That’s SpaceX out of the way. Next, investors will have to absorb the artificial-intelligence titans behind the Claude and ChatGPT chatbots, Anthropic PBC and OpenAI. It’s a heady cocktail for a market that isn’t used to swallowing initial public offerings of this size individually let alone in quick succession. How long will the aftereffects take to appear?

SpaceX’s IPO is record-breaking. While founder Elon Musk has been able to raise $75 billion at a $1.8 trillion valuation, this is a massive experiment in what the market can absorb.

IPOs are by definition a gamble and the risk-friendly hedge fund community typically plays a key role in underpinning demand until the wider market provides support. SpaceX is being fast-tracked into the Nasdaq-100 index and will have a huge retail following. We just don’t know how the technical factors are going to play out.

The IPO pitch centered on AI business services. But SpaceX is also part aerospace, part telecoms. One question is how investors in these various sectors make room for it. That’s before we get to the unknown unknowns.

Anthropic and OpenAI could seek valuations of more than $1 trillion each, Bloomberg News reported. They need SpaceX to perform, not just on launch day but in the weeks after. If people lose money on one IPO, they drive a harder bargain on the next one. But the main thing on more careful investors’ minds is whether the market can digest all of this.

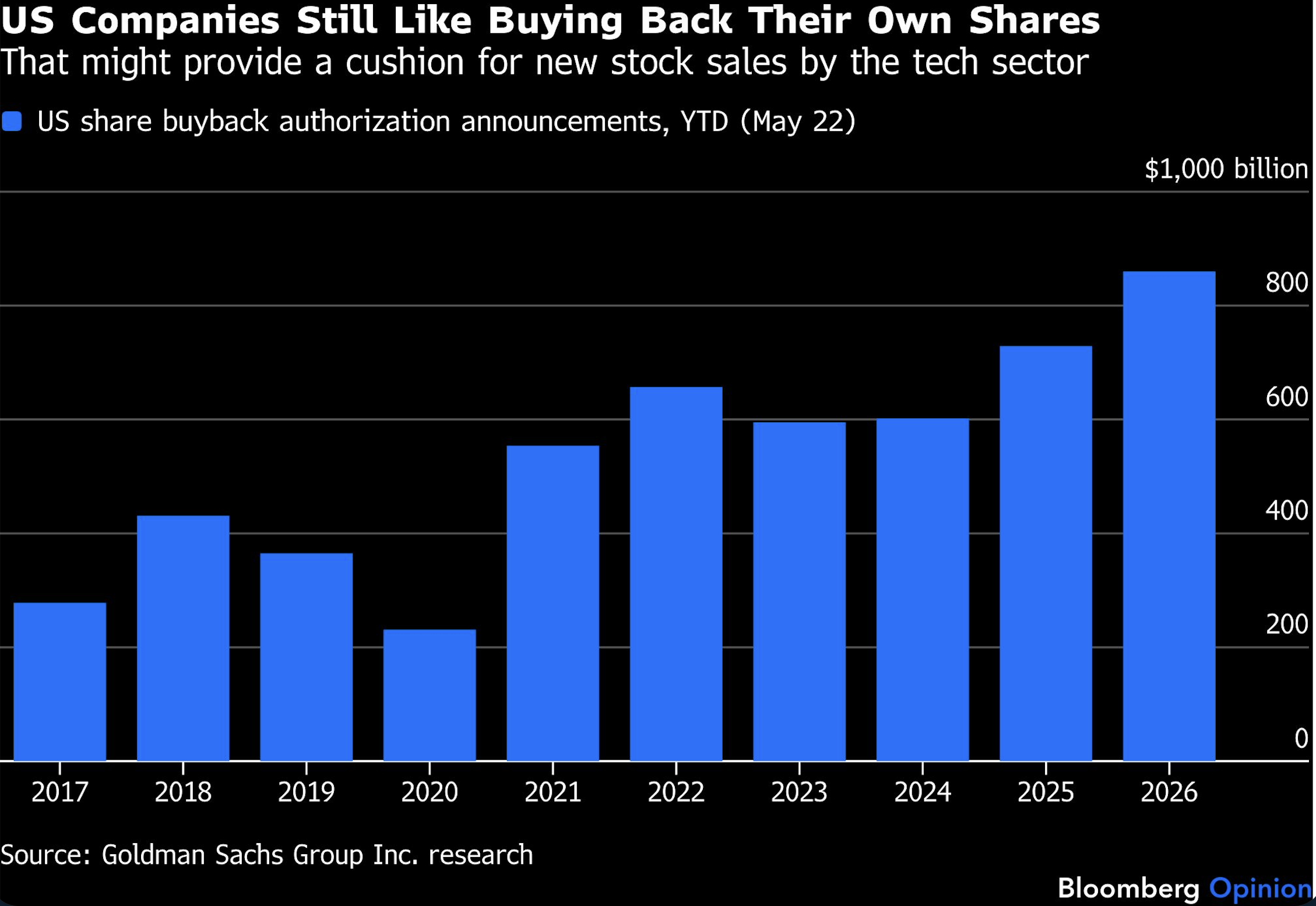

One way to answer is to compare the amount of stock arriving with the amount leaving. Analysts at Goldman Sachs Group Inc. see corporate share issuance touching $1.1 trillion this year, taking in both IPOs and new stock sales by existing listed companies, such as last week’s $85 billion fundraising by Alphabet Inc.

But share buybacks are expected to hit $1.3 trillion, driven by the financial sector and companies that benefit from AI capital spending, meaning investors have money to put to work. Factor in potential cash takeovers and, yes, it looks like the market has the requisite stomach. The balance gets more challenging in 2027, when Goldman’s research cautions on the impact of employees and pre-IPO investors selling their shares as so-called lock-up periods expire.

Strategists at Deutsche Bank AG did a deep dive into the data and academic research on how the stock market performed during past IPO waves. It usually did very well. Market conditions drive IPOs, rather than the other way round, is the ostensibly reassuring verdict. “Stronger equity markets and higher expected profitability led to an issuance wave, but the issuance has little contemporaneous impact back on markets,” the research concludes.

Again, there are caveats. An increase in the supply of stock, all else equal, is indeed negative for equities. The largest IPOs, in isolation, could drag the US market lower by about 1% (but it often falls by more than that). IPO waves “are eventually followed by weaker equity returns, but we note that the waves can run for extended periods,” the analysts say.

Finally, there’s the question of how all this fits into the grand historical arc of “de-equitization” identified by former Citigroup Inc. strategist Robert Buckland more than two decades ago. This is the long-term trend that’s seen more stock leave the market through corporate buybacks and cash takeovers (often by private equity) than enter through share sales.

The roughly $4 trillion of added market capitalization attributable to these banner IPOs would represent a 6% expansion of the US stock market. A big leap. But Buckland points out that it comes after an era of relative drought. That’s entirely different to the period of sizeable tech-equity issuance prior to the 2000-2003 bear market. This time “the glut’s just begun,” he says.

Moreover, the activity today reflects a specific shift in this particular industry, where listed firms that have been able to fund their growth through cash flow now need to raise capital externally given the huge spending demands of AI. Crucially, the equity market is supporting this. As Buckland puts it, the investor ducks are quacking to be fed.

It’s a marked shift all the same. A sector that had been contributing to de-equitization through buybacks is now issuing stock. Investors should be wary of assuming that a big tech firm is going to swoop in with a share buyback that supports its stock price the next time it suffers a fall.

So what is going on looks more like an AI boom than an all-encompassing new-issues boom. Good luck to a midsized company outside this sector if it thinks its IPO will be met with enthusiasm. The ducks are not quacking everywhere.

After SpaceX’s IPO and Alphabet’s fundraising, it’s hard to believe that the market won’t be there for Anthropic and OpenAI. But whether the reason is lock-ups expiring, historical precedent or de-equitization becoming “re-equitization,” there’s surely a red flag here for stock-market performance further down the road.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Innovative ETFs Topics >