The bond-market selloff unleashed by Donald Trump’s presidential victory last week ended almost as quickly as it began.

Yet firms like BlackRock Inc., JPMorgan Chase & Co. and TCW Group Inc. have issued a steady drumbeat of warnings that the bumpy ride is likely far from over.

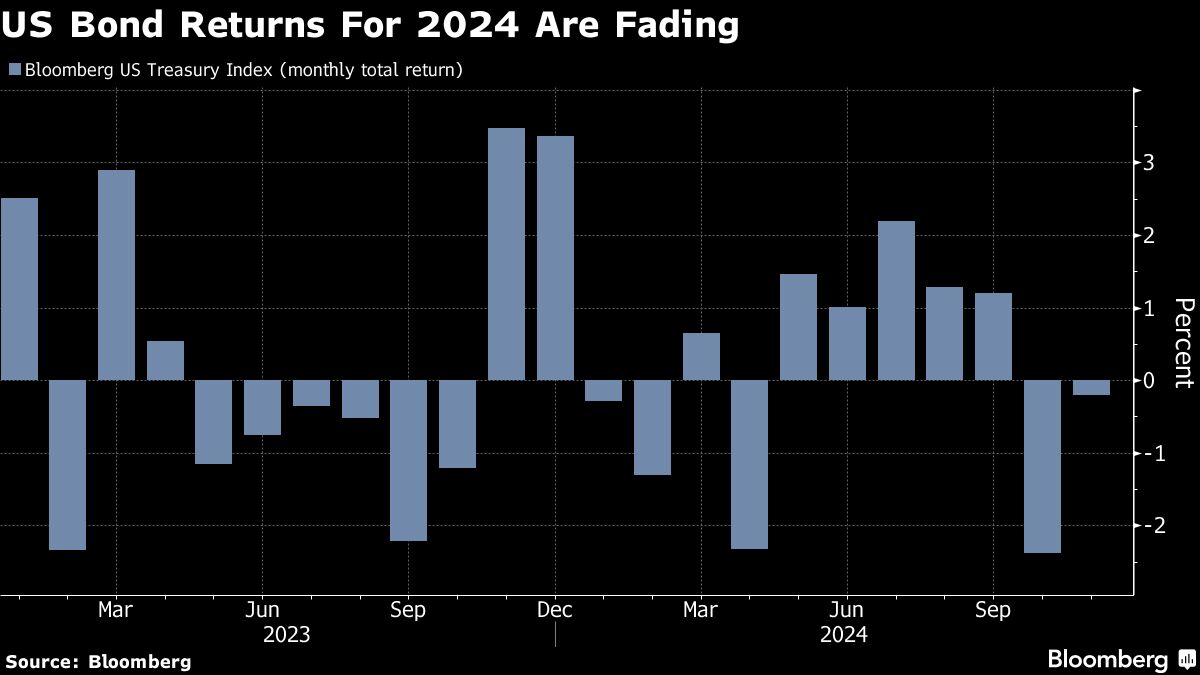

Trump’s coming return to the White House has significantly upended the outlook for the US Treasury market, where October’s losses had already wiped out much of this year’s gains.

Less than two months after the Federal Reserve started pulling interest rates back from a more than two-decade high, the likelihood that Trump will cut taxes and throw up large tariffs is threatening to rekindle inflation by raising import costs and pouring stimulus on an already strong economy.

His fiscal plans — unless offset by massive spending cuts — would also send the federal budget deficit surging. And that, in turn, has renewed doubts about whether bondholders will start demanding higher yields in return for absorbing an ever-rising supply of new Treasuries.

One scenario is “the bond market instills fiscal discipline with an unpleasant rise in rates,” said Janet Rilling, senior portfolio manager and the head of the Plus Fixed Income team at Allspring Global Investments.

She predicted the 10-year Treasury yield could rise back to the peak of 5% hit in late 2023, about 70 basis points above where it was Friday. That “was the cycle high and it’s a reasonable level if there is a full implementation of the proposed tariffs.”

There remains considerable uncertainty about the precise policies Trump will enact, and some of the potential impact has already been priced in, since speculators started betting on his victory well ahead of the vote. While 10- and 30-year Treasury yields surged Wednesday to the highest in months, they came tumbling back down again over the next two days, ending the week lower than they began.

A Bloomberg index of Treasury returns was up just 1.4% as of Friday’s close. There’s no cash Treasuries trading on Monday due to a US holiday.

But the prospect that Trump’s policies will spur growth has driven traders to pare back expectations for how deeply the the Fed will cut rates next year, dashing hopes that bonds would rally as it eased policy aggressively.

Economists at Goldman Sachs Group Inc., Barclays Plc and JPMorgan have shifted their Fed forecasts to show fewer reductions. Swaps traders are pricing in that policymakers will reduce its benchmark rate to 4% by mid-2025, a full percentage point higher than they were predicting in September. It’s in a range of 4.5% to 4.75% now.

The coming week’s economic data, particularly the latest reading on consumer and producer prices, may spark renewed volatility. Fed Chair Jerome Powell, New York Fed president John Williams and Fed Governor Christopher Waller are also set to speak, providing potentially fresh insights on their outlooks.

Federal Reserve Bank of Minneapolis President Neel Kashkari said Sunday the US economy has remained remarkably strong as the central bank progressed in beating back inflation, though the Fed was still “not all the way home.”

What Bloomberg Strategists Say ...

“Election trades are set for a bit of a breather as punters looks to recalibrate risk and sweep a bit of profit off the table. This is kind of what we saw in the aftermath of the election in 2016; after a big rally the day after, the S&P moved sideways for a few days before taking off again. The rise in Treasury yields was more consistent and pronounced, but then again the Fed was on the verge of re-starting its rate-hike normalization, not in the midst of an easing cycle.”

Cameron Crise, macro strategist

Rick Rieder, BlackRock’s chief investment officer for global fixed income, has been telling investors they shouldn’t expect bond prices to rise from here. He said the recent backup is a chance to lock in elevated yields on short-term bonds, but he remains cautious about longer-term debt given the current uncertainty.

After the Fed meeting Thursday, he said in a note to clients that the previous day’s selloff had made short-term yields “extremely attractive.” But “venturing out to the wild blue yonder of longer-term interest rates,” he added, is “maybe not worth that excitement (or the volatility).”

Others see risk the bond market has further room to fall. JPMorgan’s Bob Michele, the chief investment officer and head of global fixed income at its asset management arm, is among those warning that 10-year Treasury yields may eventually climb back to 5% after Trump takes office. At Amundi SA, Europe’s biggest asset manager, CIO Vincent Mortier has flagged that point too, saying it’s a “real alert level” that could ripple into the equity market by driving investors to shift cash over to bonds.

After the Fed cut rates for its second straight meeting on Thursday, Powell declined to speculate on how Trump’s plans may affect the bank’s path and said it wasn’t clear that the recent rise in yields will hold.

But analysts widely expect the next Trump administration to worsen the federal deficit, which has already swelled under President Joe Biden. The Committee for a Responsible Budget last month estimated Trump’s plans would increase the debt by $7.75 trillion more than what’s currently projected through fiscal year 2035.

“At some point, an increasing deficit and debt servicing, all things equal, should lead to a higher yield premium,” said Ruben Hovhannisyan, fixed-income portfolio manager at TCW Group. “The question is the degree of how much more fiscal deficits will grow under this administration.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liz Capo McCormick, Michael Mackenzie