Given that he was just elected, Donald Trump’s plans for financial regulation are, like so much else, a mystery. Yet his campaign’s disdain for the administrative state — and the public’s growing exasperation with red tape — suggests the country is in for a period of bureaucratic humility. Here’s hoping the financial system doesn’t become vulnerable as a result.

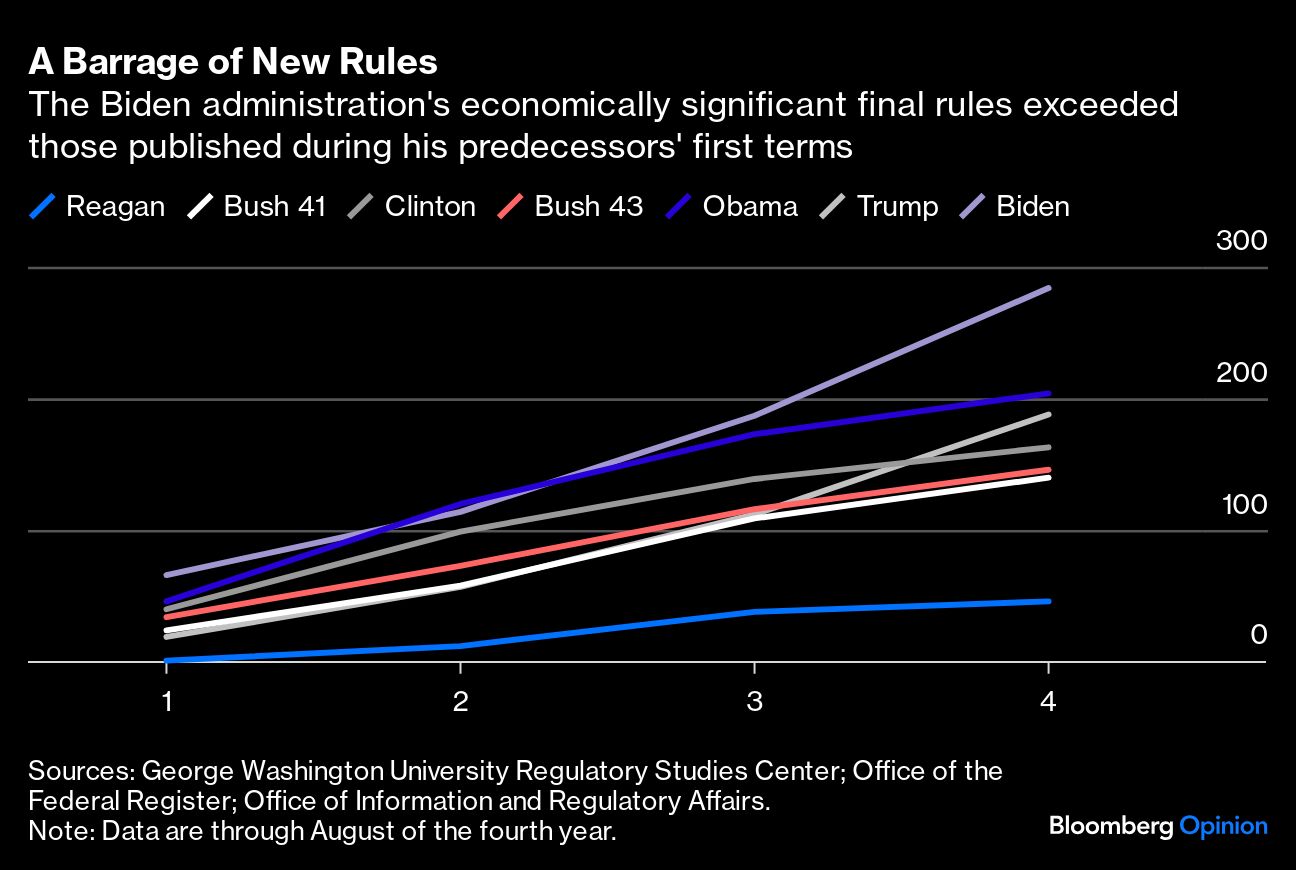

Under President Joe Biden, federal agencies have issued new rules at a historic pace. These proposals were presumably well-intentioned, and some were worthy of support, but their sheer volume — 284 economically significant rules through August — has imposed a serious burden and spurred fed-up businesses to bring a slew of lawsuits, many of them successful. (Voters share the outrage: There’s a reason the death of an Instagram-famous squirrel at the hands of state regulators became a cause célèbre in the campaign’s final days.)

Sensing the zeitgeist, Trump has vowed to reverse all this. He has promised “the largest regulatory reduction in the history of our country” and on Tuesday said he’d appoint the tech impresarios Elon Musk and Vivek Ramaswamy to helm a new “department of government efficiency.” (Musk, for his part, has said that “a bonfire of nonsense regulations would be epic.”) Trump’s goal, expanding on an effort from his first term, is to slash 10 rules for every new one added.

A big reduction in regulation would indeed be welcome. Unfortunately, it’s a complicated task that requires prudence, diligence and sustained attention to detail, virtues that were not in evidence during Trump’s previous stint in office.

Where the financial system is concerned, deregulation may be especially fraught. Last time around, Trump scaled back several major rules adopted after the global financial crisis, an effort that may have contributed to last year’s spate of bank failures. Weakening requirements further, without due discretion, could create needless risk.

Whoever ends up leading this mission, they should keep four principles in mind.

First, banks must be strong enough to weather turmoil. The 2007-2009 crisis showed that an overleveraged system — both banks and nonbanks — was too vulnerable to a drop in asset prices. Last year’s bank failures demonstrated that even “safe” assets can create losses. Ensuring that equity capital levels remain adequate is the best form of protection, and far preferable to elaborate plans for bank resolution or long-term debt-funding requirements.

Next, focus on transparency and accountability. Disclosures should be clear and fraud should be punished. With those guardrails intact, investors should be free to make their own choices and companies free to innovate. By and large, regulators needn’t insert themselves into negotiations between sophisticated investors.

Third, size is not in itself the enemy. Allowing mergers between financial companies doesn’t automatically reduce competition and can in fact increase it. Larger, more diversified banks such as JPMorgan Chase & Co. can be more resilient than small, specialized lenders like New York Community Bancorp (now Flagstar Financial Inc.). It’s true that excessive consolidation can also be a threat. Just witness the bloated aerospace and defense behemoths, or Boeing Co.’s current travails. But details matter, and hard-and-fast rules that simply vilify big banks are insufficient to the task.

Finally, regulation that defies common sense breeds cynicism. As one example among many, the Securities and Exchange Commission routinely extracts fines from financial companies for allowing their employees to converse on nonofficial channels, a practice that is all but unavoidable in the mobile communications era. A focus on changing incentives — so regulators are not rewarded for merely punishing businesses or churning out ever more rules — might help reduce such burdens. Again, though: Proceed with caution.

Dialing back federal regulation after a period of overzealous meddling isn’t the worst idea in the world. One must hope, though, that Trump hasn’t put his finger on a real problem without thinking through the solution.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors