In corporate-speak, when a company says a key target is “currently” unchanged but it plans to disclose a “review” soon, you know trouble is coming. And indeed, there’s trouble ahead for BP Plc.

The British oil major on Tuesday said that it was still buying back $1.75 billion of its stock every three months – a cornerstone of its distribution policy to shareholders. But facing weaker oil and gas prices, BP put investors on notice that it’s set to change strategy very soon. “As part of the update to our medium-term plans in February 2025, we intend to review elements of our financial guidance, including our expectations for 2025 share buybacks,” it said.

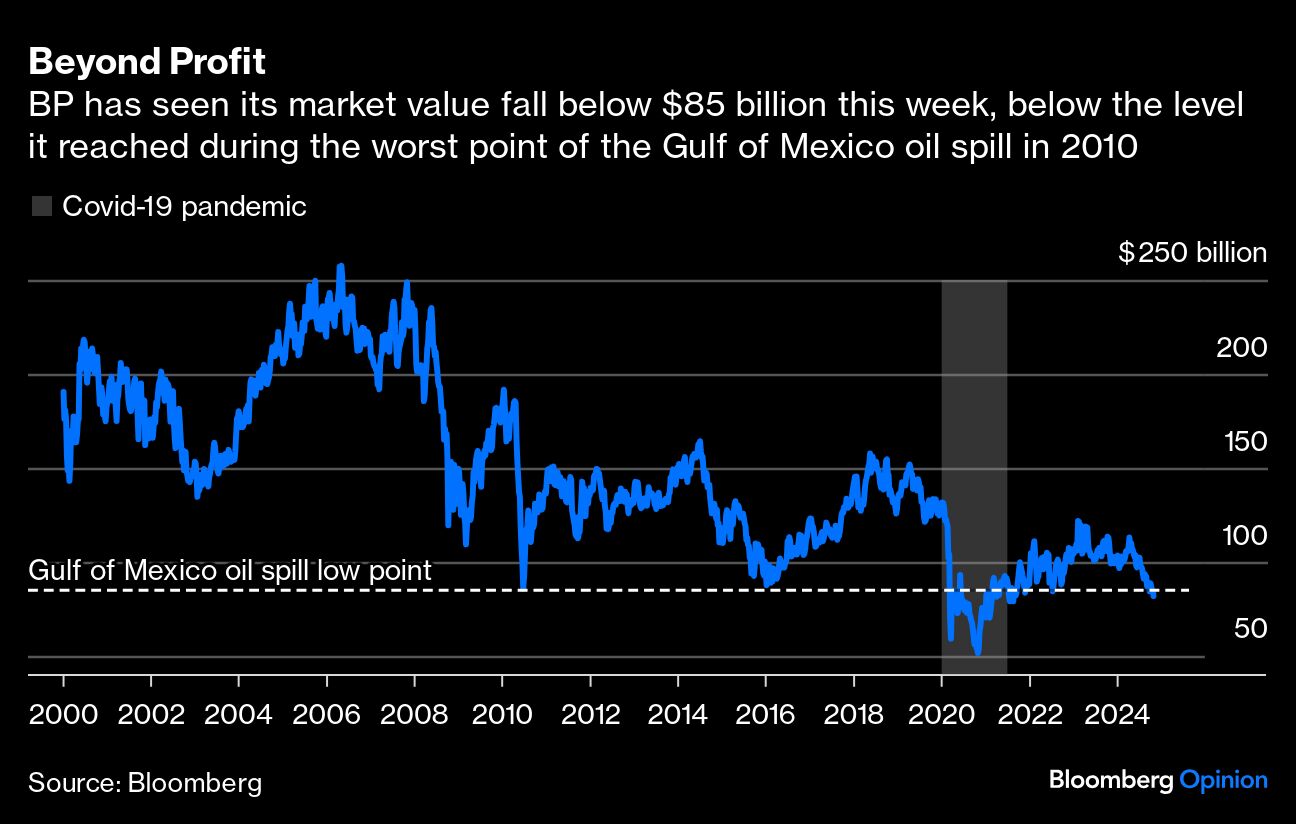

When the captains of the industry have good news, they typically announce it immediately. When they have bad news, they soften the ground with a review, delaying the revelation of harsh reality. Anyone can see the direction BP is taking. The market certainly knows it; BP’s market value dropped to just $82 billion on Tuesday, close to a four-year low. At its current valuation, BP is worth less than during the worst moment of the Gulf of Mexico oil spill in 2010. And, back then, many thought BP was going belly up.

For now, BP is playing for time. The company was able to keep its shareholder distributions unchanged in the third quarter only by taking on leverage. Net debt increased to $24.3 billion from $22.3 billion a year earlier. The increase came despite Brent crude averaging more than $80 a barrel between June and September. Now, Brent is trading closer to $70 a barrel, so the fourth quarter would be more difficult.

The British firm is the most indebted relative to its size and cash generation among the Big Oil companies — a group that includes Exxon Mobil Corp., Chevron Corp., Shell Plc and TotalEnergies SE. On a cash-generation-to-debt basis, BP stood at nearly 40% at the end of 2023, well below its international peers, each reporting more than 75%, according to data compiled by S&P Global Ratings.

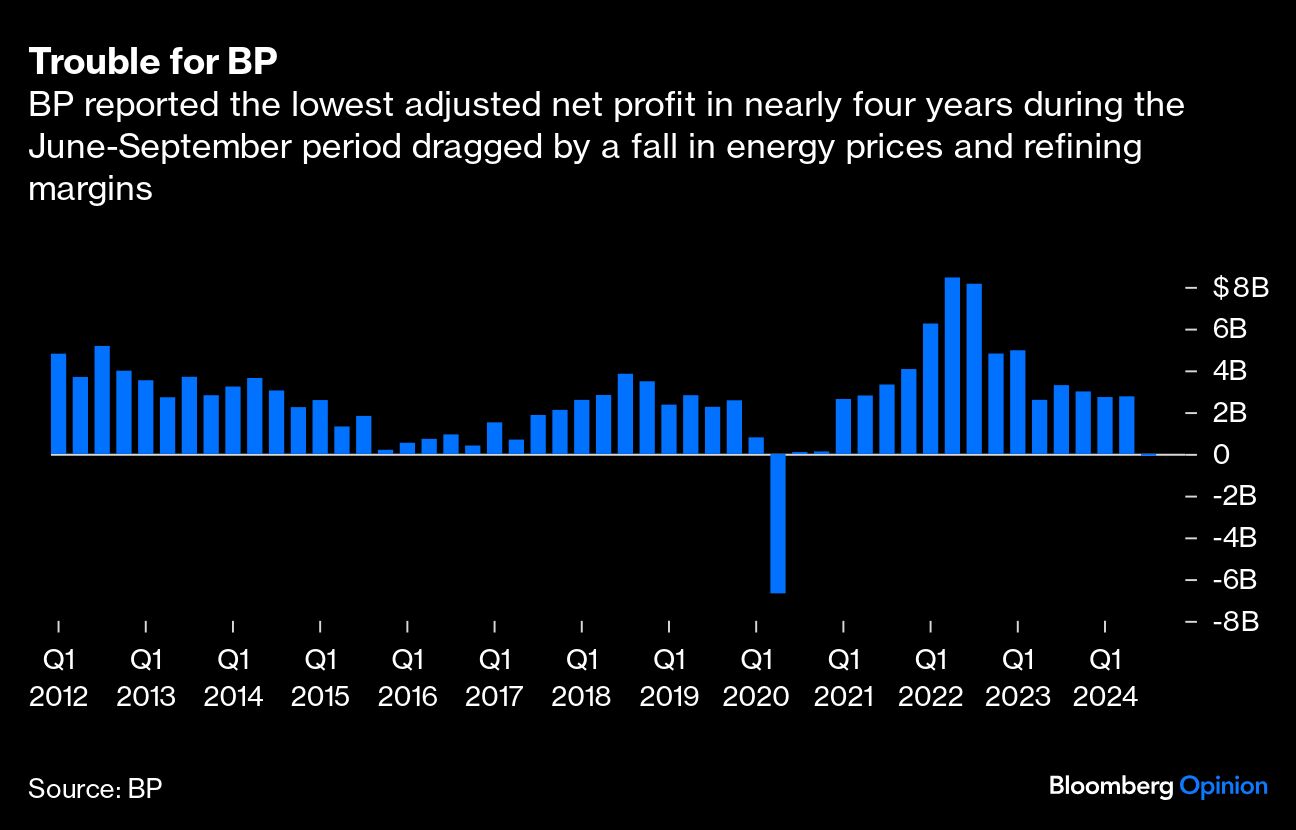

Until now, the indebtedness hasn’t mattered as much because Russia’s invasion of Ukraine in 2022 triggered a spike in oil and natural gas prices, and boosted refining margins. On top, the price volatility of 2021-2023 created rewarding trading opportunities — a corner of the market BP dominates. But that cycle is over. Unsurprisingly, BP reported on Tuesday its weakest quarterly adjusted net profit in nearly four years at $2.27 billion. Worse is to come.

Exxon, Chevron, Shell and TotalEnergies can take on debt to sustain their distribution policies. The American pair probably can afford several quarters of extra leverage; the European pair most likely only a few extra quarters. In the case of BP, I don’t think it should, or can; increased borrowing is the wrong solution.

Instead, at the next earnings announcement in February, Chief Executive Officer Murray Auchincloss should trim the buyback program from $1.75 billion a quarter to something far more affordable — say, $1 billion — to protect the balance sheet. In the oil business, the credit rating comes ahead of the shareholders.

In some ways, a reduction would be the natural result of a changing market landscape. When BP announced its current distribution policy in February, worth $14 billion through 2024 and 2025, it cited “current market conditions.” Back then, Brent was close to $85 a barrel and simple refining margins averaged $30 a barrel. Today, Brent is close to $70 and refining margins are nearer $15.

BP guided investors to expect earnings before interest, tax and depreciation of $46 billion to $49 billion in 2025. Currently, analysts expect ebitda next year of $38 billion, according to data compiled by Bloomberg. Unless the British oil major refocuses on what makes money – oil and gas – and stops wasting precious shareholder’s funds on green adventures that so far have offered little reward, its troubles will continue. The problem is, I don’t know if BP’s management — and, crucially, its chairman and board of directors — have the courage to admit they got the strategy wrong and a new direction is needed.

While it’s natural for distributions to shareholders to decline during a down energy cycle, Auchincloss handcuffed himself too tightly to the market, setting the quarterly buyback amount too high to start with. It didn’t give BP any room for maneuver to weather a potential decline in energy prices. Thus Auchincloss, who took over from disgraced former BP CEO Bernard Looney only in January, looks set to commit the worst of all business sins: overpromising and underdelivering.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas