hedge funds fine-tuned to exploit market quirks and inefficiencies. I’d say probably not.

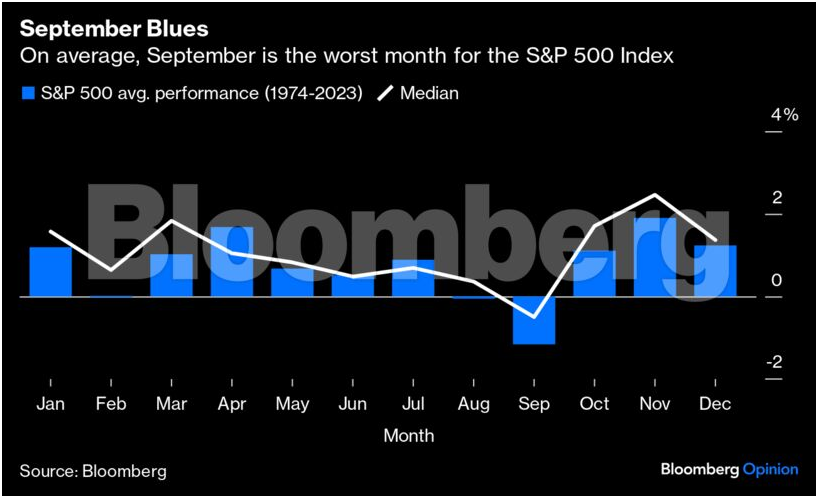

Of the past 50 Septembers, the S&P 500 has fallen 28 times (56%) — just a little worse than a coin flip. Granted, the market has only fallen 38% of the time in the other 11 months of the year, but early autumn has given investors plenty of reasons to stay invested as well. Key recent examples include September 2010 (+8.8%, the best month of that year) and the very respectable Septembers of 2012, 2013, 2017 and 2019. And many of the very worst September routs — not counting 2008 — were followed by large bounces in October. Market participants try to outsmart the calendar at their own peril.

In general, the 50-year average performance in September (-1.2%) is a lot worse than the median (-0.5%), a sign that our data is affected by a few outlier episodes. Indeed, many of the worst Septembers came when we were already clearly in a bear market, which we’re not today. September 1974 comes to mind, as do the Septembers of 2002, 2008 and 2022. Rare are the September 2000-like examples of markets that were cruising along near all-time highs when September came along and sent stocks careening. If you can tell me where the market is heading overall, I’ll tell you how September will play out — but good luck with that!

In an efficient market framework, empirical regularities and market “rules of thumb” are generally thought to disappear once everyone knows about them. Yet calendar anomalies have persisted and been on the market’s radar for at least eight decades, dating back to Sidney B. Wachtel’s 1942 paper “Certain Observations on Seasonal Movements in Stock Prices.” But the effects seem to wax and wane over time, and I’ve yet to encounter a tidy and incontrovertible explanation for why they should persist indefinitely.

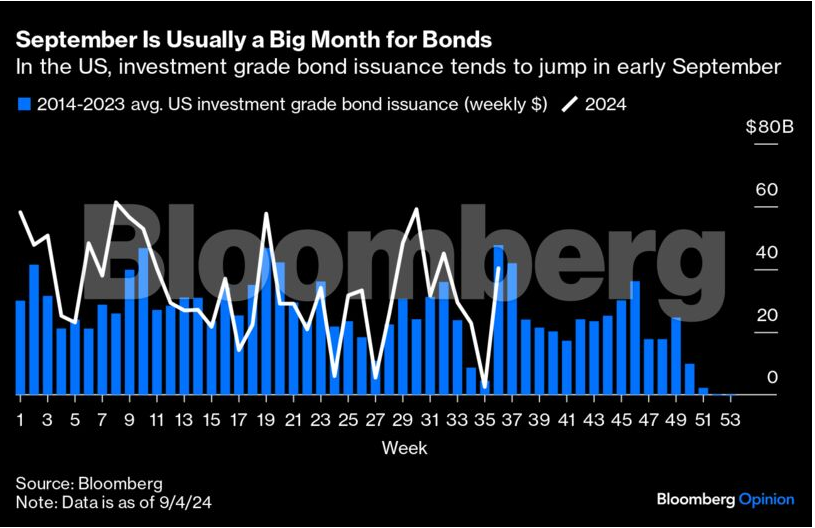

One popular theory for the September effect is that investors tend to sell stocks to participate in the flurry of bond offerings that usually come at that time of year. On average over the past decade, the first week of September (week 36) has been the single biggest week of the year, and the next week isn’t far behind. In 2024, September is once again off to a noteworthy start, with a record number of blue-chip firms hitting the market on Tuesday, including Ford Motor Credit Co. and Target Corp. Bloomberg’s Michael Gambale has reported that companies may sell $125 billion of US high-grade bonds this month, according to an informal survey. Still, September isn’t that unique from other heavy-issuance months, so it couldn’t single-handedly explain the seasonal effect.

Others have argued that the September effect stems from our summer vacation schedules. Under that theory, one may believe that bad news and rumors percolate through the market more slowly when everyone’s at the beach. Once traders return to their desks, they may feel overwhelmed by the onslaught of negative developments they learn about around the proverbial “water cooler” and rush to update their priors.

In their paper “Inattention as a Limit to Arbitrage: Evidence from School Holidays,” Lily Fang, Melissa Lin and Yuping Shao document a version of the effect around the world after different countries’ respective school breaks. But if it’s our July-August inattention to negative rumors that’s historically made the arrival of September feel so abrupt and violent, why should we expect the effect to continue in the age of social media? I know plenty of folks today who spend more time gossiping on X and other platforms when they’re on vacation — not less.

A third theory posits that the September blues are actually a symptom of seasonal affective disorder, as the arrival of autumn brings fewer hours of daylight and bums investors out. If you believe that, one extremely fun paper by David Hirshleifer, Danling Jiang and Yuting Meng goes further to explore the different “mood betas” of stocks. As their work suggests, some stocks may be more susceptible to these effects than others. Of course, this idea hinges on the notion that markets will remain fundamentally human, even in an era when computers do so much of the trading.

Readers of this column will remember that I’m basically a Jack Bogle acolyte who believes that the best investing strategy for most people is to contribute consistently over time to a broad market fund and stay invested. If you try to get cute and outsmart the calendar, you often just end up shooting yourself in the foot (with fees, taxes and missed opportunities). At the end of the day, I understand why the September effect has come into focus again after an extraordinary two-year run in US stocks that pushed the S&P 500’s valuation beyond historical averages. I also know that investors have well-placed concerns about a softening in the labor market. I’m just not sure that the September effect is what will spur very many people into action.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin