The jury is still out on whether SpaceX is primarily a rocket company, as its name suggests, or actually more of a telecom provider or artificial intelligence play. Its expected valuation doesn’t help resolve the confusion.

With the much-awaited market debut just a day away, traders are poring over the company’s financials to understand what kind of multiple to pay for the stock given its three, very different, business segments. When compared to other publicly traded space companies, the $135 IPO price appears relatively cheap. Yet when placed against other AI firms, it looks much more expensive.

Market pundits have some theories. Some have argued that most space stocks are currently riding on the coattails of SpaceX’s mega-IPO: their valuation multiples a reflection of the market’s high expectation for the Elon Musk-venture formally known as Space Exploration Technologies Corp.

AI stocks, on the other hand, trade at multiples that take their cue from established technology behemoths. Despite the hype and excitement around SpaceX focusing largely on the AI part of the business — its imminent market debut has not created the same magic for other AI stocks that it has for space names.

To some, all the efforts to draw comparisons are futile.

“Just like Tesla isn’t valued like a car company, there is no reason to compare SpaceX to space or AI,” said Brad Conger, chief investment officer at Hirtle Callaghan. “This valuation is really about Elon. He’s a walking Rorschach test, where people project all their desires and fears.”

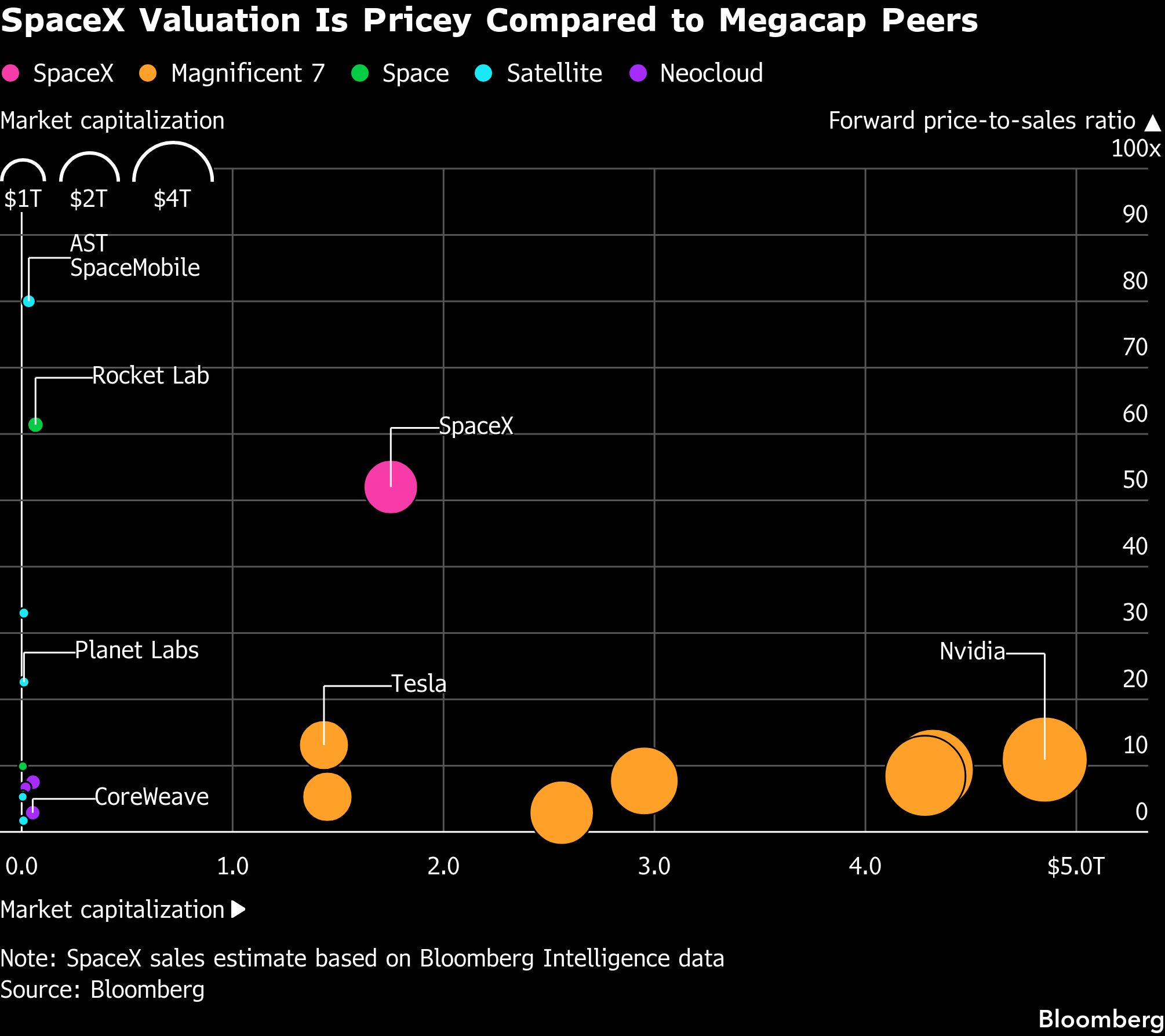

Using the lower end of SpaceX’s targeted valuation of about $1.75 trillion, and Bloomberg Intelligence’s 2026 revenue estimate of about $34 billion, the company’s shares are expected to trade at roughly 52 times sales, according to analyst George Ferguson.

That would be nearly eight-fold bigger than the average price-to-sales multiple of the mega-cap technology companies known as the Magnificent Seven, excluding Tesla, which is an outlier in the group.

Compared to other space-focused companies, such as space transportation firm Rocket Lab Corp., which trades at about 61 times forward sales, and satellite company AST SpaceMobile Inc., which trades at around 80 times sales, SpaceX’s numbers look much more reasonable.

On the other hand, next to companies like AI-focused cloud platform CoreWeave Inc., which trades at about 3 times sales, or AI data center operator Iren Ltd., which trades at about 7 times sales, SpaceX’s estimated valuation looks ridiculously steep.

For now, most of SpaceX’s revenue comes from its satellite business, Starlink. But it is certainly not being valued that way. Satellite communications company Viasat Inc. has a multiple of just 2 times forward 12-month sales, while satellite operator Iridium Communications Inc. trades at a multiple of around 5.

Of course, come Friday, when SpaceX actually starts trading, its estimated valuation multiples could swing widely.

Initial indications from Wall Street suggest expectations are high. On Thursday, Oppenheimer analyst Timothy Horan initiated coverage on SpaceX with the equivalent of a buy rating and a price target of $190. New Street Research’s Pierre Ferragu has set a price target of $165. Meanwhile, the IPO has attracted more than $70 billion in orders from retail investors, according to people familiar with the matter.

There’s also the matter of SpaceX’s final industry classification, a decision that is up to index providers like S&P and MSCI Inc., who might slot it as an industrial, technology-and-AI, or telecom company.

Experts say even that decision may not resolve the valuation question any time soon. As Conger noted, Musk’s other high-profile venture — Tesla Inc. — is categorized as a consumer discretionary company and automaker, but has long traded at multiples that dwarf even the most high-flying tech stocks.

“Starlink is predictable and profitable, xAI is more of a cost center and the space segment provides the innovation and the unlock for the future,” said Laura Rippy, managing partner at venture capital firm Alumni Ventures. “You have to break up the parts of the business and put them back together and see if it makes sense.”

SpaceX’s space business is valued at slightly over $800 billion and would trade at a multiple of about 70 times sales, according to BI. The connectivity division — Starlink — is expected to contribute about $597 billion to SpaceX’s valuation. With estimated revenues of $15.9 billion over the next four quarters, it would trade at a multiple of about 38.

The math for the AI business is a little more complex. BI’s analysis values the segment at $300 billion to $400 billion. Using an annualized revenue of about $3.3 billion for 2026, it would trade at a multiple between 94 and 125. However, if the company can get to an annual recurring revenue of $50 billion, especially after the recently announced deals with Alphabet Inc.’s Google and for AI startup Cursor, that multiple could come down drastically to about 8 to 10 times sales, said BI’s technology analyst Mandeep Singh.

Singh expects the company to hit that run rate in 2027.

“AI companies are generally valued as software or platform businesses, with revenue driven by usage and enterprise adoption, while SpaceX is being valued more like a strategic infrastructure company,” said Eric Diton, president and managing director at the Wealth Alliance. Essentially, investors are pricing SpaceX as if they own critical physical and connectivity infrastructure similar to telecom or cloud platforms, with upside tied to technology and AI, he said.

Whatever the comparison, once SpaceX shares start trading, they will likely be more expensive than all the stocks in the S&P 500 Index on the price-to-sales metric. Currently the priciest stock on the S&P 500 Index by that measure is Palantir Technologies Inc., trading at about 34 times expected sales.

“There’s no question it’s expensive but the company has ramped up its revenue in just a few weeks,” said Kevin Moss, the managing director and portfolio manager of the Private Shares Fund. “It remains expensive but you have other companies out there with 40x-plus multiples like Palantir that continue to do well.”

SpaceX is generating more than $2 billion a month from the deals it just cut with Anthropic and Alphabet, Moss added. “I don’t think you have seen a jump like that ever and that’s a new business line in providing AI compute,” he said.

Moss’s fund already owns SpaceX shares as its largest holding, having originally invested $10 million in 2019, and there are no plans to buy more in the IPO given the fund’s focus on private companies.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.