When Moody’s Ratings first evaluated Nvidia Corp. almost a decade ago, it settled on a Baa1 investment-grade rating, taking comfort in its relatively light debt load and more than $1 billion of free cash flow after 16 years as a public company.

Last week, Moody’s gave Elon Musk’s SpaceX — despite a limited public financial record, “sustained negative free cash flow” and years of heavy capital spending still to come — the same Baa1 rating.

It is, in many ways, a testament to just how much trust credit markets are putting in Musk and the almost fantastical scope of his ambitions: reusable rockets, a globe-spanning satellite network, artificial intelligence and even data centers in space.

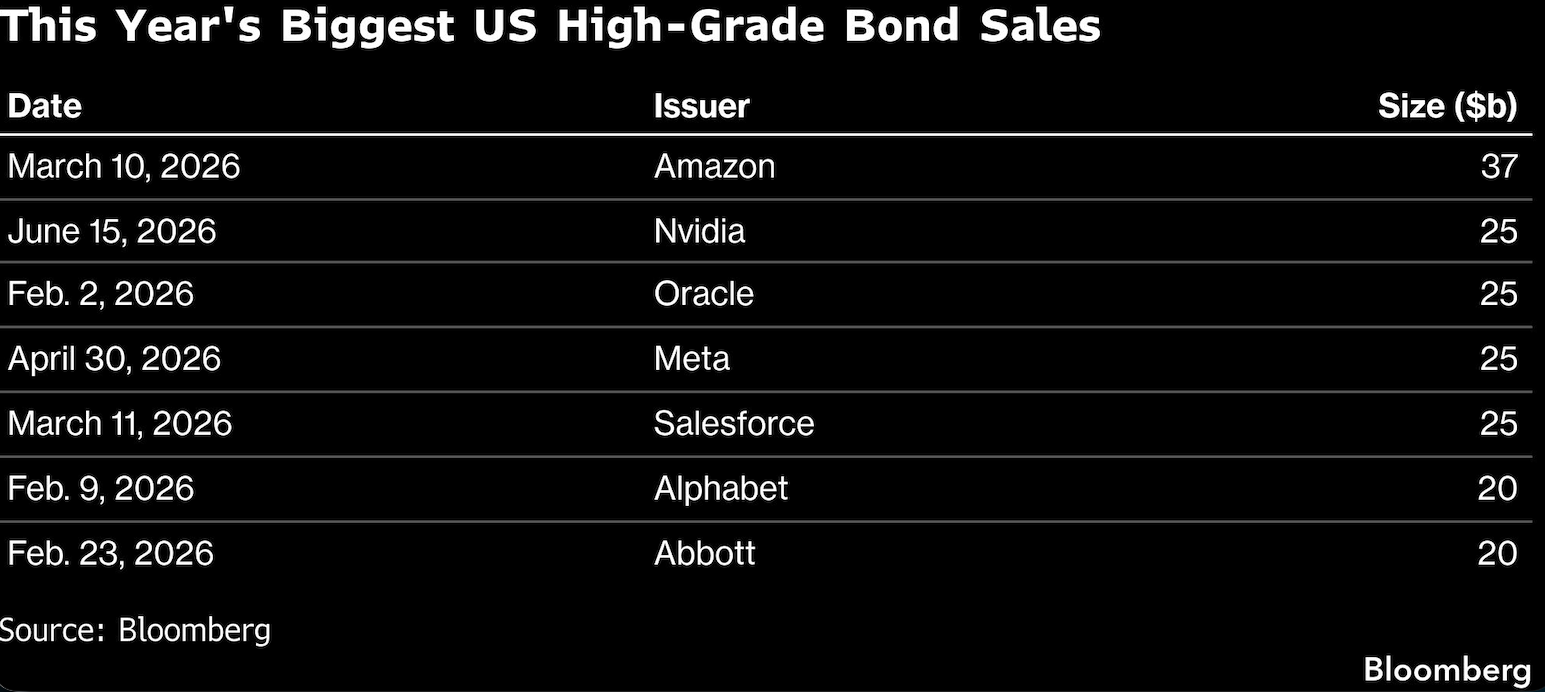

SpaceX is seeking to raise between $20 billion and $25 billion from a debut bond offering on Tuesday, after attracting about $30 billion of investor orders even before the sales process had formally begun, according to people with knowledge of the matter. At that size, the deal would rank among the biggest of the year, according to Bloomberg-compiled data.

In equities, that kind of leap is routine. Buyers pay for big stories in hopes of explosive gains. Yet it’s far rarer in investment-grade credit, a corner of Wall Street built around steady cash flows, manageable leverage and dependable, albeit more modest, returns.

“This should be a phenomenal opportunity in the equity side over the next 10 or 20 years,” said Sal Naro, chief investment officer of Coherence Credit Strategies. “On the fixed-income side, it appears that the agencies are giving them a lot of leeway and a lot of positivity for events that are going to happen in the near- or middle-term.”

For Moody’s, and likewise S&P Global Ratings and Fitch Ratings, the investment-grade case rests more on what SpaceX does have that few borrowers can match: a dominant launch provider central to the US space program, a Starlink satellite network throwing off billions in recurring revenue and access to enough liquidity to keep funding its AI expansion.

Still, SpaceX lacks some hallmarks of a typical high-grade borrower. It is spending heavily, burning through cash and relying on future growth to make the numbers work.

S&P, which grades SpaceX one notch lower than Moody’s at BBB, expects the company to remain cash-flow negative until 2030, with the burn rate rising sharply next year and again in 2028. To help finance that gap, SpaceX is expected to lean much more heavily on debt, with borrowings climbing to $132 billion in 2028. That’s up from close to zero now after adjusting for cash and lease liabilities, according to S&P.

Balancing those risks against SpaceX’s market position made for an unusually complicated rating debate, Naveen Sarma, S&P’s primary analyst for SpaceX, said on a webinar, calling it “one of the more interesting committees I’ve had in my 20 years at S&P.”

SpaceX is selling five tranches of bonds with maturities ranging from five to 30 years. The longest-dated bonds are offered at about two percentage points more than US Treasuries, a person with knowledge of the matter said, asking not to be identified because they’re not authorized to speak publicly. Proceeds will refinance a $20 billion bridge loan and fund other corporate expenses.

Bank of America Corp., Citigroup Inc., Goldman Sachs Group Inc., JPMorgan Chase & Co. and Morgan Stanley are managing the bond sale and declined to comment.

Representatives for Moody’s, S&P and Fitch didn’t respond to requests seeking comment beyond their rating statements. SpaceX, officially named Space Exploration Technologies Corp., didn’t respond to a request for comment.

‘Leap of Faith’

Ross Pamphilon, chief investment officer for fixed income at Impax Asset Management, said SpaceX is asking investors to finance a business that is both unusually strong and unusually hard to model.

“The way we look at it, you’ve got a deeply free-cashflow negative sort of business with a strong AI cash burn that’s xAI, bolted onto your strong franchise in satellite, that’s Starlink,” Pamphilon said, noting that he’s considering participating in the bond sale.

“And then you’ve got the aspirational story around data centers and connectivity and energy efficiency in space, all of which are admirable. But obviously it’s something to get your head around and take a bit of a leap of faith.”

The stock market is making that exercise harder. SpaceX shares have fallen since the IPO, erasing over $600 billion of market value and putting fresh scrutiny on one of the deal’s central selling points: the vast equity cushion sitting beneath bondholders.

For many credit investors, that doesn’t erase the broader appeal. They’re not buying SpaceX because it already looks like a typical high-grade borrower, and its market capitalization is still around $2 trillion. In addition, its launch business has few formidable competitors and much of its near-term spending is tied to projects that supporters expect to pay off sooner rather than later, according to John Lloyd, global head of multisector credit and a portfolio manager at Janus Henderson Investors.

“A lot of the near term capex is going into things that are going to realize returns pretty quickly,” Lloyd said. If Musk “accomplishes 75% of what he sets out to do, this could get ratings upgrades over time and could look much more like one of the hyperscalers.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Caleb Mutua, Davide Barbuscia, Michael Gambale, Aaron Weinman