Consumer staples are one of the sleepiest sectors of the US stock market. Investors buy them for their low volatility and generous dividends, not exhilarating upside potential. But lately, toothpaste, bleach and certain big-box food retailers seem to be acting like the new semiconductors.

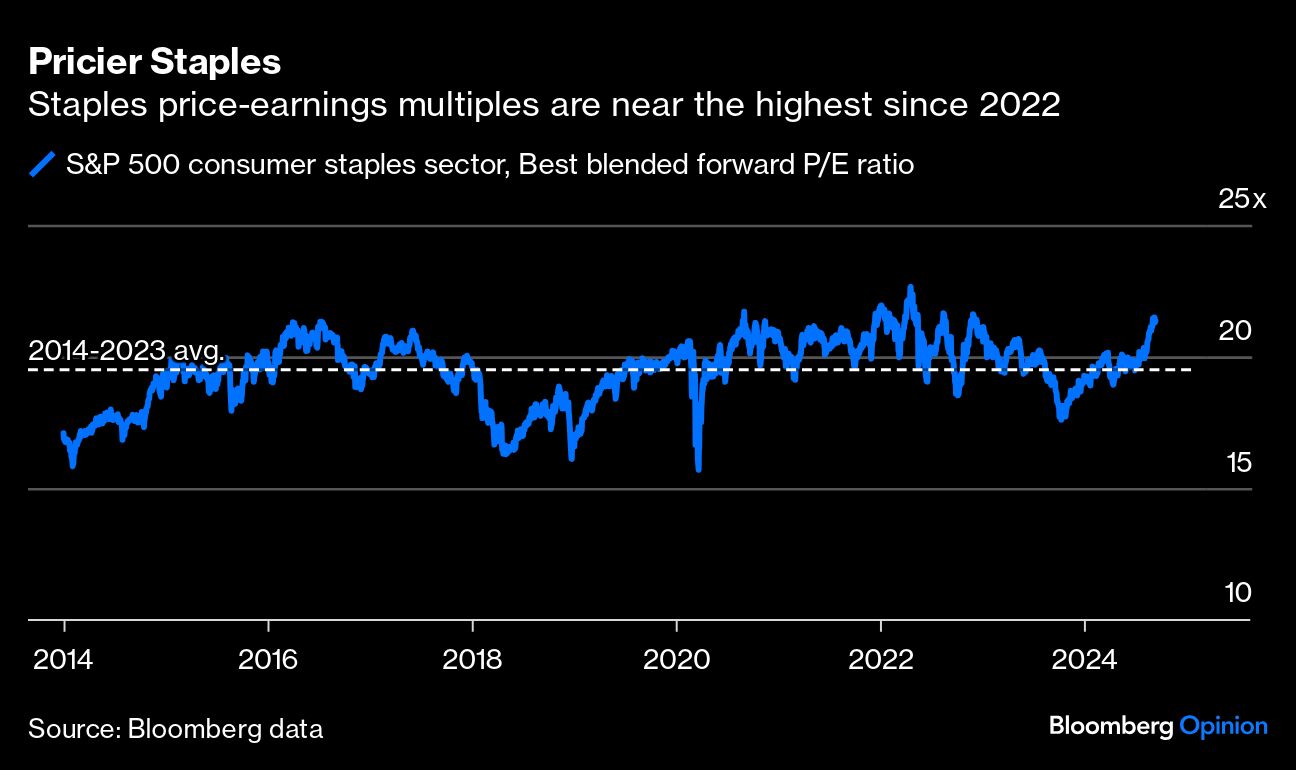

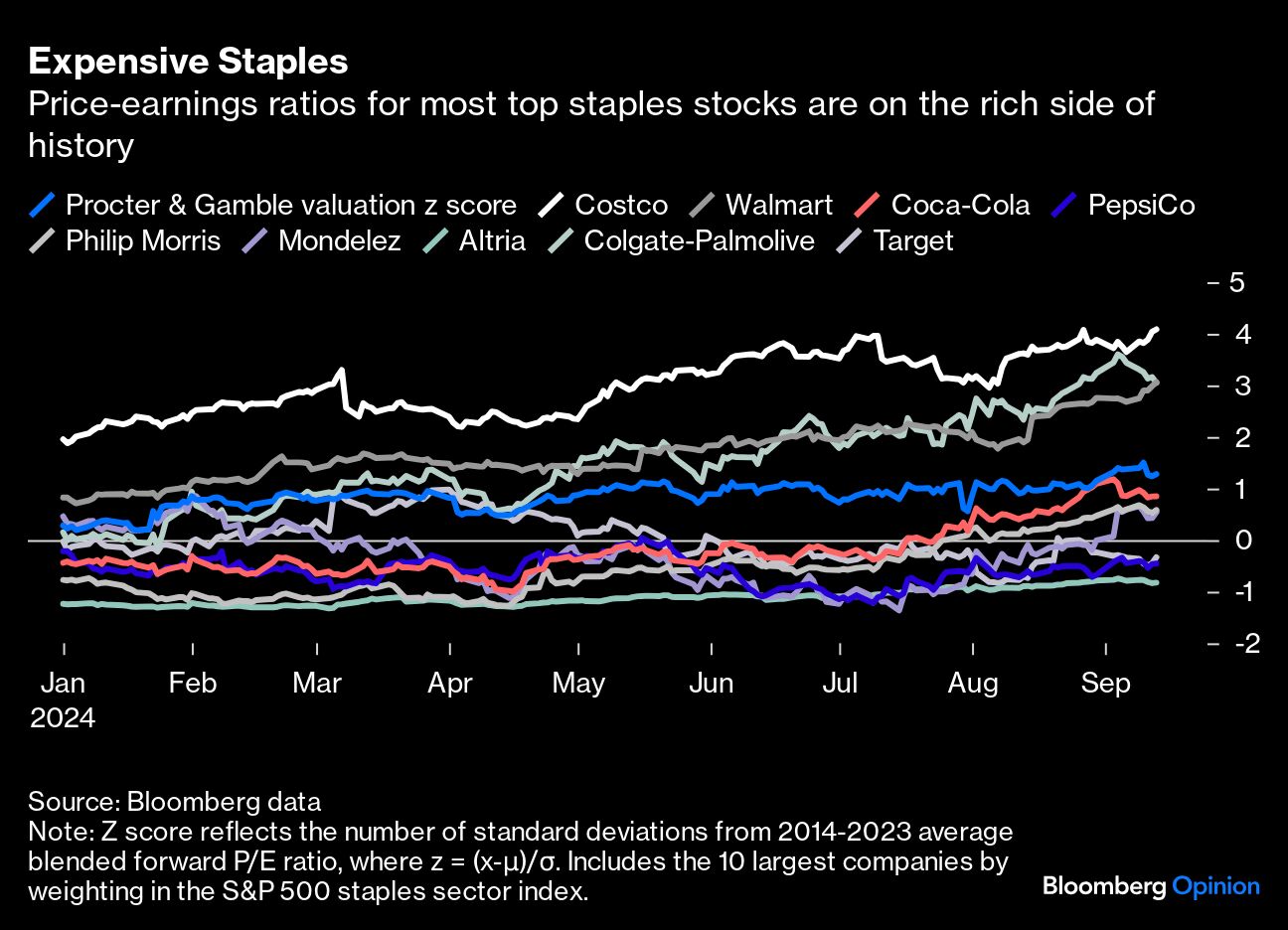

The S&P 500 consumer staples sector has returned 19.8% year to date, pushing the blended forward price-earnings multiple to 21.5 at the time of writing, near the highest since 2022. Some of that reflects optimism around juggernauts including Costco Wholesale Corp. and Walmart Inc. — which command multiples of 51.2 times and 30.8 times forward earnings, respectively — but the frothiness extends to other parts of the diverse super-sector as well.

Colgate-Palmolive Co., Procter & Gamble Co. and Coca-Cola Co. now trade at 27.9 times, 24.7 and 24 times blended forward earnings. Those multiples are 3, 1.3 and 0.8 standard deviations above their 2014-2023 averages — not 2021 meme-stock expensive, but certainly expensive on their own terms.

And this is a relatively recent phenomenon. Staples valuations exploded upward in early August, propelled by the sense that the economy was shifting from “very good” to “so-so.” Data since then has revealed that the unemployment rate, while still low, is generally on the rise. Meanwhile, Nvidia Corp., the superstar stock of the 2022-2024 bull market, failed to deliver the magnitude of earnings surprise that markets had grown to expect. As a result, the S&P 500 semiconductor sub-industry has deflated to a 28.4 times forward P/E ratio, after a 90% rally from late 2023 pushed industry multiples as high as 36.1 times.

That being the case, it made sense to seek a degree of safety in companies with steady cash flows and high dividend yields that are less sensitive to economic cycles, part of what we in the commentariat labeled the Great Rotation. To be clear, I’m not saying that staples are literally pricier than semiconductors (they’re not), but they’re certainly rich for what they are. Since the end of July, Nvidia has returned just 1.8%, while Walmart has returned 17.8% and Costco is up 11.4%. The question now is whether staples are still really safe if you buy them, in some cases, near multi-decade-high valuations.

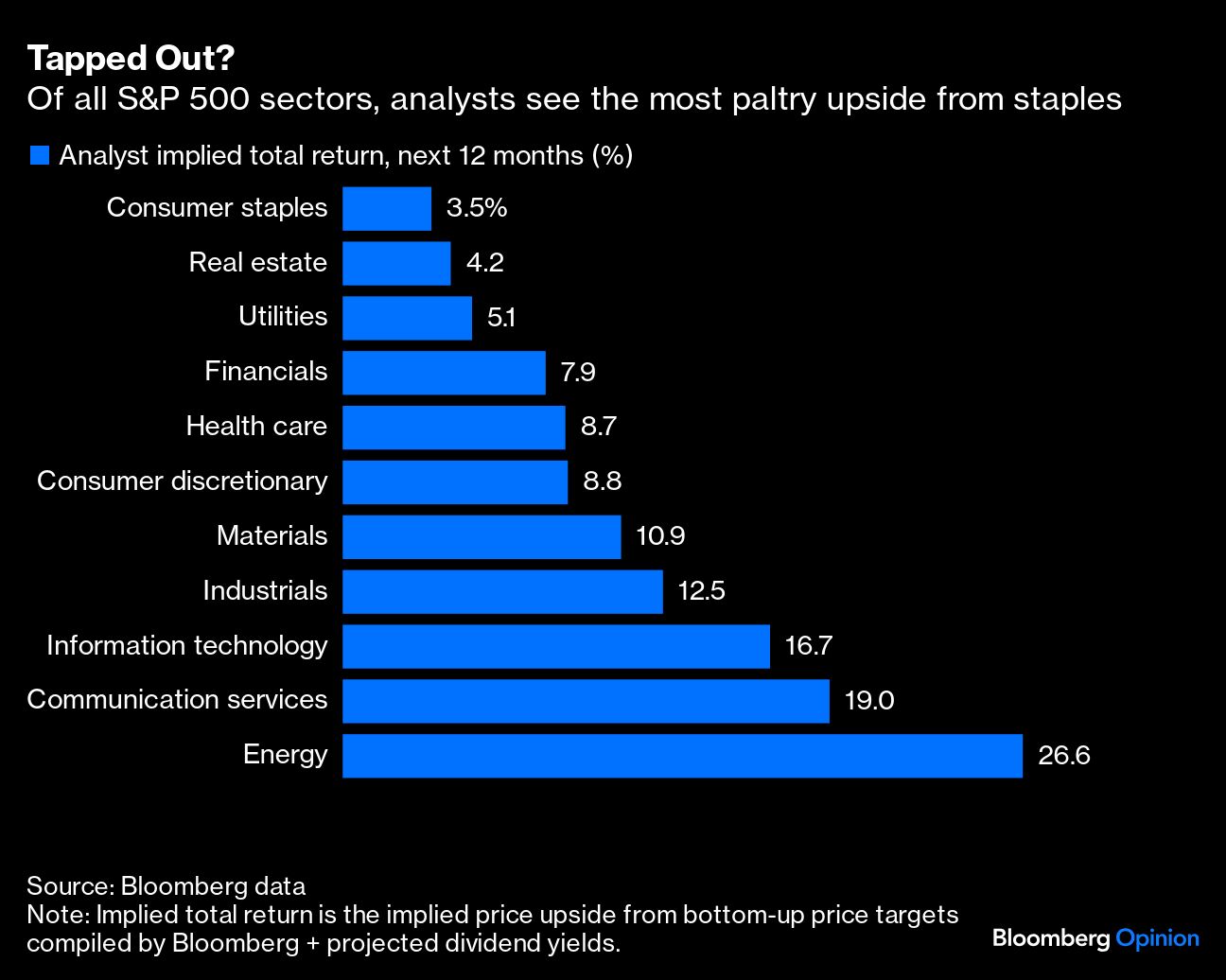

Sellside analysts seem to be struggling with the same riddle. Based on consensus price targets aggregated by Bloomberg, the market-cap weighted S&P 500 consumer staples index may rise just about 1% in the coming 12 months. Adding the projected dividend yield of 2.5%, Wall Street is projecting a 3.5% total return, the most paltry of any sector. That’s fine if it plays out like that, but you can do better in a 12-month Treasury bill without the risk. To prefer staples, you’d have to believe that there’s some hidden bull case that analysts are missing, and I just don’t see it.

The most exciting action is in the likes of Costco, which is hiking membership prices, and Walmart, which is capturing more affluent customers. Yet as my colleague Andrea Felsted told me recently, many of these retail companies are finding it harder in general to push through price increases, instead discovering that they often have to offer more promotions to keep increasing sales volumes, which weighs on profitability. The sky is not the limit, at least not at this point in the economic cycle.

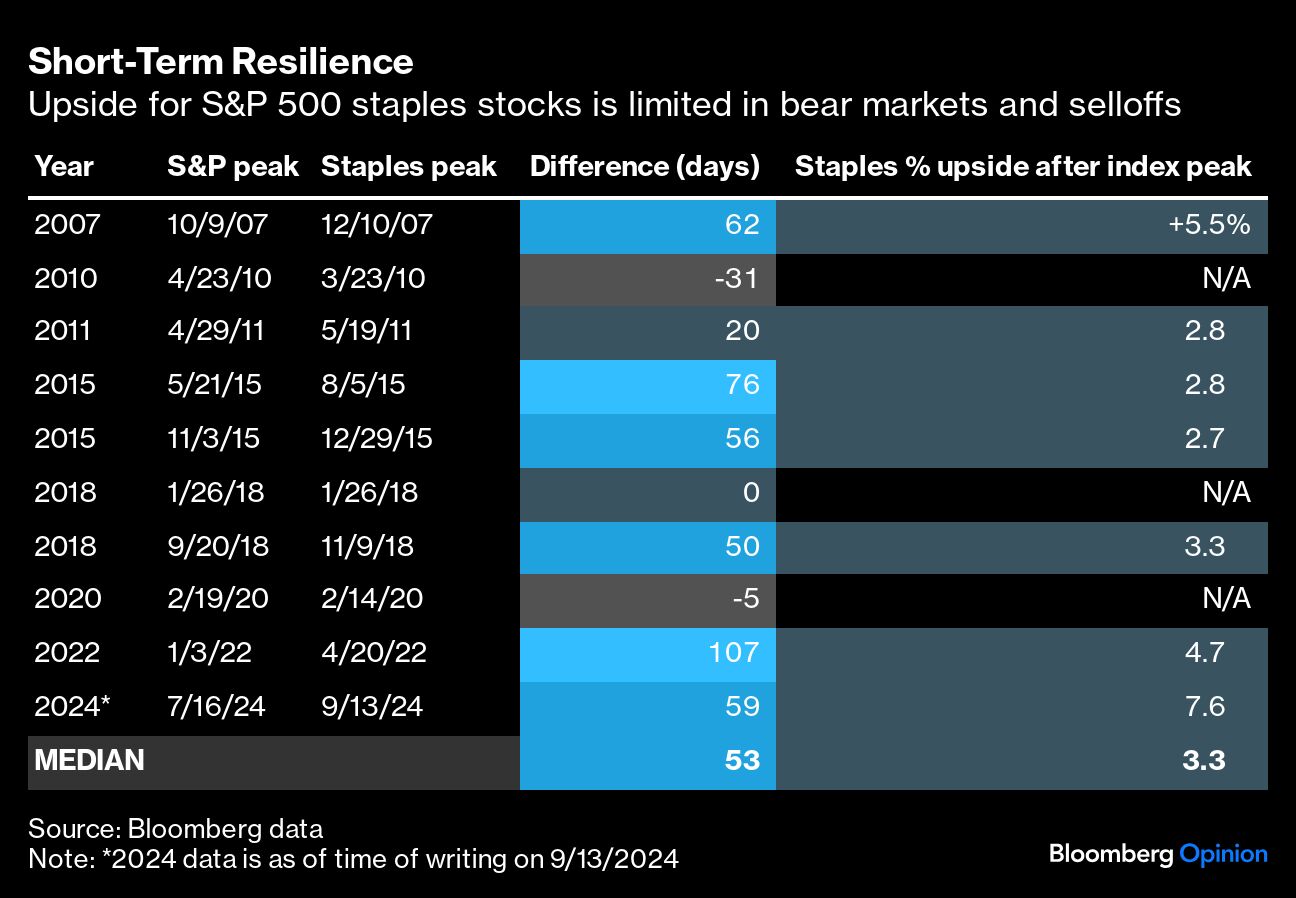

Granted, some people just don’t care about the company-specific fundamentals; they simply see staples as a flight-to-quality bet on macro outcomes. If you’re ultra-bearish on risk assets but simply must own equities (perhaps due to an institutional arrangement), then, sure, by all means continue to buy bleach and tobacco. But as the table below shows, there’s a very finite upside to staples even in noteworthy selloffs and bear markets: They tend to rally for at most a few months after the S&P 500 peaks.

If history is any guide, the boost from this rotation has mostly played itself out. Eventually staples stall or roll over too, either because (a) growth scares fade and investors rotate back into sexier stocks; or (b) macro worries are validated and everything starts to fall together. I still think we’re in the first type of situation, but the staples upside looks pretty tapped out either way.

Of course, one thing that’s true for every corner of the market is this: Events rarely unfold exactly as expected, and valuations can remain stretched for extended periods of time. Personally, I’ve never been great at timing the turns (see my four-months-too-early musings on the overbought consumer discretionary sector). Timing is just a parlor game. But if it’s peace of mind that people are after, staples stocks sure looked a lot safer before their prices reached the stratosphere.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.