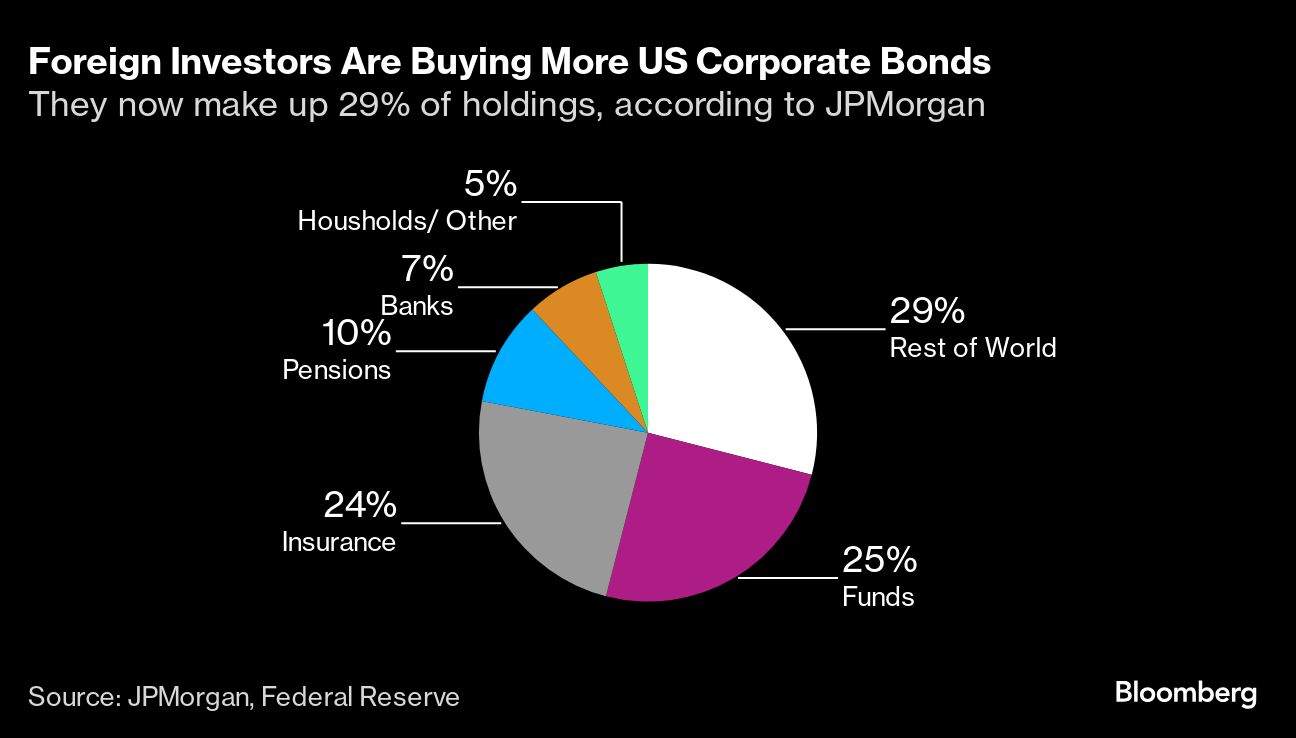

Foreign investors have been buying more US corporate bonds, a trend that will likely continue as Federal Reserve monetary easing lowers the cost of hedging and investors hunt for yield.

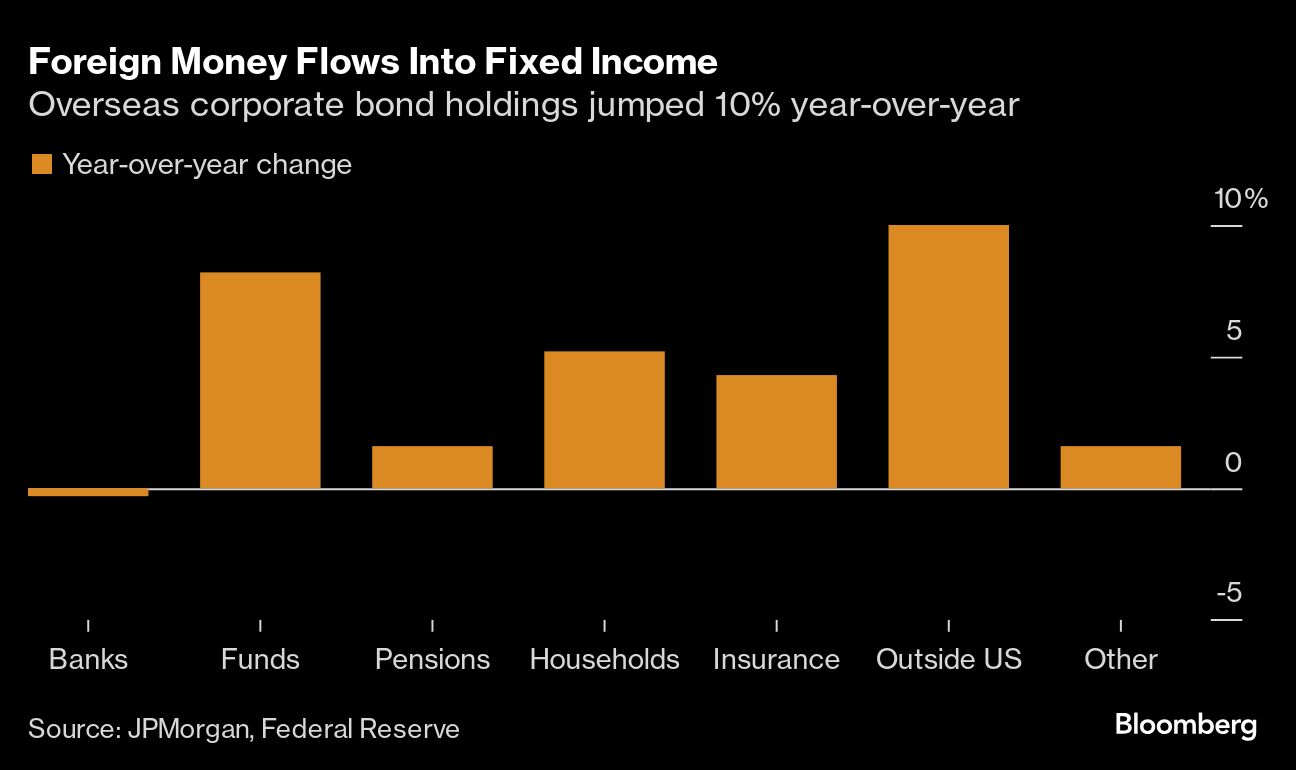

Holdings of the debt by overseas investors jumped 10% year-over-year as of the second quarter, to nearly $4 trillion, JPMorgan Chase & Co. analysts Eric Beinstein and Nathaniel Rosenbaum wrote in a report last month. They see the future attractiveness of US high-grade bonds to this buyer base rising as Federal Reserve rate cuts reduce hedging costs.

For investors in Europe and Asia, lower hedging costs can keep yields from US bonds relatively high in their local currencies even if the Fed is cutting rates. These buyers could become a key source of funds in the future if lower yields end up reducing demand from pensions and insurance companies. At the same time, investors seeking relatively higher yields now are drawn to the US, which began cutting rates after most other developed economies.

“We believe a significant driver of this activity is the fact that most overseas investors were cognizant that the same Fed easing that is driving HG yields lower is also just as likely to drive hedging costs lower too over time,” the strategists wrote.

At the same, the yield curve is expected to steepen as short-term borrowing costs drop and fears of recession diminish, making fixed income attractive. Many people who haven’t invested in credit or those that want more exposure are likely to act now, before yields get lower.

“This is a little bit of a FOMO moment for fixed income,” said Matt Mish, head of credit strategy at UBS Group AG in a phone interview. “You’re in this moment where inflows and duration extension is going to continue. The offshore demand for credit is going to accelerate.” UBS models suggest hedged demand, specifically, to increase closer to the middle of next year.

The strength of US corporate earnings is also an important factor for foreign investors as the US economy grows faster than expected. The rest of the world has not had the same growth outlook and outcome, which makes US fixed income more attractive, according to, Torsten Slok, chief economist at Apollo Global Management.

“With more weakness in Europe, more weakness in Canada, more weakness in Australia, and in particular more weakness in China that’s hitting also buyers from Taiwan,” Slok said in an interview. “You are seeing more demand for US credit because you’re not seeing high yields in the rest of the world,” Slok said.

To be sure, even though US credit is attractive, there are downsides to be wary of — particularly for spread buyers. The average risk premium for high-grade debt is at the lowest level since 2021. That means there is less room for the bonds to tighten, which would translate to a smaller excess return. High-grade spreads look expensive compared to its European counterpart, Bank of America Corp. strategist Yuri Seliger wrote in a note Thursday.

Still, the demand for US corporate bonds isn’t expected to fall anytime soon.

The investment-grade “buyer base has been a strong asset this year which we believe has contributed to keeping spreads tight as different segments of the buyer base have stepped up at different times for different reasons,” JPMorgan’s Beinstein and Rosenbaum wrote.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.